Structured Products and Modern Asset Allocation: Simplicity is the ultimate sophistication

I. Why Professional Investors Consider Asset Allocation

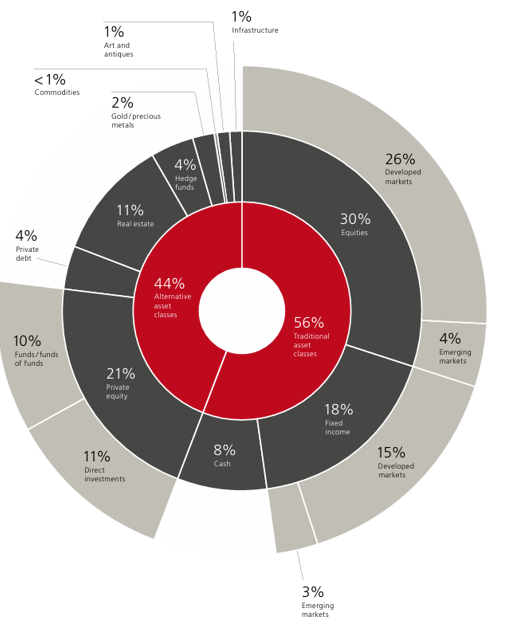

Across the investment world, one idea consistently appears in the way professional and institutional investors manage their portfolios: they start with asset allocation. Instead of focusing on individual products, they begin by thinking about how different parts of the portfolio should work together through various market environments. This broader perspective helps guide decisions on growth, income and risk management in a more structured way.

Equities, fixed income and other instruments each play distinct roles, and the aim is to create a balanced mix rather than rely on any single source of return. As Howard Marks puts it, the future is difficult to predict, so a well-prepared portfolio matters more than trying to identify the perfect moment to invest. Ray Dalio has also highlighted that diversified return drivers help portfolios stay resilient during periods of uncertainty. These are ideas that have shaped how many experienced investors approach their long-term planning.

Recent market conditions have made this approach especially relevant. Interest-rate expectations shift more quickly, macroeconomic cycles evolve faster and traditional asset classes sometimes behave less predictably than before. Because of this, many investors today look beyond the simple equity–bond mix and incorporate tools that offer different patterns of return. Structured products are one example. They do not replace traditional assets, but they can complement them by offering income enhancement or more flexible equity exposure.

In this article, we look at how asset allocation has evolved, where structured products can play a role and how investors can use them thoughtfully as part of a well-constructed portfolio.

II. More Than 60/40 Asset Allocation

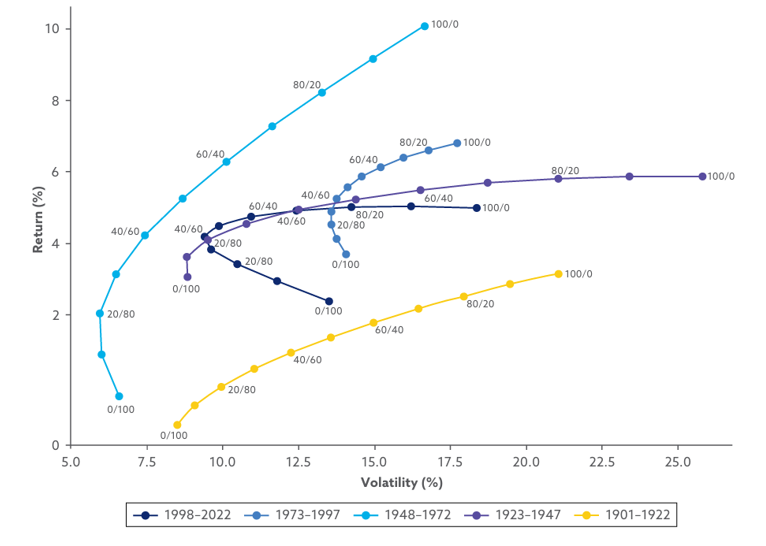

The 60/40 portfolio has been one of the most widely used investment frameworks for decades. Popularized by large pension funds and later adopted broadly by private banks, the idea is simple: allocate roughly 60% to equities for long-term growth and 40% to bonds for income and stability.

For many years, this blend worked well. When equities experienced periods of volatility, bonds often provided protection as interest rates declined and bond prices rose. This balance helped smooth returns and became a reliable foundation for long-term investors.

Historically, such portfolios delivered steady performance. Over long periods, they benefited from strong equity markets and the multi-decade decline in interest rates, which supported bond returns. Because of this consistency, 60/40 became the default model for many investors around the world.

However, the market environment over the past few years has shifted. Several structural changes have challenged the traditional equity–bond mix:

1. Higher market volatility: Economic cycles, interest-rate changes and geopolitical events have created more frequent swings in asset prices.

2. Equity–bond correlations turning positive at times: Instead of moving in opposite directions, equities and bonds have occasionally declined together, reducing the natural protection 60/40 was designed to offer.

3. Weaker diversification from traditional assets: When both major asset classes respond to the same drivers — particularly inflation and interest rates — diversification becomes harder to achieve.

These developments do not diminish the value of equities and bonds themselves. They simply mean that portfolios today benefit from an additional dimension beyond the traditional 60/40 framework that can complement market exposure, provide differentiated income, or reshape risk.

Structured products often serve this role for sophisticated investors, as they offer return patterns that are not identical to stocks or bonds and can be adjusted to different market conditions.

III. A Quick Revisit: What Are FCNs and Accumulators?

In our earlier articles, we introduced two of the most familiar structured product types in private banking: Fixed Coupon Notes (FCNs) and Accumulators/Decumulators (AQDQ).

Rather than revisiting the full technical mechanics, it may be more helpful to think about them through everyday situations.

Fixed Coupon Notes (FCNs): Like renting out your capital for a fixed return

An easy way to imagine an FCN is to think of it as renting out your capital to the market. You agree to “rent” your money for a period of time, and in return, you receive regular coupon payments. As long as the market stays within a certain range, you continue earning this income. If conditions are favourable, the FCN may even “autocall,” meaning your capital is returned early together with the coupons.

This is why many investors use FCNs as an income-enhancement tool, especially when markets are moving sideways and it is difficult to find yield in traditional products.

But there is also a condition: if the market drops too far below a predetermined level, you may need to “take back” the asset — in this case, by ending up with shares at a lower price. This is not necessarily a bad outcome, especially when the investor already likes the underlying company.

Selecting the right underlying stocks is also an important part of using structured products effectively. Professional investors usually choose companies with sound fundamentals and reasonable volatility profiles, as these characteristics help the structure behave more predictably. Simpler, single-underlying structures are easier to evaluate and monitor, and they align more directly with the investor’s intended exposure.

In essence, FCN can:

• Earn steady income as long as the market stays within range

• May receive shares if the market declines beyond a certain point

• Useful for investors comfortable owning the underlying stock at a cheaper price

Accumulators: Like buying something gradually when it goes on discount

Accumulators can be thought of as a way to accumulate shares at regular intervals, often at a discount to the current market price.

Imagine you are a long-term fan of a particular company. Instead of buying all shares at once — when the price may be high or volatile — an accumulator allows you to buy gradually over time, often at a lower effective price.

This can be helpful when:

• You believe in the company

• You prefer not to invest a large lump sum at once

• You want to benefit from lower entry prices if the market dips

However, as with many good deals, there is a trade-off: if the share price keeps falling, you continue buying shares, which means your total exposure increases.

For investors who genuinely want to build a long-term position in a company, this can be acceptable. But for those who only want limited exposure, it requires careful sizing.

In short:

• Buy gradually, often at a discount

• Build a position over time, useful for long-term believers

• Be mindful of increasing exposure in a falling market

Be Careful With Multi-Underlying FCNs

Multi-underlying FCNs deserve particular care. These structures often show higher coupons because one of the linked stocks carries significantly higher volatility. While the headline yield may look attractive, the pricing dynamics become more complex: the high-volatility stock usually contributes most of the premium and also drives most of the risk.

For example, in an FCN linking two stocks—one known for higher volatility (Stock A) and another recognized for stronger fundamentals and stability (Stock B)—using both together tends to result in a less favorable strike level compared with a single-underlying FCN based solely on the volatile stock (Stock A), assuming all other terms are the same.

In a market decline, the volatile stock is also more likely to breach its barrier first, which reduces the diversification benefit that the multi-underlying structure seems to provide. Additionally, high-volatility names often take longer to recover when markets stabilize, as liquidity typically returns first to larger, more established companies.

For these reasons, many institutional investors prefer simpler structures with clearer and more transparent risk profiles.

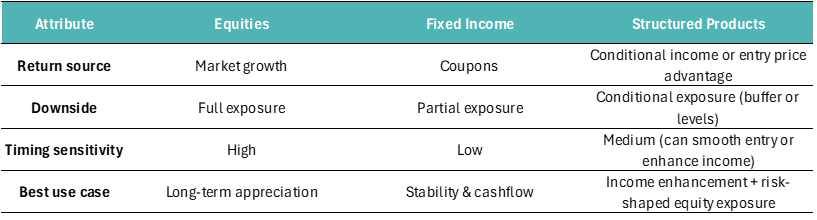

IV. Fit Structured Products Inside a Portfolio

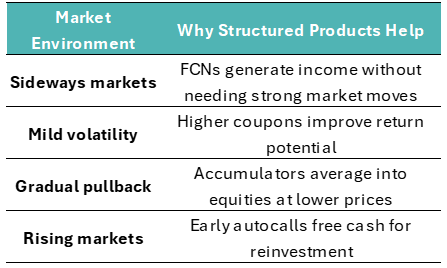

Structured products sit between traditional equities and fixed income, which is why many sophisticated investors use them as a third layer in their portfolios. Equities provide long-term growth but come with full market volatility, while bonds offer income and stability but may struggle to deliver attractive returns when interest rates move unpredictably. Structured products combine elements of both: they can offer higher income than most bonds while providing a more controlled form of equity exposure. This makes them especially useful in markets that are uncertain, range-bound or gradually trending—conditions where neither equities nor bonds are at their best.

Because of these characteristics, structured products tend to be helpful in environments where equities are not trending strongly or where investors are unsure about timing. FCNs can generate steady income during sideways markets, while accumulators allow investors to build equity positions gradually when valuations are uncertain. In periods of moderate volatility, structured products often offer more attractive terms, adding flexibility to the overall asset mix.

From a portfolio-level perspective, structured products are most effective when used as a modest but meaningful allocation. For many balanced investors, an allocation of around 10% to 20% offers sufficient exposure to benefit from enhanced income or smoother entry into equities, without concentrating the portfolio in a single payoff structure. Conservative and growth-oriented investors may adjust this range depending on how comfortable they are owning the underlying equities should markets decline.

In short, structured products do not replace equities or bonds; they complement them. By offering income enhancement, more flexible timing and shaped equity exposure, they help portfolios navigate conditions where traditional assets alone may not provide the most consistent outcomes.

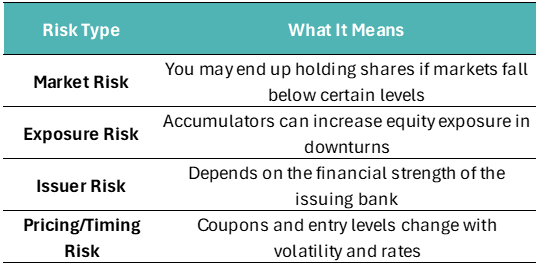

V. A Sensible Reminder of Risks

Structured products can be effective tools, but they still carry risks. FCNs may deliver shares if markets fall below certain levels, and accumulators can increase equity exposure during extended declines. Their performance also depends on conditions such as volatility and interest rates, which influence coupon levels and strike prices. As with any investment, careful selection of underlyings, diversification across issuers and sensible sizing help keep risks manageable.

Multi-underlying FCNs require particular attention. Higher coupons often come from including a stock with significantly higher volatility, which also becomes the main driver of downside risk. In a stressed market, this volatile name is typically the one that breaches the barrier first, making the perceived diversification less effective. Understanding this dynamic is important to ensure the structure matches the investor’s intention.

A few simple guidelines can improve the experience:

1. choose underlying with strong fundamentals,

2. avoid chasing very high coupons (moderate coupons often come with more balanced risk), and

3. consider shorter durations for greater liquidity and flexibility.

Applied thoughtfully, structured products can support the overall portfolio without adding unnecessary risk.