Understanding Structured Products Series 6 Sarah and Emma Investment Adventures – Fixed Coupon Notes (FCN)

Understanding Structured Products Series 6: Sarah and Emma’s Investment Adventures – Fixed Coupon Notes (FCN)

Introduction: A New Adventure in the World of Structured Products

Meet Sarah and Emma, two ambitious young professionals navigating the exciting yet complex world of investing. Sarah, a tech enthusiast with a knack for spotting market trends, has been intrigued by the buzz around structured products. Emma, her cautious yet curious friend, prefers safer investments but is open to learning about opportunities that balance risk and reward. Together, they’ve been exploring financial strategies under the guidance of their trusted advisor, Alex, a seasoned portfolio manager with a talent for breaking down complex concepts.

In their latest meetup at a cozy coffee shop in New York, Sarah and Emma are eager to dive into Fixed Coupon Notes (FCNs). They’ve heard FCNs can offer attractive returns, but whispers of their risks—especially the knock-out (KO) mechanism—have piqued their curiosity. Alex, with his usual blend of wit and wisdom, is ready to guide them through this intriguing financial instrument, shedding light on its allure and hidden dangers.

What Are Fixed Coupon Notes (FCNs)?

“Alright, let’s start with the basics,” Alex begins, sipping his latte. “Fixed Coupon Notes are structured products that combine a zero-coupon bond with the sale of put options, offering investors a steady stream of fixed coupon payments. Think of them as a hybrid: you get bond-like stability with the potential for enhanced returns from the options component.”

Sarah leans forward, intrigued. “So, it’s like getting regular interest payments, but with a twist?”

“Exactly,” Alex replies. “The ‘twist’ comes from the put options you sell as part of the FCN. These generate the premium that funds those juicy coupons. The catch? Your returns depend on the performance of an underlying asset—like a stock, index, or currency pair.”

Alex adds, “When you invest in an FCN, the issuer takes your money and uses it strategically. They buy a zero-coupon bond to secure the principal repayment at maturity, hedge the put options you’ve sold to fund the coupons, and manage the knock-out feature to limit their costs. This setup lets them offer high coupons, but it’s a calculated game—they’re hedging their bets while you take on the market risk.”

Emma, ever the cautious one, raises an eyebrow. “That sounds promising, but what’s this knock-out feature everyone’s talking about?”

Alex smiles. “Great question. Let’s dive into that—it’s where things get really interesting, and potentially risky.”

The Knock-Out Feature: A Double-Edged Sword

What Is Knock-out feature?

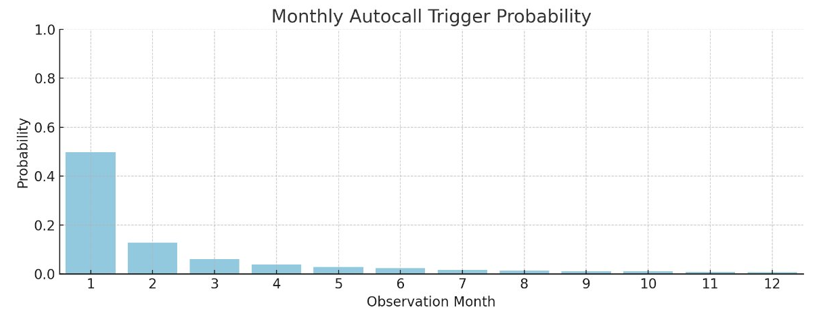

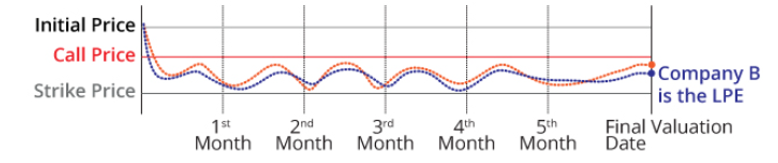

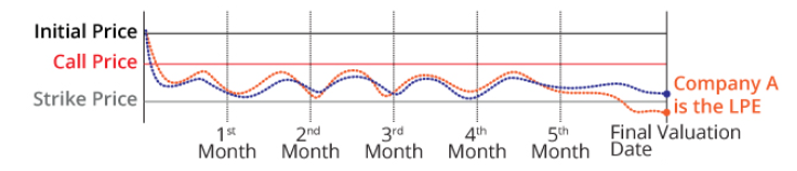

Alex pulls out his tablet and sketches a simple diagram. “With knock-out feature, FCN can be ‘called back’ or redeemed early by the issuer if certain conditions are met. These conditions are tied to the performance of the underlying asset. For example, if the asset’s price reaches a predefined call barrier—say, 110% of its initial value—on a specific observation date, the FCN is automatically redeemed. You get your principal back, plus any accrued coupons, and the contract ends.”

Sarah nods. “So, it’s like the issuer can hit the ‘eject’ button if the market performs well?”

“Spot on,” Alex says. “But here’s the trap behind knock-out: it’s designed to benefit the issuer as much as—if not more than—the investor. The issuer prices in the probability of an early call based on market data and their sophisticated models. If the FCN is called early, they pay fewer coupons over the product’s life, saving them money. The earlier the call, the less they owe you. The catch? Investors don’t have access to those probability models, so you’re at a disadvantage. And if the market drops, you can’t just ‘stop the loss’—you’re locked in until maturity or a call event, exposed to the full downside risk.”

Emma frowns. “That sounds like the issuer has all the control.”

“Exactly,” Alex replies. “The KO feature makes FCNs appealing because it offers the potential for early redemption with a tidy profit. But it also limits your upside and introduces risks that aren’t immediately obvious.”

Why It’s Attractive

Alex lists the reasons why KO FCNs draw investors in:

• Enhanced Coupon Rates: “The KO feature allows issuers to offer higher coupons than traditional bonds, since they might redeem the note early, reducing their obligation.”

• Potential for Early Profits: “If the underlying asset performs well, the FCN might be knocked out after a few months, returning your principal plus coupons faster than expected.”

• Capital Protection (Sometimes): “If the underlying asset’s price stays above the strike price at maturity, the investors receive full principal with coupons even if it dipped below the initial level during the term. This safety net appeals to cautious investors like you, Emma.”

Emma perks up. “That sounds pretty good. So, what’s the catch?”

Alex’s expression turns serious. “The catch is that the KO feature can work against you, especially in volatile markets. Let’s break down the risks.”

The Hidden Dangers of KO FCNs

1. Capped Upside Potential

“The biggest drawback,” Alex explains, “is that the KO feature caps your gains. Imagine you invest in an FCN linked to a tech stock index. If the index surges 20% in the first year and triggers the KO, you get your principal back plus the fixed coupons—say, 8% annually. Sounds great, right? But if the index keeps climbing to 50% over the next year, you miss out on those gains because the note was redeemed early.”

Sarah frowns. “So, it’s like being forced to cash out just when the party’s getting started?”

“Exactly,” Alex says. “The KO feature protects the issuer by limiting their payout, but it can leave you regretting not holding a direct investment in the underlying asset.”

2. Strike Price Risk and Downside Exposure

Alex continues, “In a typical FCN, there’s a strike price—say, 90% of the underlying asset’s initial value. If the asset’s price at maturity is below this strike, you could lose part of your principal. For example, if the index falls to 80% of its initial value, you might get back less than your investment, even after collecting coupons.”

Emma’s eyes widen. “So, even with those nice coupons, I could lose my principal if the market tanks?”

“Yes,” Alex confirms. “In a standard FCN, a drop below the strike price at maturity hurts you.”

3. Market Timing Risk

“Another risk,” Alex adds, “is that KO FCNs are sensitive to market timing. If the underlying asset hovers just below the KO barrier, the note might not be redeemed early, and you’re locked in for the full term—potentially years. During that time, you’re earning coupons but missing out on other investment opportunities.”

Sarah scribbles a note. “So, it’s like being stuck in a long-term commitment when the market’s teasing you with better options.”

Alex chuckles. “That’s a great way to put it. And if the market turns volatile, you might end up with a note that neither gets knocked out nor protects your capital if it falls below the strike.”

4. Complexity and Lack of Transparency

“Finally,” Alex says, “FCNs with KO features are complex. The terms—KO barriers, strike prices, observation dates—can be confusing, even for seasoned investors. Plus, these are often over-the-counter (OTC) products, meaning they’re customized and not traded on an exchange. This makes them harder to value or sell before maturity, and you’re reliant on the issuer’s creditworthiness. FCNs are like black boxes—investors often have to accept whatever prices issuers provide.”

Emma sighs. “So, it’s like signing a contract with fine print you need a magnifying glass to read.”

“Exactly,” Alex says. “You need to understand every detail, or you might be in for a surprise.”

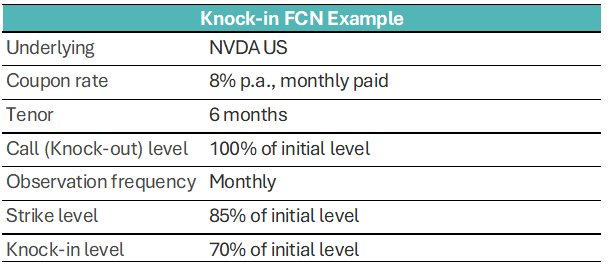

A Real-World Example: Sarah’s Tech Bet

To make things concrete, Alex walks Sarah and Emma through a hypothetical FCN investment.

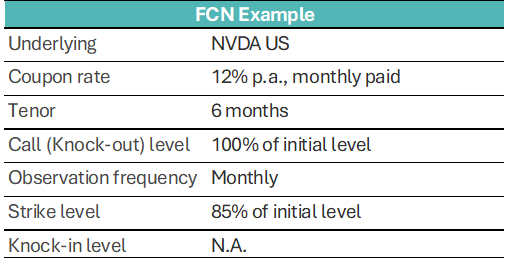

“Let’s say Sarah invests $100,000 in a typical FCN with these terms:

Scenario 1: Early Call (Bullish Market)

If NVDA’s stock price reaches 100% of its initial value after 3 months, the FCN is knocked out. Sarah receives her $100,000 principal plus 3 months of coupons (1% per month = $1,000 × 3 = $3,000). Total return: $3,000. But if NVDA climbs to 150% over the next few months, Sarah misses out on those gains.

Scenario 2: No KO, No Strike (Stable Market)

If NVDA stays between 85% and 100% for 6 months, the FCN isn’t knocked out, and the stock price is above the strike level at maturity. Sarah receives 12% coupons annually ($1,000 per month × 6 = $6,000) and her $100,000 principal. Total return: $6,000 over 6 months.

Scenario 3: Receiving Shares at Maturity (Bearish Market)

If NVDA drops to 80% at maturity, below the 85% strike level, Sarah receives only $80,000 of her principal, plus $6,000 in coupons. Net return: $80,000 - $100,000 + $6,000 = -$14,000 loss, with significant capital erosion despite the coupons.

Sarah whistles. “That last scenario sounds scary. You could end up worse off than just holding a bond.”

“Exactly,” Alex says. “The coupons are tempting, but the downside risk can wipe out your gains—or more—if the market turns against you.”

Why Investors Fall for FCNs

Sarah raises a hand. “If these are so risky, why do people invest in them?”

Alex leans back. “It’s the allure of high coupons and the promise of capital protection. In a low-interest-rate environment, investors are hungry for yield. An 10% coupon looks incredibly attractive compared to a 4% Treasury bond. Plus, the KO feature makes it seem like you can get in and out quickly with a profit. But as we’ve discussed, the risks are often understated because issuers have already priced in the likelihood of an early call, giving them an edge.”

Emma nods. “It’s like being offered a shiny new car without being told it might break down on the highway.”

Alex laughs. “That’s a great analogy. The key is to understand the engine under the hood before you take it for a spin.”

Tips for Navigating FCNs

Alex shares some practical advice for Sarah and Emma:

1. Understand the Terms: “Read the fine print. Know the knock-out level, observation dates, and what happens at maturity. If anything’s unclear, ask your advisor.”

2. Assess the Underlying Asset: “Choose an asset you’re confident in. If you think the NASDAQ 100 is stable or likely to rise modestly, an FCN might work. If you expect volatility, think twice.”

3. Consider Your Risk Tolerance: “If losing principal scares you, look for FCNs with deeper strike level or full capital protection, but expect lower coupons.”

4. Diversify: “Don’t put all your money in one FCN. Spread your investments across different assets or strategies to reduce risk.”

5. Monitor Issuer Credit Risk: “Since FCNs are OTC products, the issuer’s financial health matters. Stick with reputable institutions.”

6. Have an Exit Plan: “Know whether you can sell the FCN before maturity and at what cost. Liquidity can be limited.”

Improving Your FCN Strategy

Emma looks curious. “Is there a way to make FCNs less risky for us?”

Alex nods. “Great question. Here are some strategies to tilt the odds in your favor:

• Reduce Observation Frequency: Instead of monthly observation dates for the knock-out, opt for quarterly observations. This reduces the chance of a knock-out being triggered by a short-term market dip, giving you more protection. It also makes the issuer’s pricing less aggressive, as they can’t bank on frequent checks to call the note early.

• Choose Bullet FCNs: With a Bullet FCN, you receive the full coupon for the entire term upfront or on the first observation date, rather than incrementally. This locks in your income early, reducing the risk of losing coupons if the note is called. It’s like getting paid for the whole job before you even start!”

• Explore Knock-In FCNs: Some FCNs, though less commonly traded, include a knock-in feature that sales teams might not highlight. Here, the strike price doesn’t kick in unless the asset’s price falls below a knock-in barrier—say, 70% of its initial value. This adds an extra layer of protection, as you’re safe from losses unless that barrier is hit. The trade-off? You’ll get a lower coupon rate, so weigh if the added safety is worth it for you.”

Sarah grins. “That sounds like a smarter way to play the game.”

“It is,” Alex says. “These tweaks can’t eliminate the risks, but they give you more control and protection.”

The Bigger Picture: Lessons from Sarah and Emma

As their coffee cups empty, Sarah and Emma reflect on their journey. Sarah’s excited about the potential of FCNs to boost her portfolio’s yield, but she’s now aware of the need to carefully assess the underlying asset and terms. Emma, meanwhile, appreciates the income potential but plans to stick with Knock-in FCNs that offer additional protection.

Alex leaves them with a final thought: “Structured products like FCNs are powerful tools, but they’re not a one-size-fits-all solution. They reward knowledge and discipline, but they punish overconfidence. Always align them with your financial goals and risk tolerance.”

Conclusion: Your Investment Adventure Awaits

Sarah and Emma’s exploration of knock-out Fixed Coupon Notes highlights the delicate balance between opportunity and risk in structured products. The high coupons and early redemption potential are undeniably attractive, but the capped upside, knock-in risks, and complexity demand careful consideration.

For investors, the key is education. By understanding the mechanics of FCNs and their knock-out features, you can make informed decisions that align with your financial aspirations. Whether you’re chasing yield like Sarah or prioritizing safety like Emma, structured products can play a role in your portfolio—if you approach them with eyes wide open.