Wired For Profit - US Power Series

US Power Series 1 - How America's Power Grid Actually Works and Where the Investment Opportunity Lies

The U.S. power sector is experiencing one of its most consequential structural shifts in decades. The rise of AI data centers — energy-hungry, always-on, and growing fast — is colliding with a grid that was designed for a very different era.

A single hyperscale AI data center can require 100–300 megawatts of continuous electricity — roughly equivalent to the power consumption of 80,000–250,000 U.S. households. Unlike traditional enterprise computing loads, these facilities run at high utilization around the clock, creating a new class of industrial-scale, always-on electricity demand.

To understand where capital will flow and where returns will be earned, we need to grasp something most overlook: the deep operating logic beneath America's electricity system.

This essay unpacks that logic — and maps it directly to where the money is.

1. The Fundamental Rule: Every Watt Must Balance in Real Time

Electricity is unlike any other commodity. Because it cannot be stored at scale, the physics of the grid requires that generation and consumption match continuously — every second of every day.

Frequency stability is the signal: keeping supply and demand in balance keeps frequency locked at 60 Hz — the standard that all grid-connected equipment is designed to operate at. Let that balance slip, and cascading failures follow.

The entity responsible for maintaining this balance is called a Balancing Authority (BA). In regions with organized wholesale markets, this balancing role is typically performed by Independent System Operators (ISOs) or Regional Transmission Organizations (RTOs), which simultaneously operate the grid and administer electricity markets.

This real-time balancing imperative is the central constraint around which all market design, regulation, and investment logic is built.

At the macro level, the U.S. grid is divided into three largely separate physical interconnections:

• Eastern Interconnection — covering most of the eastern two-thirds of the country

• Western Interconnection — the western states

• ERCOT — the Texas grid, operating largely in electrical isolation from the others

⚡ Key Insight: These interconnections operate independently. Power cannot freely flow between them, which means regional supply-demand dynamics — and investment theses — are highly localized.

2. The Four Links in the Value Chain

The electricity system is not a monolith. It is composed of four distinct business activities, each with its own economics, risk profile, and regulatory treatment.

A. Energy Generation — Converting Fuel into Electrons

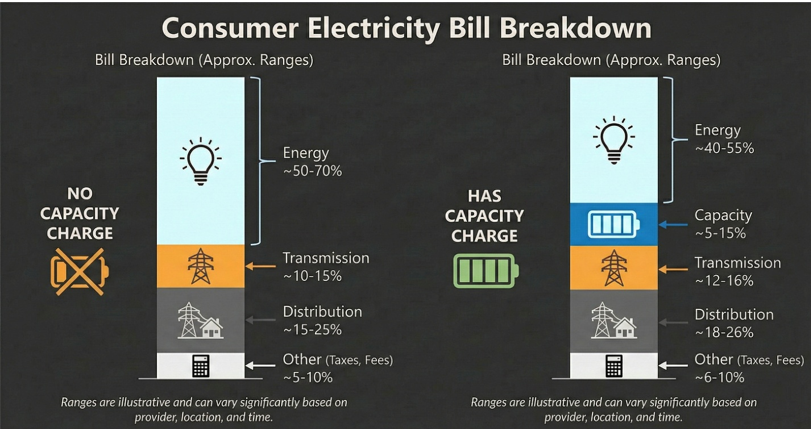

Generation assets convert energy into electricity: thermal plants, nuclear, hydro, renewables, and increasingly battery storage. This could account for 40–70% of your bill. In markets with a capacity charge — such as PJM — an additional 5–15%.

Ownership can take two forms:

• Regulated utility-owned generation: costs are passed through to ratepayers via a regulated rate structure

• Merchant / independent power producers (IPPs): revenues depend on market prices — energy, capacity, ancillary services, and bilateral Power Purchase Agreements (PPAs).

In competitive markets, generator revenues are largely determined by wholesale electricity markets built around locational marginal pricing (LMP) — a pricing mechanism that reflects both the marginal cost of generation and the cost of transmission congestion at specific grid locations.

The AI boom has increased demand for reliable 24/7 power. Hyperscalers such as Microsoft, Google, and Amazon are actively seeking long-term power purchase agreements (PPAs) to secure supply.

B. Transmission — The High-Voltage Highway

High-voltage transmission lines move bulk power across long distances.

Because parallel systems are economically irrational to build, transmission is a natural monopoly and is rate-regulated. Federal regulators oversee interstate transmission and wholesale market rules, while permitting and construction often fall to states and local authorities — one reason large transmission projects can take a decade or more to complete.

C. Distribution — The Last Mile

Distribution networks step voltage down and deliver electricity to end users — homes, commercial buildings, factories, and data centers. Like transmission, distribution is a natural monopoly, regulated at the state level by Public Utility Commissions (PUCs).

Large new electricity consumers such as hyperscale data centers often require significant upgrades at the distribution level — including substations, feeders, and transformers — before power can be delivered.

D. Retail Supply — The Billing Relationship

In states with retail competition, customers can choose their electricity supplier. The local utility still delivers the power; it simply charges a separate "wires" fee. In non-competitive states, the local utility provides bundled service from generation through billing.

3. Two Business Models, Two Investment Theses

The U.S. electricity sector is not governed by a single national framework — regulatory architecture varies significantly by region, and that variation defines the investment landscape.

Most infrastructure is privately owned but operates under extensive federal and state regulation: private capital finances and operates critical infrastructure, while regulators define the rules that determine returns.

Model 1: Vertically Integrated Utilities (The Traditional Model)

A single utility owns generation, transmission, distribution, and retail supply within a defined service territory. If you live in Georgia or the Carolinas, you have one utility, one bill, one phone number to call. Your rates are stable and predictable — but you have no choice of supplier and no ability to shop around.

The business model is straightforward:

• Capital expenditures form a "rate base" upon which a regulator-approved return is earned.

• Revenue stability is high; earnings volatility is low.

• Growth is driven by capital investment — building more infrastructure means earning more.

In effect, much of the investment risk is socialized across ratepayers through regulated tariffs, allowing utilities to earn relatively stable returns on approved capital expenditures.

Utilities in these markets must demonstrate the need for new resources through Integrated Resource Plans (IRPs) — a process that, while slow, provides investment visibility and reduces stranded asset risk. The Southeast and parts of the West are the heartlands of this model.

💡 Investment Logic: In vertically integrated states, a new data center translates directly into sanctioned capital spending — on new generation and grid infrastructure — with predictable, regulated returns.

Model 2: Restructured / Deregulated Markets (The Competitive Model)

Generation is competitive; transmission and distribution remain regulated. If you live in Texas or Pennsylvania, you can shop for your electricity supplier the same way you shop for a phone plan — different prices, different contract lengths, different green energy options. Your delivery charges stay fixed, but your energy supply rate can vary.

Independent power producers sell into wholesale markets organized by RTOs/ISOs: PJM (Mid-Atlantic/Midwest), MISO (Midwest/South), CAISO (California), SPP (Great Plains), NYISO (New York), ISO-NE (New England), and ERCOT (Texas).

Returns can be higher but are significantly more volatile, depending on electricity prices, capacity markets, and transmission constraints.

4. ERCOT — The Exception That Proves the Rule

Texas's ERCOT is the most unusual market structure in the country — and the most relevant for investors tracking AI-driven load growth.

ERCOT differs from most other U.S. markets in several ways:

1. It operates largely within Texas and is only weakly connected to other U.S. grids

2. It uses an energy-only market design rather than a centralized capacity market

3. It supports extensive retail competition

Instead of a capacity market, ERCOT relies on scarcity pricing with electricity prices allowed to spike sharply during periods of tight supply. Texas households saw electricity spot prices spike to hundreds of dollars per MWh during Winter Storm Uri in 2021 — a direct consequence of the energy-only market design that normally keeps Texas power cheap.

ERCOT has become the dominant destination for new data center load. The numbers are striking: ERCOT's current peak load is approximately 86 GW. Queued data center interconnection requests have exceeded 59 GW in just the Dallas-Fort Worth and West Texas service territories alone — the majority served by Oncor, the regulated transmission and distribution utility.

5. The AI Load Wave — Mapping Demand to Investment Opportunity

The proliferation of AI infrastructure is creating a step-change in electricity demand. Data centers require firm, 24/7 power — a demand profile that stress-tests both generation adequacy and grid delivery capacity.

The investment implications vary sharply by market structure.

Vertically Integrated States: The Clearest Path to Regulated Returns

In regulated, vertically integrated markets — particularly the Southeast — new data center load maps cleanly onto sanctioned capital investment.

The utility files an IRP, receives regulatory approval to build or procure new generation and upgrade grid infrastructure, and earns a regulated return on that capital. The revenue visibility is high; the execution risk lies in regulatory approval timelines and construction costs.

RTO/ISO Markets: Higher Complexity, Greater Return Dispersion

In competitive markets, new load drives locational marginal prices (LMPs), congestion rents, and capacity market signals — but the transmission and interconnection queue is often the binding constraint. The winners in these markets tend to be:

• Owners of flexible, well-located generation assets (fast-response gas peakers, battery storage, existing nuclear)

• Transmission and distribution utilities that serve high-growth load pockets

• Developers with proven interconnection expertise and speed-to-market advantages

Texas (ERCOT): Speed-to-Market Premium

ERCOT offers relatively fast interconnection timelines and a favorable development environment.

Oncor is the only company that owns and operates the electricity delivery network across Dallas-Fort Worth and West Texas. Its tracker/rider mechanism — which allows capital recovery on approximately 97% of CAPEX with minimal regulatory lag — makes it one of the most financially efficient T&D(Transmission & Distribution) investments in the country.

6. The Real Bottleneck — and Where the Durable Value Is

The critical insight for investors is this: the challenge of powering the AI economy is not primarily a generation problem.

The U.S. has substantial generation capacity, and new capacity is being developed rapidly. The true constraints are:

• Interconnection queues: the line to get new resources connected to the grid now stretches years in most markets

• Transformer and switchgear supply chains: lead times on large power transformers have extended to three or more years in some cases

• Transmission permitting and construction: siting high-voltage lines across multiple jurisdictions remains painfully slow

The investment hierarchy, in descending order of earnings certainty:

Tier 1 — Regulated Transmission & Distribution Infrastructure

Companies like Oncor (owned by Sempra Energy, NYSE: SRE), Duke Energy (NYSE: DUK), Southern Company (NYSE: SO), and similar regulated utilities earn predictable, regulator-sanctioned returns on growing rate bases. New load = new capex = new rate base = higher earnings. The regulatory compact insulates them from commodity price risk and competitive dynamics.

Tier 2 — Electrification Equipment and Grid Services

Transformer manufacturers, switchgear producers, grid engineering and construction firms benefit from the capex cycle — but their earnings are more sensitive to order flow timing, supply chain conditions, competitive intensity, and valuation multiples. Representative names include Eaton (NYSE: ETN), which has invested over $1 billion in North American transformer and switchgear manufacturing capacity since 2023, and GE Vernova (NYSE: GEV), spun out of GE in 2024 with a grid solutions division covering transformers, switchgear, and HVDC systems — both directly leveraged to the grid upgrade cycle stories.

Tier 3 — Unregulated / Merchant Generation

Companies like Vistra (NYSE: VST) own unregulated nuclear and gas assets in PJM and ERCOT. The bull case rests on securing long-term power purchase agreements (PPAs) with hyperscalers at premium prices — a real and growing opportunity. But current valuations already embed significant AI-demand optionality, and these assets are exposed to headline risk if data center buildout disappoints or interconnection bottlenecks persist.

Bottom Line

The U.S. power grid is not a simple market. It is a mosaic of regulatory regimes, ownership structures, and market designs that produce very different investment dynamics across regions.

In this environment, the most reliable path to capturing the AI infrastructure buildout is to own the regulated wires — the physical infrastructure that every data center must connect to, regardless of which generator wins the contract.

Generation competition is real. Energy market volatility is real. But the toll road always gets paid.