From Hype to Heavy Assets: Is the Wind Shifting?

Executive Summary: A Regime Shift in Motion

Early 2026 increasingly resembles a structural regime transition rather than a conventional cyclical correction. The S&P 500 remains modestly positive year-to-date (+1–2%), yet that surface stability obscures one of the most pronounced internal dispersions of the post-pandemic era. What appears calm at the index level is, in fact, a reordering of capital allocation priorities.

The market is recalibrating how it prices durability, competitive moats, and terminal growth assumptions in an AI-maturing environment. The narrative is shifting from AI as a disruptive threat to AI as a pragmatic enabler. In parallel, capital is rotating away from asset-light, long-duration growth models and toward balance-sheet strength, tangible scarcity, and low obsolescence — what we frame as the HALO paradigm.

This is not merely a sector rotation. It is a repricing of duration risk.

1. Structural Divergence Beneath Surface Stability

Recent price action echoes prior inflection points — the late-1990s concentration buildup or the 2018–2019 late-cycle broadening. While the S&P 500 has traded sideways in recent months, high-growth segments have underperformed value by roughly 23% on a relative basis. The Russell 2000 has advanced more than 5%, and cyclical sectors including Energy, Materials, and Industrials have posted gains ranging from the low teens to the mid-20% over the past year. Meanwhile, software-focused names have experienced double-digit declines in a matter of weeks.

This pattern does not signal collapsing risk appetite. Rather, it reflects a deliberate redistribution of it.

Capital is exiting asset-light, high-duration business models — those most exposed to AI-driven margin compression and accelerated obsolescence — and reallocating toward companies whose competitive positioning is anchored in physical infrastructure, balance-sheet resilience, and embedded operational ecosystems.

The index-level calm masks a deeper repricing of competitive durability. Software moats that were treated as structurally defensive during the 2022–2024 AI enthusiasm cycle are now being stress-tested under a more disciplined framework.

2. AI: From Disruption Narrative to Integration Reality

The catalyst for this rotation lies in the maturation of the AI narrative itself.

Initial selling was driven by renewed anxiety around agentic AI and its potential to commoditize software, compress terminal margins, and shorten duration for asset-light models. Markets priced in displacement risk aggressively.

However, accumulating micro-level evidence from earnings releases and product deployments suggests AI is increasingly functioning as an augmentation layer rather than a wholesale replacement technology.

ServiceNow, despite trading roughly 60% below its January 2025 peak amid disruption fears, delivered 21% subscription revenue growth in Q4 2025 and maintained a 98% renewal rate. These metrics point to embedded demand and workflow stickiness rather than erosion.

Intuit began transforming into an AI-driven platform as early as October 2019, leveraging decades of proprietary TurboTax and QuickBooks data to develop domain-specific models and deploy AI agents capable of executing real-world tax and accounting workflows for SMEs. The result has been a strengthening of data network effects — a moat difficult for entrants to replicate without comparable data depth.

Adobe’s valuation compression to below 16x GAAP earnings reflects pervasive anxiety. Yet analysts project revenue reaching $30.6 billion by 2028, implying approximately 9% annualized growth. Limited reinvestment needs enable robust buyback activity, underscoring capital return discipline.

Similarly, following Anthropic’s enterprise AI demonstrations, stocks such as FactSet rallied as investors began interpreting AI tools as orchestration layers that enhance existing data ecosystems rather than supplant them.

The emerging pattern is clear:

Platforms with deep proprietary data, high switching costs, entrenched customer workflows, and demonstrated AI integration capability are resilient. Horizontal or commoditized software lacking differentiated data advantages faces sustained margin pressure and multiple contraction.

The AI trade is not collapsing — it is discriminating.

3. The HALO Framework: Repricing Durability

In parallel, markets are increasingly applying what can be termed the HALO framework — Heavy Assets, Low Obsolescence — as the dominant lens for pricing durability.

Over the past year, capital-intensive sectors have materially outperformed AI-disruption-exposed themes. In an environment where AI rapidly compresses marginal differentiation in software, physical networks and infrastructure — pipelines, utilities, railroads, telecommunications towers, energy assets, and robotics systems embedded in real-world environments — are acquiring genuine scarcity value.

Capital intensity, once penalized during the zero-interest-rate era as a return drag, is increasingly recognized as a form of structural defensibility against technological churn.

Serve Robotics’ acquisition of Diligent Robotics illustrates this dynamic. Moxi robots have completed more than 1.25 million hospital deliveries across over 25 facilities nationwide. These systems represent integrated ecosystems of hardware, compliance, logistics, maintenance, and operational data — not easily replicated through code alone. AI enhances routing, reliability, and efficiency; it does not render the physical infrastructure redundant.

Critically, HALO should not be interpreted as a repudiation of AI exposure. In our view, HALO represents a hedge leg against AI uncertainty — not a substitute for AI participation.

Heavy-asset franchises are increasingly AI-enabled. They leverage AI to optimize utilization, predictive maintenance, routing, and cost structures. HALO therefore functions as a complement to AI positioning: it dampens disruption risk while preserving exposure to AI-driven efficiency gains.

The post-2010 playbook reflexively rewarded capex as growth. Today, incremental investment is treated as return dilution unless it embeds durable optionality within tangible assets that benefit from AI enablement without being fully substitutable by it. This inversion of capital allocation logic lies at the heart of the regime shift.

4. Macro Policy Tailwinds and Positioning Dynamics

The macro backdrop reinforces this structural broadening.

The Federal Reserve’s pivot toward growth stabilization, combined with fiscal measures such as accelerated depreciation and R&D expensing, lowers the effective cost of capital for domestic cyclicals and small- to mid-cap companies. Infrastructure spending and reshoring initiatives are generating record order backlogs across industrial and materials sectors.

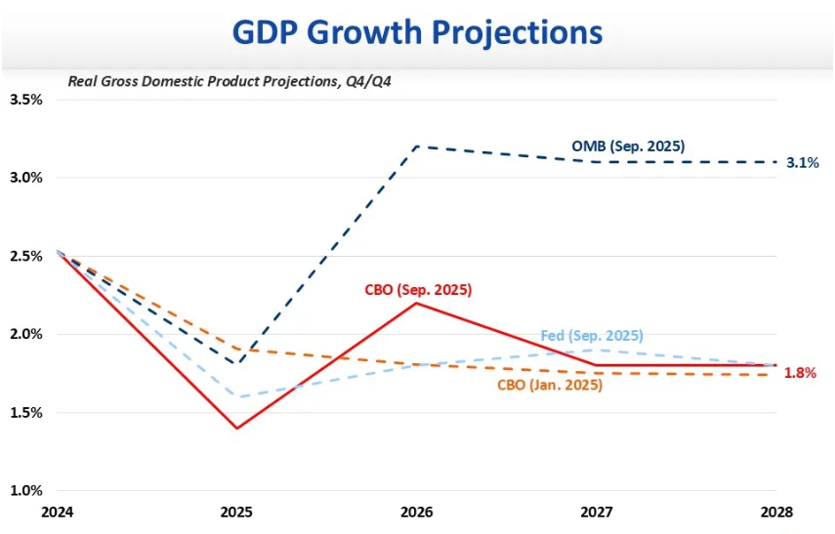

The Congressional Budget Office projects real GDP growth of 2.2% in 2026, moderating to roughly 1.8% thereafter — a trajectory consistent with steady expansion rather than disruption-driven volatility.

From a positioning standpoint, hedge fund exposure to semiconductors and direct AI beneficiaries sits near multi-year highs, while software and AI-disrupted baskets hover near historical lows. Speculative long exposure has declined for consecutive weeks, crowding metrics have moderated, and corporate buybacks are poised to re-enter post-blackout.

Extreme dispersion amid easing macro conditions typically signals positioning stress rather than economic deterioration — a dynamic often preceding leadership transitions.

The central question remains whether this represents cyclical mean reversion or the early stage of a multi-year regime shift.

The balance of evidence — earnings resilience among data-rich incumbents, sustained outperformance of capital-intensive sectors, supportive policy, and positioning extremes — tilts toward the latter.

The AI trade is not vanishing. It is maturing.

The first phase rewarded exposure and narrative momentum. The current phase rewards balance-sheet strength, pricing power, tangible scarcity, disciplined capital allocation, and the ability to harness AI as an efficiency multiplier rather than a disruptor.

Capital intensity is no longer dead weight. In an environment where digital advantages can erode quickly, tangible infrastructure embeds real optionality.

Conclusion: Positioning for the Transition

During this transition, positioning should emphasize HALO durability — cyclicals, infrastructure proxies, and resilient software incumbents integrating AI effectively — while remaining prepared to re-engage high-quality growth names once panic selling exhausts and breadth strengthens.

Regime shifts rarely resolve in weeks. They unfold over quarters — sometimes years. Those who adapt early to the new pricing paradigm tend to be rewarded.

The wind is not leaving Silicon Valley. It is broadening the landscape.