Private Credit: Check Under the Hood

Private Credit: Check Under the Hood

After the stress test — what broke, what held, and where the next chapter is being written

Prelude

In 2023, in our piece Private Credit — The Hidden Growth Engine (Nov 2023), we described private credit as a hidden growth engine — a $1.5 trillion market still misunderstood by most investors, quietly filling the financing vacuum left by post-2008 bank regulation. In October 2025, we returned to the subject in Private Credit Market in US: Winter or Winning?, asking the harder question — and flagging the cracks appearing in the market's most visible stress events: the collateral that simply vanished in the First Brands and Tricolor collapses, the governance failures, the opacity of structures that had grown faster than the frameworks meant to monitor them.

Six months on, the stress test has run. Not to its conclusion — these cycles rarely resolve cleanly — but far enough that the results are no longer speculative. We know more now about what breaks under pressure, what holds, and where the next chapter of this market is actually being written.

What Has Actually Broken

Start with the honest assessment. Private credit is facing real stress. A series of high-profile defaults in late 2025 — not isolated incidents but a pattern — suggested that years of loose underwriting, compressed spreads, and optimistic growth assumptions had created vulnerabilities that the market had been reluctant to fully acknowledge.

The headline default rate had stayed below 2% for several years, which many market participants cited as evidence of resilience. But that figure could be misleading. Once selective defaults, distressed exchanges, covenant amendments, and debt restructurings dressed up as something else are included, the true default rate has been running closer to 5%. That is not a crisis reading — yet the gap against the headline is difficult to dismiss.

Payment-in-kind, or PIK, has become the market's most visible stress signal. PIK provisions allow borrowers to defer cash interest payments, adding the unpaid amount to the principal balance. They were originally a feature of riskier mezzanine and subordinated debt — an acknowledgment that certain borrowers needed flexibility in exchange for higher eventual returns. What has changed is where PIK is now appearing. It has migrated into senior secured loan documentation, the part of the capital structure that was supposed to be insulated from exactly this kind of pressure. Public Business Development Company (BDC) portfolios now receive roughly 8% of investment income via PIK. That number is not catastrophic. But the direction of travel matters.

The regulatory world has also arrived. In early May 2026, the Financial Stability Board published its first dedicated vulnerability assessment of the private credit market. The document is measured in its language, as such reports tend to be. But its core finding is pointed: this is an asset class that has never been tested through a complete credit cycle at its current scale, and the interconnections between private credit funds, the banks that finance them, and the institutional investors that hold them are less well understood than the headline numbers suggest.

This is not a warning that the system is about to collapse. It is something more specific and, in some ways, more useful: an acknowledgment that the market has been operating in a period of extended benign conditions, and that the assumptions baked into that period need to be revisited.

Why This Is Not 2008

The comparisons to the financial crisis are understandable. Opaque structures, concentrated exposures, interconnections that are difficult to map — these are features that characterize both moments. But the comparison breaks down quickly when you look at the actual mechanics.

The 2008 crisis was fundamentally a liquidity crisis in highly leveraged, short-funded structures. When confidence evaporated, the funding dried up overnight. Private credit funds, by contrast, are closed-end structures for the most part. The capital is locked up. There is no equivalent of the money market run that froze credit markets in 2008. The semi-liquid retail vehicles that have attracted scrutiny are a real concern, but a contained one: they sit at the periphery of the market, not at its core.

Where the numbers get more uncomfortable is at the smaller end of the market, and in portfolios with concentrated exposure to software and technology. Software represents 20.8% of private credit portfolios based on public Business Development Company (BDC) data — a figure that rises further when broader technology and business services are included. For context, that same exposure in the high-yield bond market sits at roughly 5%. The question of what AI disruption does to the revenue assumptions embedded in 2021 and 2022 vintage software loans is not hypothetical. It is happening now, in real portfolios, with real consequences.

The more honest framing is that private credit is experiencing its first real credit cycle — a process of sorting that every mature asset class goes through, and that this one has been postponed by years of favorable conditions. What is happening now is not collapse. It is differentiation. And differentiation, uncomfortable as it is for managers with weaker portfolios, is exactly what a healthy market needs.

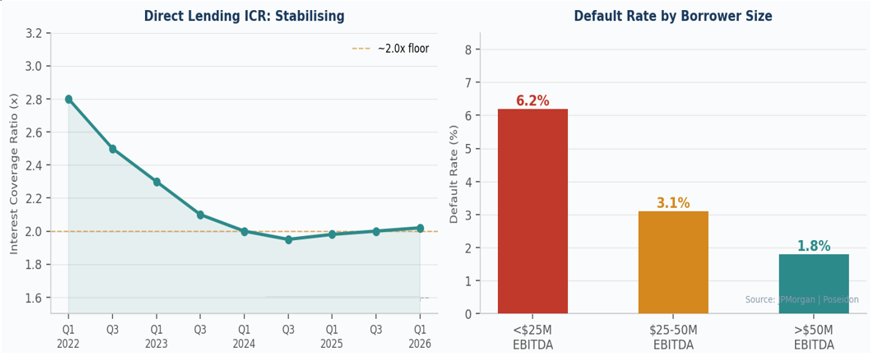

The data supports this interpretation. At the macro level, interest coverage ratios for direct lending have stabilized at around 2x after the initial shock of the 2022 rate cycle. That is below public market levels — public borrowers typically run at around 4x — but it reflects a risk premium that investors have historically been compensated for. Default rates for borrowers with more than $25 million in EBITDA have remained materially lower — at 3.1% for the $25–50M bracket and 1.8% above $50M — which is the segment where most of the institutional capital is actually deployed.

Where the Next Chapter Is Written

It would be a mistake to read the current stress as the end of the private credit story. The structural case for the asset class — banks retreating from middle market lending under regulatory pressure, the genuine financing gap that private lenders fill, the floating-rate protection against inflation — remains intact. What is changing is which parts of the market are the most compelling, and where the next cycle of growth is being built.

Asset-Based Finance: The Quiet Compounder

Asset-based finance — lending secured against specific, tangible assets rather than cash flow projections — has been growing steadily in the shadow of the direct lending boom. The addressable market is enormous: infrastructure loans, equipment finance, trade receivables, residential and commercial mortgages, consumer credit pools. The total opportunity has been estimated at over $30 trillion globally, of which private credit has captured a fraction. The characteristics are different from corporate direct lending: the underlying assets have intrinsic value independent of the borrower's operating performance, the AI disruption risk that is pressuring software-heavy direct lending portfolios is largely absent, and the illiquidity premium remains structurally justified. Several of the largest alternative asset managers have explicitly flagged ABF as their highest-conviction growth area for the next several years.

European Private Credit: Structural Tailwinds, Less Competition

European fundraising for private credit surged in 2025, and market participants increasingly describe the shift in allocator interest toward the continent as structural rather than cyclical. The reason is straightforward: Europe remains a bank-dominated lending market, with banks accounting for roughly 70% of total lending. The implementation of Basel IV over the coming years will replicate, at least partially, the regulatory dynamic that drove private credit's growth in the US after 2008. Defense spending commitments and infrastructure buildout across European governments have created a specific origination opportunity that several major managers have now explicitly entered. The spreads available in European private credit continue to offer a premium to comparable US deals — a reflection of a market that is less picked-over, not less creditworthy.

Credit Secondaries: The Discount Window

The growth of semi-liquid retail vehicles created a structural tension that was always latent and has now become visible. These were funds that offered quarterly redemptions while holding illiquid underlying assets; when redemption pressure arrived, the mismatch could not be managed quietly. Several large managers have faced exactly that pressure over the past twelve months.

For patient investors, that dislocation has produced something valuable: the availability of fund interests at discounts to net asset value. Credit secondaries, once a niche within a niche, have become a legitimate sub-strategy, with dedicated credit secondaries funds raising close to $40 billion in 2025 alone — nearly double the share of total secondaries capital compared to two years prior. The entry basis matters enormously in credit. Buying a well-constructed private credit portfolio at a 10–15% discount to NAV is a fundamentally different proposition from buying the same portfolio at par.

What Investors Should Examine

What follows is not a list of fund recommendations. It is a framework — a set of dimensions that matter now in ways they simply did not when conditions were uniformly forgiving. For any private credit allocation, these are the questions worth asking seriously.

Borrower size. Stress is concentrated in portfolios with heavy small-borrower exposure. Sub-$25M EBITDA companies have shown materially higher default rates than their larger counterparts, while funds focused on sponsor-backed middle market businesses with established operating histories have held up comparatively well. This is not a guarantee — but in the current environment, it is a genuine differentiator.

Sector concentration. Software at roughly 21% of a private credit portfolio is a fundamentally different risk proposition from software at 5% in the high-yield bond market. Managers with diversified sector exposure and deliberate underweights to the subsectors most vulnerable to AI disruption, are better positioned for the next 18 months than those who built their books during the SaaS boom years.

PIK discipline. PIK is not inherently a red flag — in growth-oriented lending structures, it can be a legitimate feature. But a rising PIK ratio across a portfolio warrants serious investigation. It signals that borrowers are struggling to service debt in cash, and the compounding effect on eventual principal repayment is consistently easier to underestimate than to model accurately.

Restructuring capability. The managers who emerge strongest from this cycle will be those with genuine workout experience — the legal, operational, and negotiating infrastructure to manage distressed situations effectively, not just the marketing language to describe it. This capability is easy to claim and hard to verify without examining track records across prior cycles in detail.

Structure type. Closed-end institutional vehicles and semi-liquid retail products are meaningfully different risk propositions in a stressed environment. Understanding which structure you are in — and what happens to the portfolio if redemptions accelerate — is the kind of basic due diligence that years of benign conditions made easy to skip.

Vintage exposure. Portfolios with significant 2021–2022 vintage concentration face a compounding challenge: the rate shock and AI disruption arrived together, and both bear directly on the underwriting assumptions of that era. Asking a manager what percentage of their book is pre-2023 vintage, and how those positions are tracking against original underwriting, is a straightforward question that remains conspicuously absent from most due diligence processes.

Conclusion

The windfall conditions are behind us. Direct lending yields are normalizing toward the high single digits — still a meaningful premium over public credit, but no longer the 12–14% that attracted capital poorly suited to the asset class. That normalization is, in the end, a healthy one. Those who remain in private credit are here for the right reasons: illiquidity premium, floating rate protection, senior secured positioning.

Open questions remain. The Financial Stability Board's recent vulnerability assessment was a first word, not a final one. Peak-vintage loans in software-heavy portfolios have not yet fully worked through the system. Regulatory scrutiny of the asset class is deepening, not receding. These are not reasons to exit the asset class — they are reasons to be precise about where within it you are positioned, and why.

Three pieces in three years. In 2023, we called private credit an underappreciated engine. In 2025, we asked whether it could survive its first real test. In 2026, the answer is clear: the engine still runs. But the vehicles on the road are not all in the same condition. Knowing the difference is, at this point, the entire game.