The World's New Maps I: From Oil Exporter to Strategic Crossroads

Globalization is not disappearing. It is being redrawn.

For three decades, companies built supply chains around efficiency: low-cost production, lean inventories, just-in-time delivery and global specialization. That model created enormous scale. It also created fragile dependencies. The pandemic, Russia’s invasion of Ukraine, Red Sea shipping disruptions, technology restrictions and rising industrial policy have all exposed the same weakness: the world’s supply chains were optimized for cost, not resilience.

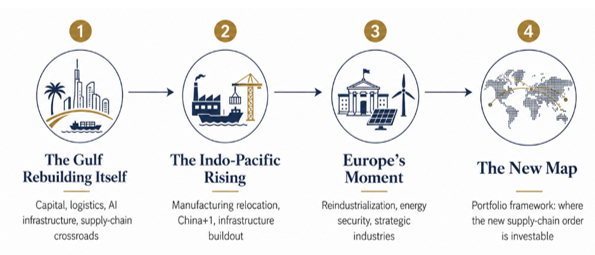

This series looks at the regions now trying to benefit from that shift. The Gulf is using sovereign capital and infrastructure to reposition itself between Asia, Europe and Africa. The Indo-Pacific is becoming the center of manufacturing relocation and industrial upgrading, from India to Japan. Europe is attempting to rebuild strategic capacity in energy, defense, semiconductors and heavy industry. The final piece will bring these regions together into a portfolio framework: where the new supply-chain map is investable, where the risks are overstated, and where investors should remain cautious.

The objective is not to predict the end of globalization. It is to understand its next version. Trade is still growing. UNCTAD expects global trade in goods and services to exceed $35 trillion in 2025 for the first time, up around $2.2 trillion from 2024, even as geopolitical tensions, policy shifts and higher costs complicate the outlook. The lesson is straightforward: global commerce is not shrinking, but its routes, partners and strategic logic are changing.

This first piece starts in the Gulf — a region still associated with oil, but increasingly trying to become something more: a supply-chain middle layer for capital, energy, logistics, compute and trade.

For clarity, the “Gulf” in this article mainly refers to the Gulf Cooperation Council (GCC): Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Bahrain and Oman. Saudi Arabia is the largest economy and landmass in the group. The UAE is a federation of seven emirates, including Abu Dhabi and Dubai. They are not the same country, and their economic models differ. But from a geographic and commercial point of view, they share a crucial position around the Arabian Gulf, near the energy, shipping and trade routes linking the Indian Ocean, the Red Sea, the Mediterranean and Europe.

For decades, investors looked at the region through a narrow lens: oil prices, shipping chokepoints, fiscal breakevens and geopolitical risk. That lens still matters. The Strait of Hormuz remains one of the world’s most important energy arteries. Gulf budgets still move with crude. Regional politics can reprice risk overnight.

But that is no longer the whole story.

Behind the familiar oil-market narrative, the Gulf is trying to build a new economic operating system. The region is deploying sovereign capital into logistics corridors, ports, airports, industrial zones, mining, artificial intelligence infrastructure and domestic capital markets. The goal is not simply to diversify away from oil. It is to make the Gulf more necessary to a world where supply chains need alternatives.

That distinction matters. Diversification stories often disappoint because they are measured against ambition. Supply-chain stories can be measured against function. Does a region reduce transit risk? Does it provide alternative routing? Does it offer capital, power, land, ports, data centers, industrial policy and political alignment in one package? Increasingly, the Gulf’s answer is yes.

From “Just in Time” to “Just in Case”

The old model of globalization was built on a simple assumption: the most efficient supply chain was usually the best one. Production moved to the lowest-cost location. Inventory was minimized. Logistics networks were optimized for speed and price. A smartphone could be designed in California, assembled in China and filled with components from Taiwan, Japan, South Korea, Germany and Malaysia.

That system did not collapse. It was exposed.

“Just in time” means keeping inventories low and relying on precise delivery schedules. It works when borders are open, ports function smoothly and politics remains in the background. “Just in case” means accepting higher costs to build backup suppliers, routes and inventories. It is less elegant, but more durable.

The pandemic revealed single points of failure in medical equipment, semiconductors, pharmaceuticals and industrial inputs. The war in Ukraine disrupted energy and food flows. Red Sea shipping disruptions reminded companies that maritime geography still matters. The new corporate question is not only “where is it cheapest?” It is “what happens if that route closes, that supplier is sanctioned, that port is delayed, or that border becomes political?”

This is the environment in which the Gulf’s long-term infrastructure push becomes more relevant. Supply-chain redundancy — the use of alternative suppliers, ports, routes and inventories so that one disruption does not halt the entire chain — is no longer only a logistics concern. It is becoming part of national industrial strategy.

Strategy& argues that logistics is now high on the GCC agenda as a growth engine, but that regional providers need to build “supply chain density” along prioritized trade routes where they have a genuine right to win. In plain English, this means the Gulf cannot simply build more ports and warehouses. It must build enough connected activity along specific routes to make companies want to use the region as a default trade platform.

That is the frame through which Vision 2030 should be judged. Not as a collection of futuristic renderings. Not as a tourism campaign. Not even simply as an oil-diversification plan. It is better understood as an attempt to build the physical and financial infrastructure of a more fragmented world.

Vision 2030: Less Fantasy, More Execution

Saudi Arabia’s Vision 2030 is often described in extremes. Supporters present it as an unstoppable modernization program. Critics focus on the delays, cost overruns and scale-backs around NEOM and other giga-projects. Both views contain part of the truth. Neither is sufficient.

Giga-projects are extremely large, state-backed development projects, often combining real estate, tourism, infrastructure and industrial policy. They are highly visible, but they are not the whole story. The more useful assessment is this: Vision 2030 has moved from the era of maximum ambition to the era of capital discipline.

Capital discipline means prioritizing projects that can generate economic returns or strategic value, rather than funding every announced ambition at once. That shift is important. A strategy that tries to build everything everywhere is difficult to underwrite. A strategy that concentrates capital on logistics, mining, AI infrastructure, tourism, aviation and financial markets is easier to assess.

The official scorecard is not trivial. Saudi authorities say 93% of national program and strategy indicators had met, exceeded, or were close to meeting their 2024 interim targets, with several 2030 targets reached ahead of schedule, including more than 100 million tourists and more than one million volunteers. Official Vision 2030 materials also describe 2026 as the beginning of the program’s third and final phase, focused on full delivery and sustaining impact beyond 2030.

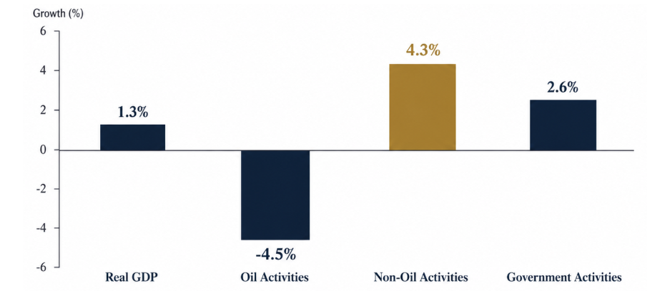

The macro data also show real change. Saudi Arabia’s statistics authority reported that real GDP grew 1.3% in 2024, despite a 4.5% contraction in oil activities. Non-oil activities grew 4.3%, while government activities rose 2.6%. In other words, the non-oil economy is no longer decorative. It is carrying the growth story when oil output is constrained.

The International Monetary Fund’s 2025 Article IV consultation reached a similar conclusion, noting Saudi Arabia’s resilience, expanding non-oil activities, contained inflation and record-low unemployment, while still flagging downside risks from uncertainty and commodity prices.

This does not mean Vision 2030 is risk-free. It means the story has become more complicated than the caricature. Some of the spectacle has been reduced. Some of the infrastructure remains. For investors, that distinction is critical.

The question is not whether every original rendering becomes real. The question is whether Saudi Arabia and its neighbors are building durable economic functions beyond oil. On that test, the evidence is stronger than it was five years ago.

The Sovereign-Wealth Pivot

The Gulf’s most important economic actors are not only ministries. They are sovereign investors.

Sovereign wealth funds are state-owned investment vehicles. In the Gulf, they are not only financial investors. They are also tools of national industrial policy. They decide which sectors receive long-term capital, which foreign partners gain local access and which domestic industries are expected to scale.

Saudi Arabia’s Public Investment Fund reported assets under management of $913 billion at the end of 2024, up 19% from the prior year. PIF also said cumulative investments in priority sectors had exceeded $171 billion since 2021. Its annual report emphasized a transition from digital transformation to digital leadership, with artificial intelligence and automation becoming central to operations.

That language is easy to dismiss as institutional branding. The investment pattern suggests otherwise.

In 2025, Saudi Arabia launched HUMAIN, a PIF-backed artificial-intelligence company designed to operate across the AI value chain. PIF said HUMAIN would provide next-generation data centers, AI infrastructure, cloud capabilities, advanced models and AI solutions. AI infrastructure means the physical layer behind artificial intelligence: data centers, power supply, cooling systems, chips, cloud platforms and fiber connectivity.

The UAE is moving in parallel. In 2025, G42, OpenAI, Oracle, Nvidia, SoftBank and Cisco announced Stargate UAE, a next-generation AI infrastructure cluster inside a planned 5-gigawatt UAE-U.S. AI campus in Abu Dhabi. OpenAI said the project includes a 1-gigawatt Stargate UAE cluster, with 200 megawatts expected to go live in 2026.

This is not a side story. AI infrastructure requires cheap and reliable power, land, capital, permitting speed, fiber connectivity, cooling capacity and political willingness to build at scale. The Gulf has several of those ingredients. It also has a strategic reason to move early: data centers and AI compute could become to the next industrial cycle what refineries and petrochemicals were to the last one.

Mining is another priority. Saudi Arabia’s official mining strategy describes the sector as a pillar of national industrial development. The logic is clear: an economy trying to build electric vehicles, batteries, defense supply chains, industrial equipment and advanced manufacturing needs access to minerals and processing capacity, not just oil revenue.

The pattern is increasingly visible. Gulf sovereign funds are not simply buying trophy assets abroad. They are trying to manufacture strategic ecosystems at home. The current map points toward AI infrastructure, logistics, mining, industrial localization, aviation, clean power, tourism and financial-market deepening.

For investors, this makes Gulf sovereign funds a signal. Where PIF, Mubadala, ADQ, ADIA and QIA deploy capital is not merely a portfolio decision. It is a roadmap of the sectors Gulf governments want to scale.

The Gulf as a Trade Crossroads

The most underappreciated part of the Gulf story is logistics.

The region’s geography has always been useful. What is changing is the scale of deliberate investment around that geography. The GCC sits between Asia, Europe and Africa. It has deepwater ports, large airports, free zones, energy infrastructure, industrial land and sovereign capital. In a world looking for alternative routes and regional redundancy, that combination has value.

A Gulf Research Center report argues that the GCC transportation and logistics sector is being driven by non-oil economic expansion, infrastructure development, free trade zones, industrial parks and regional trade collaboration. It also notes the Gulf’s strategic position along the Asia-Europe trade route and its emergence as a hub in global commodity circulation.

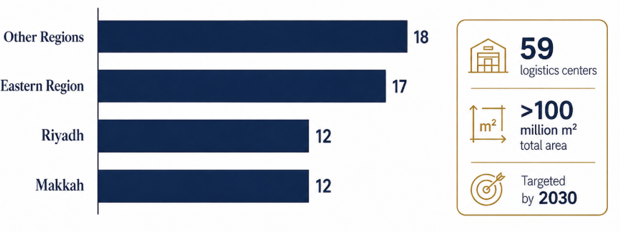

Saudi Arabia is building into that thesis. The kingdom’s master plan for logistics centers calls for 59 centers with more than 100 million square meters of total area, including 12 in Riyadh, 12 in Makkah, 17 in the Eastern Region and 18 elsewhere. The plan targets completion by 2030 and is explicitly tied to making the kingdom a global logistics hub.

The UAE already has a head start. Dubai’s Jebel Ali and Abu Dhabi’s Khalifa Port are not just ports. They are integrated trade platforms connected to free zones, industrial clusters, customs infrastructure, warehousing, aviation and financial services. Etihad Rail is adding another layer by connecting industrial and port infrastructure across the UAE.

This matters because supply chains do not reroute on narrative. They reroute on infrastructure. Companies need bonded zones, customs efficiency, multimodal connectivity, predictable regulation, storage capacity, financing, insurance, labor, digital visibility and political reliability. The Gulf is trying to package those inputs together.

PwC Middle East has argued that the GCC is entering a new phase of outward-looking growth, expanding trade agreements, deepening global value-chain integration and strengthening its position as a bridge between Asia, Africa and Europe.

That bridge function is the investable story. The Gulf does not need to replace China, India, Europe or the U.S. It needs to become more useful between them.

In the old globalization model, the Gulf exported energy and imported almost everything else. In the emerging model, it wants to export energy, capital, compute, logistics capacity, tourism, financial access and industrial services. That is a much broader proposition.

What Has Really Been Built

A fair scorecard should separate three categories: what has been built, what is still aspirational and what has been scaled back.

What has been built is meaningful. Saudi Arabia’s non-oil economy has expanded. Tourism has grown. Labor-market reform has changed the domestic workforce. Capital markets have deepened. PIF has grown into one of the world’s most consequential sovereign investors. Logistics-zone planning is no longer theoretical. AI infrastructure has moved from policy language into named vehicles and international partnerships.

What remains aspirational is also large. AI compute at global scale is not created by announcement. Mining ambitions require exploration success, permitting, processing capacity, water management and global customers. Logistics hubs need utilization, not just square meters. Tourism requires repeat demand, not only events and construction. Manufacturing localization requires productivity, skills and supplier depth.

What has been scaled back should not be ignored. Some giga-projects were launched with timelines and concepts that always looked stretched. That recalibration is not necessarily negative. In fact, it may be healthier than the alternative. The Gulf’s first phase of transformation was defined by ambition. The next phase will be judged by selection.

For investors, the key question is whether discipline lasts when oil prices recover, political priorities shift or global capital becomes cheaper again.

Our Thoughts: What Is Investable

The Gulf should not be treated as a single trade. It is a platform with several investable expressions, each with different risk and liquidity profiles.

The first is public-market access. Saudi Arabia’s Tadawul and UAE exchanges offer exposure to banks, utilities, telecoms, exchanges, logistics operators, petrochemicals, consumer companies and real-estate-linked names. The case is not that all Gulf equities are cheap or defensive. It is that the region’s listed markets are becoming a cleaner expression of non-oil policy execution than they were a decade ago.

The second is infrastructure. Ports, logistics parks, airports, rail, power, water, data centers and industrial zones are the backbone of the Gulf transformation. Many of these assets are not easily accessed directly by public-market investors. Global infrastructure funds, listed infrastructure vehicles and private-market managers with Gulf exposure may offer more practical routes.

The third is AI and power infrastructure. Investors should be careful with the hype. But the physical requirements of AI are real: power, cooling, land, fiber, chips, cloud platforms and data-center operations. The better investment question is not “which Gulf AI app wins?” It is “who provides the picks and shovels for sovereign-scale compute?”

The fourth is critical materials and industrial localization. Saudi Arabia’s mining strategy and the region’s broader industrial ambitions point to a long-term push into minerals, processing and advanced manufacturing. Execution risk is high, but the strategic logic is clear.

The fifth is global companies exposed to Gulf capital expenditure. Engineering firms, contractors, equipment suppliers, logistics-technology providers, data-center operators, chip companies, power-equipment manufacturers and consultants may all benefit from the region’s buildout without requiring investors to take direct local-market risk.

The main risk is that investors overpay for the theme. The Gulf’s transformation is real, but it is not linear. Oil still matters. Fiscal pressure still matters. Governance still matters. Execution capacity still matters. Geopolitical risk still matters. Currency pegs, labor-market constraints, regulatory opacity and project-level delays are not footnotes.

The right approach is not blind bullishness. It is selective exposure to the parts of the Gulf buildout that solve real problems for the global economy.

The New Middle Layer

The Gulf has spent much of the past decade trying to answer a question that became more urgent only recently: what does an energy exporter do in a world where energy is still essential, but no longer enough?

The first answer was diversification. Build tourism. Build cities. Build entertainment. Build capital markets. Build national champions.

The better answer is now emerging: build usefulness.

Useful to companies that need alternative supply-chain routes. Useful to countries that want energy security and industrial partnerships. Useful to technology companies that need power and land for AI infrastructure. Useful to miners and manufacturers looking for capital. Useful to investors looking for exposure to a region where state policy and capital deployment are unusually aligned.

This is why the Gulf story is not simply about oil, and not simply about moving beyond oil. It is about the region trying to reposition itself from commodity supplier to strategic intermediary.

The old Gulf exported hydrocarbons through narrow waterways. The new Gulf wants to intermediate trade, capital, compute, minerals, logistics and industrial policy across three continents.

That ambition will not be delivered exactly as advertised. Few national transformation plans are. Some projects will disappoint. Some will be delayed. Some will be quietly reduced. But enough has already changed to make the region difficult to ignore.

In a world where supply chains are becoming more regional, more political and more redundant, the Gulf is building for the map that comes next. For investors, the task is not to buy the vision wholesale. It is to identify which parts of the vision have become infrastructure.

The next piece moves east. If the Gulf is trying to become the middle layer of the new supply-chain map, the Indo-Pacific is where much of the production map is being redrawn. India is pushing to become a manufacturing alternative to China. Japan and South Korea remain critical technology and industrial anchors. Southeast Asia is absorbing factories, ports, electronics supply chains and data-center investment.

Together, they form the arc where “China plus one” is becoming something broader: a new manufacturing geography.

That is where the series goes next.