Private Credit Market in US: winter or winning?

Prelude

Private credits sound very technical but closely related to everyone in this world and mainly come from non-bank lenders: investment firms, specialized loan companies, or wealthy individuals. The most famous example would be that some mafia in the west primarily used private credit and union pension funds to secretly finance the construction of Las Vegas casinos from the 1940s to the 1970s. Today, private credits have become the cornerstones of modern credit system. However, the implosion of auto parts manufacturer First Brands and auto loan lender Tricolor seem remind us that private credit may not look “private” anymore.

From First Brands to Tricolor: What truly happened?

Auto parts manufacturer First Brands and subprime auto lender Tricolor have both filed for bankruptcy after the former has reported billions of dollars in loans "simply vanished. The collapse of two US firms, First Brands and Tricolor, has shone a light on private credit and its growing influence in the global economy. The failures have led to ballooning losses at traditional banks, and, coupled with worries about the health of US regional banks, have raised concerns about weak lending standards and potential threats from an opaque corner of the so-called shadow banking sector.

JPMorgan reportedly wrote off $170 million, and Fifth Third Bank disclosed $200 million in potential losses. Raistone, a trade finance creditor, alleges that $2.3 billion in collateral effectively vanished. Swiss bank UBS faces more than $500 million in exposure; Jefferies disclosed $715 million in receivables exposure. In each case, sophisticated creditors armed with advanced systems and compliance frameworks were blindsided by opaque privately structured financing arrangements. But the structures involved were nontraditional loans built within the sprawling $1.7 trillion private credit ecosystem: trade finance funds, supply-chain financing vehicles, and warehouse lines linked to securitizations.

The increasing opacity of these financing structures has led to a corollary collapse in collateral verification: Private credit has grown so fast that verification and audit frameworks haven’t kept up, leading to structural weaknesses across modern credit markets. Lenders are discovering that their control mechanisms, designed for more-transparent syndicated markets, don’t function in opaque financing ecosystems.

Is market evolving or circling around?

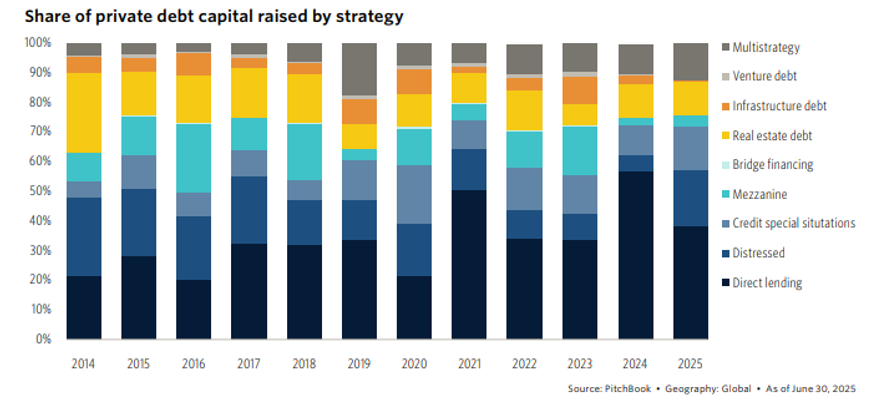

Private Credit or non-bank lending is when investment funds lend directly to companies instead of buying bonds or other securities that represent bank loans to companies. Blackstone Credit, one of the largest and most important funds, was founded in 2005, but the growth really starts after this regulation regime goes into effect. According to McKinsey and Company, the size of this asset class, “Totaled nearly $2 trillion by the end of 2023, roughly ten times larger than it did in 2009.” The growth of this sector is fueled by multiple factors like the growth of private equity. However, the sudden growth of private credit following the 2008 financial crisis and the subsequent regulation certainly fueled the growth of the private credit sector. Regulators achieved this goal in curbing excessive risk taking in the banking industry. This was epitomized by the success of conservative banks like JP Morgan and the sluggish growth of banks like Citigroup which were very aggressive before 2008.

However, there were some unintended side effects with banking’s newfound conservatism. A conservative banking culture led to a deficit between how much companies want to invest, and banks are willing to lend, leading to this deficit being filled by these new products. These new products have also had a clear impact on the systemic risk of the financial system. In investment funds, deposits are not federally insured and more prone to runs than bank deposits increasing the systemic risk of the financial system.

This poses a real and dangerous problem when these funds are non-insured and hold a large portion of people’s saving and business’ debt. For this reason, Shadow banks and non-bank financial institutions add unnecessary systemic risk across the financial system. This increased systemic risk could make financial downturns worse and cause credit to freeze up during downturns.

How is market going?

Private credit, which can offer floating interest rates that increase in tandem with benchmark rates, has seen significant growth in recent years and could become a $5 trillion market by 2029. Demand for private credit, which refers to lending to companies by institutions other than banks, has grown significantly in recent years. Unlike most bank loans, private credit solutions can be tailored to meet borrowers’ needs in terms of size, type or timing of transactions. Like bank loans, however, most of the private credit lending is in the form of floating-rate investments that change as rates change, providing real-time interest rate protection compared to investments like fixed-rate bonds. In addition, increased market volatility and bank lending regulations have helped fuel further growth in private credit in recent years, as some borrowers have flocked to its price certainty and speed.

Private credit has historically offered compelling performance in relation to other segments of the fixed-income market and leveraged finance. Over the last 10 years, when private credit began to grow in earnest, it has provided higher returns and lower volatility compared to both leveraged loans and high-yield bonds.

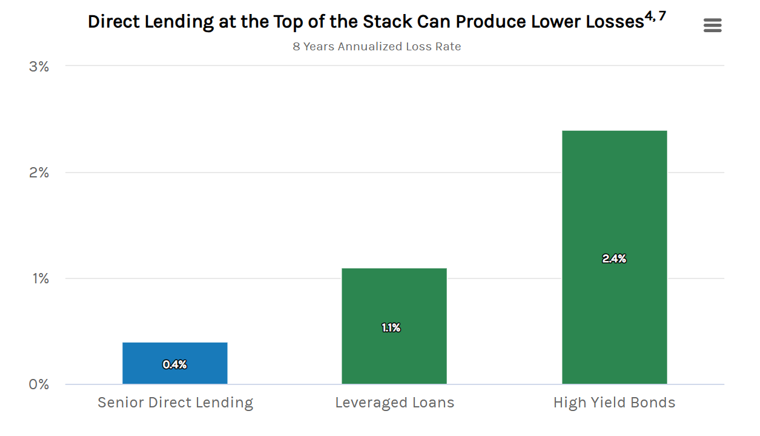

Private credit may also offer better risk management against losses. Privately held companies often do not have credit ratings or, if they do, are rated below investment grade. Direct lending can be more conducive to proactive engagement with borrowers. That, combined with a greater focus on senior secured loans, may produce lower credit losses relative to the broader leveraged finance space. Senior direct lending, for example, has sustained losses of 0.4% since 2017, compared to losses of 1.1% for leveraged loans and 2.4% for high-yield bonds.

Direct lending that stays true to a senior secured focus may do quite well in a soft economic landing aided by shallow rate cuts. Direct lending is highly geared to private equity deal flow, and lower rates are likely to stimulate that activity and demand for leveraged buyout loans. Significant pent-up demand and private equity dry powder that has built up over the years may create favorable lending conditions and pricing for direct lenders once fully released.

A proactive approach has become increasingly important, which includes closely analyzing companies’ earnings and free cash-flow generation considering the current economic and interest-rate environment. Private credit borrowers are typically domestically focused, but the impact from tariffs is another important overlay. Meanwhile, for companies, the primary focus is liquidity management. Borrowing costs have eased since the first set of Federal Reserve rate cuts in 2024 but remain significantly above levels preceding the inflation shock of 2022. To date, most borrowers have been able to successfully manage their liquidity.

How investors can navigate away from one pitfall and avoid the next.

Investors seek a return premium vs. traditional publicly traded credit for taking illiquidity risk and dealing with greater complexity. In other words, this is a premium sought by investors for the challenges of holding illiquid assets that cannot be quickly sold and for navigating bespoke loan structures requiring specialized manager expertise. However, we believe it is important to gain a comprehensive understanding of the risks and potential downside scenarios that may affect performance. To assess the relative value of private credit, consider the following more nuanced factors:

- Lender protections in the debt agreement – loan documentation is a critical aspect of private lending. Lenders can include specific requirements such as covenants to protect against borrowers or equity owner actions that may increase risk for them. Most of the broadly syndicated loan market lacks stringent financial maintenance covenants with 90% of the market containing no covenants.

- Ability to engage with management – private loans are directly originated, either held wholly by the originator, or in a small club typically made up of 2-5 managers. This concentrated lender group may create better alignment between borrower and lender and may provide greater flexibility to work with borrowers to address business issues which may occur. In syndicated markets, loan exposure can be distributed among potentially hundreds of lenders which may make engagement difficult or impractical in the event of a business issue.

- Third party valuations vs. market prices- The less-frequent third-party valuation of private credit is often viewed as a benefit to investors, as it typically stabilizes price performance, showing fewer potential distortions. Simultaneously, third party valuations focus primarily on the potential contractual cashflows. By comparison, continuous pricing in public markets can be distorted by a variety of factors including who owns the loans, whether the loan is included in an index, and potential price movement associated with large investors, such as collateralized loan obligations (CLOs). These differences reflect distinct market dynamics and valuation methodologies. Investors may want to carefully consider how these factors may impact the perceived stability or volatility of private credit versus publicly traded loans.

Conclusion and recommendations.

The private credit market presents a compelling opportunity for higher returns and lower volatility, but its rapid growth and structural opacity have created significant, systemic risks. As for investors, private credit investments are typically held to maturity and are not subject to the same daily mark-to-market volatility as public bonds and equities. This reduces overall portfolio volatility and helps provide a stable source of income during public market downturns. Also, private lenders could step into filling the financing gap left by the bank, which offers them access to a wide array of companies and projects—particularly small and medium-sized enterprises (SMEs)—that are not available in public markets.

In conclusion, if investors want to successfully navigate this landscape and avoid pitfalls, they should truly be fully prepared and deep dive into their homework. Therefore, they must move beyond just chasing illiquidity premiums but adopt a highly diligent, proactive approach focused on three critical areas: stringent loan documentation, active engagement with borrowers, and a deep understanding of the unique valuation methods.