US Power Series III - Ice and Fire: Bottleneck Beneath the Boom

Ice and Fire: Bottleneck Beneath the Boom

Backup generation, cooling, and what is behind Time-to-Power

This is Part 3 of the US Power Series. Part 1 mapped how America's electricity system actually works and why regulated wires are the cleanest way to monetize AI-driven load growth. Part 2 moved closer to the data center and explained why the binding constraint is no longer only generation, but the slower and harder-to-scale infrastructure between the transmission grid and the GPU: interconnection, substations, transformers, switchgear and campus power distribution.

Part 3 moves one layer deeper into the systems that decide whether a project can run, not just whether it can be announced: backup and bridge power, high-density cooling, and the public-market companies positioned around those bottlenecks. The recent NextEra Energy-Dominion Energy transaction is the clearest market signal yet that power access, large-load franchises and regulated rate-base growth have become strategic acquisition currency.

The core thesis is simple: Time-to-Power (TTP) is no longer just an engineering metric. It is an investable scarcity premium.

I. Backup Power Is Becoming Bridge Power

Historically, on-site generation in a data center was not meant to run every day. The grid was the primary source of electricity. The UPS (Uninterruptible Power Supply) carried the load for seconds or minutes, while diesel generators started and stabilized. Generators were insurance: expensive, essential, but normally idle.

That architecture is still the baseline for most facilities. Diesel remains hard to displace because it is proven, dispatchable, easy to test, and supported by a mature service network. For a mission-critical facility, reliability outranks almost everything else. A battery can respond faster, but a multi-day outage still requires stored fuel or another form of continuous generation.

The change in 2025 and 2026 is that on-site generation is moving from standby insurance to bridge power. A data center developer that faces a three-to-five-year grid interconnection delay can either wait, relocate, or bring power to the site. For AI training clusters, where hardware depreciates quickly and capacity commitments are time-sensitive, waiting is often the worst option. The result is a new class of data center power architecture: not fully off-grid forever, but grid-parallel, behind-the-meter, and designed to get capacity online before the public utility system can catch up.

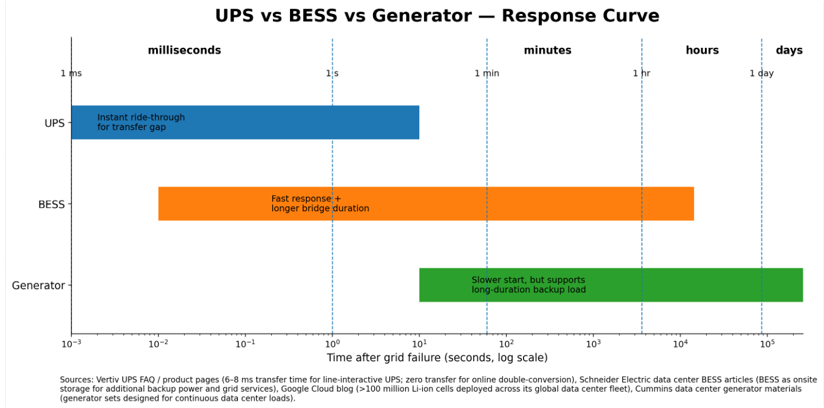

The resilience stack: different tools for different time horizons

UPS, BESS, and generators are often treated as substitutes. In reality, they are layers in the same resilience stack, each designed for a different failure duration.

This distinction matters because the market is increasingly paying for duration certainty. UPS systems protect milliseconds. Batteries protect seconds to hours. Generators and fuel cells protect hours to days and, in some configurations, can operate as prime power.

Natural gas is becoming the fast lane when the grid is not ready

The most important shift is the move from emergency diesel to gas-fired prime or bridge power. The Joule Capital Partners, Caterpillar and Wheeler Machinery agreement in Utah is a useful reference point. The project is designed to provide four gigawatts of total energy to a high-performance compute campus, using Caterpillar G3520K generator sets and combined cooling, heat and power (CCHP) solutions integrated with liquid-cooling architecture. That is not a traditional standby configuration. It is a distributed generation platform built around compute demand.

Bloom Energy sits on the same time-to-power (TTP) vector through a different technology. Bloom's SOFC (solid oxide fuel cell) systems can be containerized and deployed on-site, using natural gas infrastructure and providing modular power near the load. Oracle's expanded agreement with Bloom includes an initial 1.2 GW under contract and a master agreement supporting up to 2.8 GW of fuel cell capacity. Bloom also disclosed that it delivered a fully operational system to Oracle in 55 days, faster than the expected 90-day schedule. For a data center operator, that time difference can be worth more than marginal differences in levelized cost of energy.

The caveat is that gas-fired bridge power is not free of constraints. It needs gas pipeline capacity, air permits, local political acceptance and a credible decarbonization path for hyperscalers with net-zero commitments. Gas solves the grid access problem, but it can create a carbon, permitting and fuel-supply problem. That is why the best framing is not "gas replaces the grid." It is "gas buys time until the grid, transmission and long-lead equipment catch up."

II. Cooling: The Second Front

If the power system answers "how do we get electricity in," the cooling system answers "what do we do with the heat after the electricity is consumed." In a data center, almost every watt that enters the IT load ultimately becomes heat. As rack power density rises, heat removal becomes as important as power delivery.

Cooling is not a secondary category. Excluding IT equipment, it is one of the largest infrastructure cost buckets in a data center and one of the largest non-IT electricity loads. In legacy enterprise data centers, air cooling could handle 10 to 15 kW racks. AI clusters changed the density problem. NVIDIA's GB200 NVL72 platform is a liquid-cooled rack-scale system, and Vertiv's reference architecture for the GB200 NVL72 was designed around a 7 MW facility block with racks that can reach roughly 120 kW. At that density, liquid cooling is no longer a premium option. It is part of the base design.

The three main cooling paths

• Direct-to-chip liquid cooling (DLC): the most mature and fastest-ramping solution for new AI builds. Cold plates attach directly to high-heat components, coolant carries heat into a facility loop, and supplemental air cooling still handles lower-density components. This is the dominant path for GB200-class deployments.

• Rear-door heat exchangers (RDHx): a lower-barrier retrofit technology for existing facilities. It can improve legacy air-cooled halls, but its practical capacity is not sufficient for the highest-density rack-scale systems. It is a bridge for brownfield assets, not the final architecture for the densest AI clusters.

• Immersion cooling: thermally efficient and attractive for certain high-performance computing environments, but still constrained by server design changes, maintenance workflow, dielectric fluid cost and operating familiarity. It remains more of a specialized solution than a mainstream hyperscale standard.

The near-term investment implication is that the cooling transition pushes value toward precision thermal systems: coolant distribution units (CDUs), pumps, manifolds, cold plates, quick-disconnect fittings, controls and facility piping. The shortage is not only in hardware. It is also in mechanical engineering labor and commissioning expertise. A shell that was designed for 15 kW racks cannot become a 120 kW AI factory simply by swapping server cabinets.

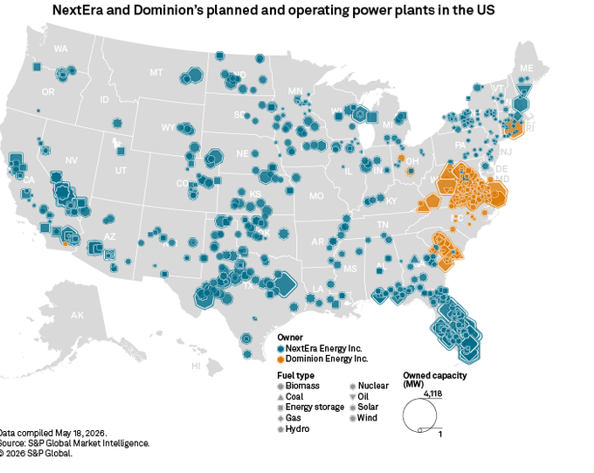

III. The NEE-Dominion Deal: Acquiring the Load Franchise

The most important recent transaction in the US power sector is NextEra Energy's agreement to combine with Dominion Energy. This is not just a scale deal. It is a thesis-defining event for the AI power cycle because it attaches a premium utility platform to one of the most important data center load pockets in the country.

Dominion Virginia sits at the center of Northern Virginia's data center ecosystem. NextEra brings the largest renewables and storage development platform in North America, with meaningful nuclear, gas and transmission optionality through FPL and NEER. The combined company would pair a large regulated rate base with a massive large-load opportunity set. That is exactly the direction Part 1 and Part 2 pointed toward: the scarcity is not simply megawatt-hours; it is regulated power delivery capacity in the right location, with the right interconnection path and the right customer demand.

Why the deal matters for the AI power thesis

First, data center load has graduated from a demand assumption into a sanctioned strategic asset. NEE's willingness to dilute its own shareholders by ~25.5% in order to absorb Dominion's Virginia franchise — the heart of "Data Center Alley" — is the strongest revealed-preference signal we have seen this cycle. The combined platform inherits a 130+ GW large-load pipeline, enough to justify years of sanctioned generation, transmission and distribution investment.

Second, the transaction validates the regulated-wires thesis over the merchant-generation thesis. In merchant power (CEG / VST / TLN), AI demand expresses itself as price volatility and capacity-market exposure — high-beta but exposed to spot softening. In a regulated utility, the same demand becomes sanctioned capex earning a regulator-protected return for 30–40 years. The combined NEE sits on a $138 Bn rate base with 80%+ regulated cash flow — a multiple-expansion candidate, not just an EPS-growth story.

Third, scale becomes a procurement weapon. The binding constraints in this cycle are no longer financial — they are transformer slots, turbine reservations (GEV backlog now past 2028), switchgear (ETN, VRT), interconnection queues and permitting bandwidth. A combined NEE-Dominion has structurally more leverage where delivery time matters more than unit price — the same logic that let Bloom's 55-day delivery beat lower-LCOE(Levelized Cost of Energy) alternatives at Oracle.

Fourth, the deal pushes the narrative beyond the narrow merchant trade. Gas gensets and SOFC fuel cells remain the tactical answer to time-to-power (TTP), but the highest-quality long-duration asset may be the integrated regulated platform that originates load, builds generation across renewables/gas/nuclear, upgrades wires, and procures constrained equipment at scale. This cycle's analog to Big Tech's vertically integrated capex platforms — but in regulated power.

If the deal closes, NEE pro forma becomes a regulated large-load platform with optionality across renewables, gas, nuclear, transmission and customer-supply — more powerful but more politically exposed than a pure renewables compounder.

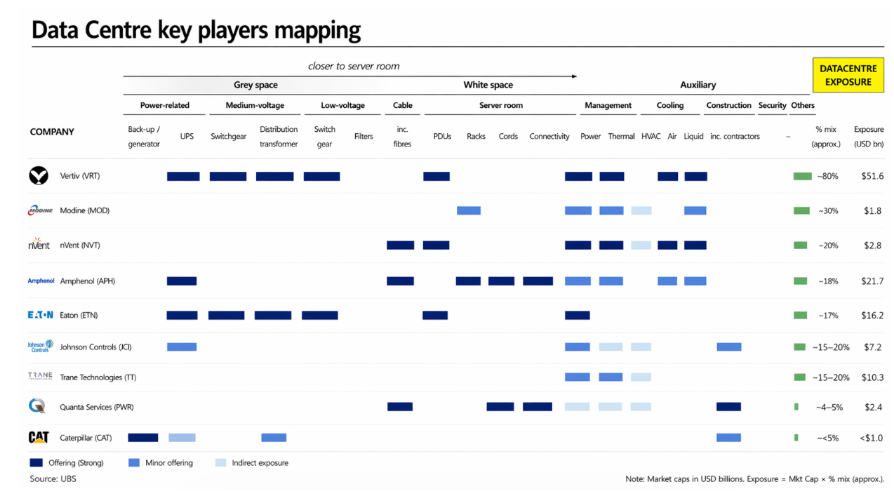

IV. Public-Market Map: Who Gets Paid and Why

The right way to rank the opportunity set is by proximity to the bottleneck and by the quality of risk transfer. A company that gets paid through regulated rate base has a different risk profile from a merchant generator exposed to spot power prices. A company that manufactures long-lead equipment has a different risk profile from a contractor whose revenue depends on project timing. The investment map should start with the question: does this company directly improve Time-to-Power (TTP)?

Tier 1 — Supply-Side Chokepoints: Where Lead Times Become Margin Expansion

These are the names that benefit regardless of which utility or hyperscaler wins, because they own positions in the value chain that cannot be substituted on AI's timeline.

GE Vernova (GEV) —One of three Western suppliers in HV power transformers, HV switchgear, and heavy-duty gas turbines (alongside Hitachi Energy and Siemens Energy). Prolec GE consolidates North American transformer capacity at the moment HV transformer lead times stretched past three years, and gas turbine slots are sold out beyond 2028. The thesis is no longer "discovered" — the next leg depends on margin expansion as backlog converts at richer pricing, not on order growth surprise.

Eaton (ETN) — The breadth play. ETN doesn't dominate any single product the way GEV dominates transformers, but it sells across the entire campus electrical stack — medium- and low-voltage switchgear, busways, UPS, power distribution, and now thermal through the Boyd Thermal acquisition. In a cycle where data center developers want fewer vendor interfaces, ETN's portfolio breadth is itself the moat. Closest analog: the "Schneider Electric of North America," with stronger AI-cycle leverage.

Vertiv (VRT) — The cleanest data center pure-play in the public markets. VRT's co-development of the 7 MW reference architecture for NVIDIA's GB200 NVL72 is the clearest signal of its design-in position: when NVIDIA wants to demonstrate how its highest-end rack should be powered and cooled, VRT is the partner of record. That is a structural position, not a contract. The risk is symmetric — when you are priced as the cleanest pure-play, expectations leave no slack.

Amphenol (APH) — Easy to miss in a power framework because interconnects are not "power equipment." But every high-density AI rack runs through APH's electrical, fiber and high-speed connectors, and requalification across a hyperscaler's installed base is so painful that incumbents almost never lose share. APH is the quietest way to own AI density — small share of system cost, disproportionate share of system reliability.

Tier 2 — Firm Power & Time-to-Power (TTP): Positioning the Bridge Phase

These solve a more specific problem: getting firm or clean megawatts to a campus before the grid is ready. Their value depends on a window — wide today, narrowing as Tier 1 supply catches up and regulated platforms like NEE/Dominion mobilize.

Bloom Energy (BE) — The only public SOFC pure-play at scale. BE's position is about being the fastest "real" power source in the market, deployable in weeks rather than years, on natural gas pipelines that already exist. Oracle's master agreement (with an attached warrant) signals something more than a customer relationship: a hyperscaler taking equity-linked optionality on its supplier's future. That is the tell.

Constellation Energy (CEG) — The cleanest large-cap expression of firm, low-carbon power scarcity in the US. CEG owns the largest US nuclear fleet by capacity; the Microsoft Three Mile Island Unit 1 restart (Crane Clean Energy Center) effectively set the market template for premium clean-firm PPAs. Calpine adds gas and geothermal optionality. CEG's position is structural — there are only a handful of operators in North America with both the fleet and the regulatory relationships to do this.

Vistra (VST) — The second-largest US nuclear operator at 6.4 GW, and Comanche Peak is one of only two nuclear stations in ERCOT — an islanded grid that cannot be served by PJM nuclear assets at the moment Texas is absorbing the densest hyperscaler buildout in the country. The PJM gas fleet adds a separate, contracted cash flow leg through rising capacity-market clears. The catalyst is behind-the-meter PPAs on the Energy Harbor sites.

Note on Tier 2: the NEE/Dominion deal, if successful, will slightly compress the structural premium of merchant nuclear by validating regulated nuclear as the lower-cost-of-capital alternative. CEG and VST remain valid trades, but the field is no longer theirs alone.

Caterpillar (CAT) — The dominant Western maker of large reciprocating gas gensets, with a dealer service network (Wheeler, Holt, Finning) that no AI campus developer can replicate. The Utah Joule 4 GW project reframes CAT from "standby supplier" to prime power partner — a structural shift the market is still digesting. The caveat is mix: data center remains a single-digit share of total CAT revenue, so the AI vector is incremental upside, not the core thesis.

V. How to Underwrite the Theme

The five-question framework we apply to every name in this universe:

1. Does the company shorten time-to-power (TTP), or is it merely adjacent to the theme?

2. Does it own a regulated load franchise, a constrained equipment slot, or a scarce engineering capability — or is its position replicable inside two years?

3. Is revenue protected by regulation, backlog, long-term contract, or customer prepayment — or is it merchant-exposed?

4. Who pays if the forecast is wrong — shareholders, ratepayers, hyperscalers, or merchant generators?

5. Is the stock already priced as if every announced megawatt becomes energized demand?

These questions sort our coverage along a clear axis. Regulated platforms like the NEE/Dominion combination convert AI capex into rate base earning a regulator-protected return for decades — earnings visibility unmatched anywhere else in the universe, paid for in regulatory dependency. One rung up the beta curve, the bottleneck equipment suppliers — GEV, ETN, VRT, APH — capture the same demand through physical scarcity; their pricing power is structural, but the market knows it, and the debate is now entirely about multiples. At the high-beta end sit the bridge and merchant names — BE, CEG, VST, CAT — where the revenue inflection comes fastest and the cash flows are most operationally levered, but the duration of those cash flows depends on how quickly the regulated tier behind them mobilizes.

The NEE-Dominion deal is the clearest validation of the US Power Series thesis to date. AI power demand is no longer a question of who owns electrons. It is a question of who owns the load pocket, the interconnection path, the transmission and distribution franchise, the equipment supply chain, and the regulatory permission to build.

This is why the theme is best framed as chokepoints, not categories. The investable positions are the bottlenecks that capital cannot instantly solve: regulated wires, transformer and switchgear capacity, gas turbine and reciprocating generator slots, liquid cooling infrastructure, precision interconnects, and the engineering labor that ties them together.

Gas gensets and fuel cells buy time. NEE/Dominion embeds AI demand into a regulated annuity. Between those two horizons, the chokepoint owners get paid on every megawatt that moves.