Will Three Mega Projects Make KoreaBecome the Next Mega in the AI Industry?

I. A "Nation-Scale Bet" Made Official

On June 29, theKorean government, together with Samsung, SK and other major chaebol, unveileda sweeping cross-ministerial long-term investment plan grandly titled the"Republic of Korea Great Leap Forward: 3 Mega Projects." This is thesingle most important macro event in Korea within this quarter — and arguablythis year. Combined government and corporate AI-related investment is plannedat roughly KRW380 trillion per year over the next decade, equivalent to around10% of GDP annually, with semiconductor-related investment alone accounting forabout 6% of GDP. Layered on top of the special act for USD350 billion ofinvestment in the US already passed by the National Assembly, Korea iseffectively wagering its entire industrial future.

At the same time,June exports smashed expectations with 70.9% year-on-year growth, and the goodstrade surplus hit a fresh record of USD36.1 billion — providing the mosttangible backing for this bet. The government's support policies are, quiteliterally, being funded by AI-boom windfalls.

This report isorganized around one core question: can the Three Mega Projects upgrade Koreafrom a "chokepoint supplier" in the AI supply chain into the nextmega player of the AI industry itself?

II. The 3 Mega Projects:Scale, Structure and Supporting Measures

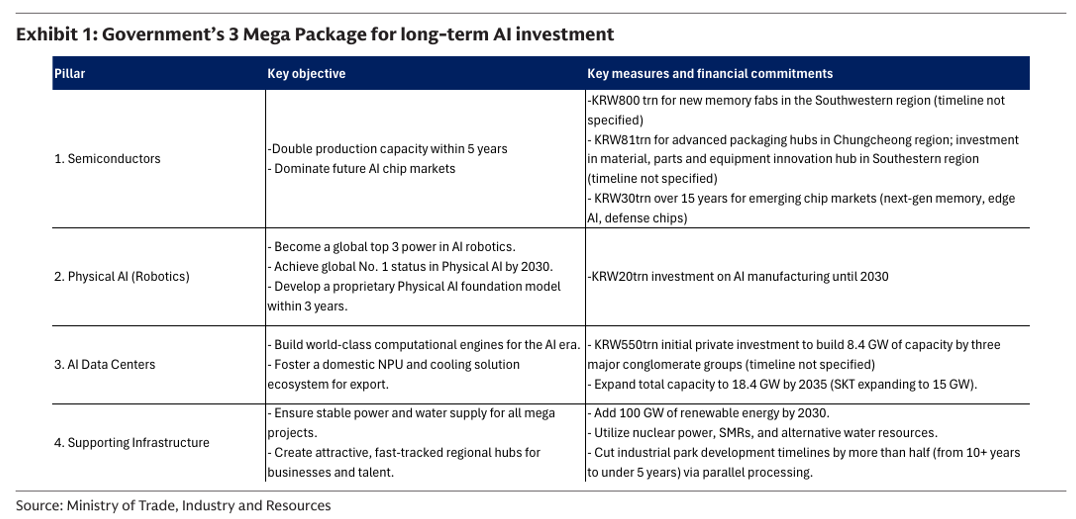

The plan is builton three pillars — semiconductors, Physical AI, and AI data centers — plussupporting infrastructure:

Pillar 1:Semiconductors. The target is todouble production capacity within five years and bring forward completion ofthe Yongin semiconductor hub in the greater Seoul area by 7–12 years. Thegovernment plans a cumulative KRW800 trillion investment to build new memoryfabs in the Southwestern region, an additional KRW81 trillion for advancedpackaging hubs in the Chungcheong region, and a materials, parts and equipmentinnovation hub in the Southeastern region. A further KRW30 trillion will bedeployed over 15 years into emerging markets such as next-generation memory,edge AI and defense chips. A presidential-led "SemiconductorCompetitiveness Special Committee" will coordinate comprehensive support.

Pillar 2:Physical AI (robotics). The goal isto make Korea a global top-3 power in AI robotics, achieve global No.1 statusin Physical AI by 2030, and develop a proprietary Physical AI foundation modelwithin three years. KRW20 trillion will be invested in the AI transition of manufacturingby 2030, which the government expects to create KRW100 trillion in value added.

Pillar 3: AIdata centers. SK Group, GS Groupand Naver will collectively invest KRW550 trillion to build 8.4GW of AI datacenter capacity, with SK Group further expanding total capacity to 18.4GW by2035 (SK Telecom leading a phased 15GW build-out expected to mobilize aroundKRW1,000 trillion, reportedly including foreign investment). The governmentwill also foster a domestic ecosystem of NPUs, power and cooling solutions withan eye toward exports.

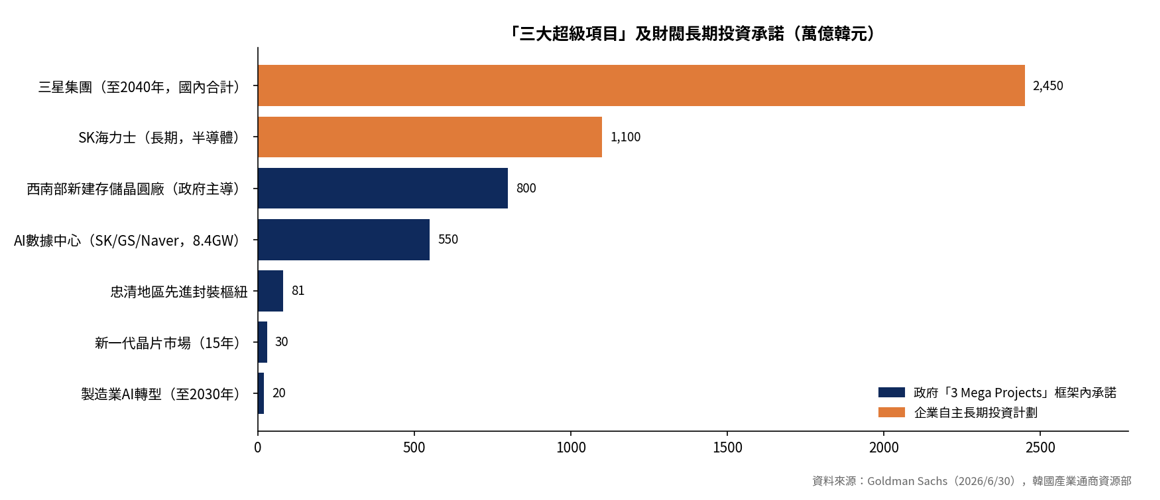

Supportingmeasures and corporate plans. Thegovernment has pledged stable power and water supply, competitive electricitytariffs, 100GW of additional renewable energy by 2030, use of nuclear power andSMRs, and cutting industrial park development timelines from over ten years tounder five. On the corporate side, Samsung confirmed plans to invest KRW2,450trillion domestically by 2040 (around KRW2,100 trillion in semiconductors),while SK Hynix plans KRW1,100 trillion in semiconductors over the long term,including KRW600 trillion for the Yongin cluster.

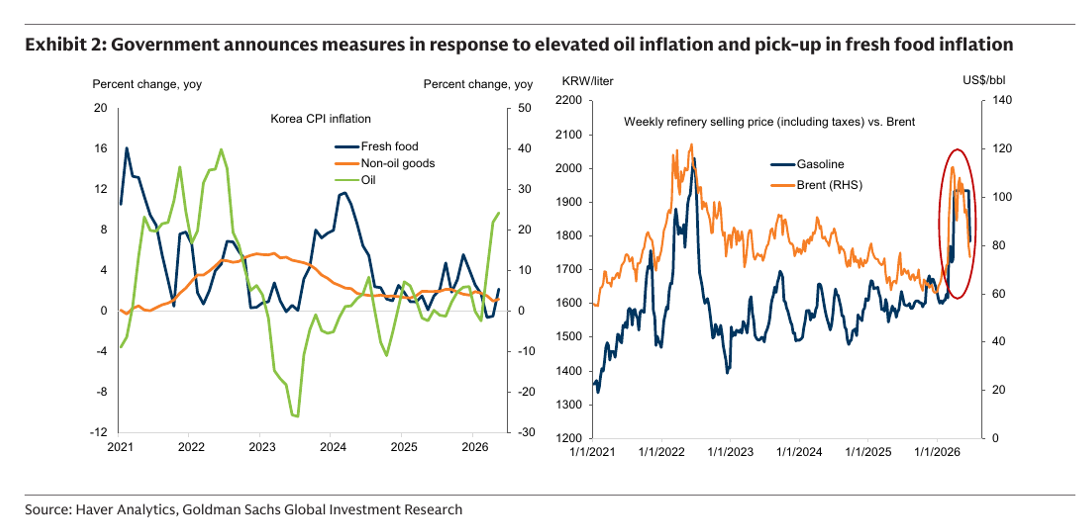

Also noteworthy:the government simultaneously rolled out roughly KRW1 trillion ofprice-stabilization measures — fuel price caps cut by KRW150 per liter (about10%), large-scale fresh-food discount subsidies, and a freeze on public serviceprices through year-end — together covering roughly 12% of the CPI basket. Thesignal is important: the fiscal windfall generated by the AI boom is beingrecycled to offset the inflation and cost-of-living pressures the boom itselfis creating.

III. Data Check: TheExport Boom Is Accelerating, Not Peaking

The Three MegaProjects are not a leap into the unknown — they double down on a lane whereKorea's advantage is already proven. June data provide powerful corroboration:

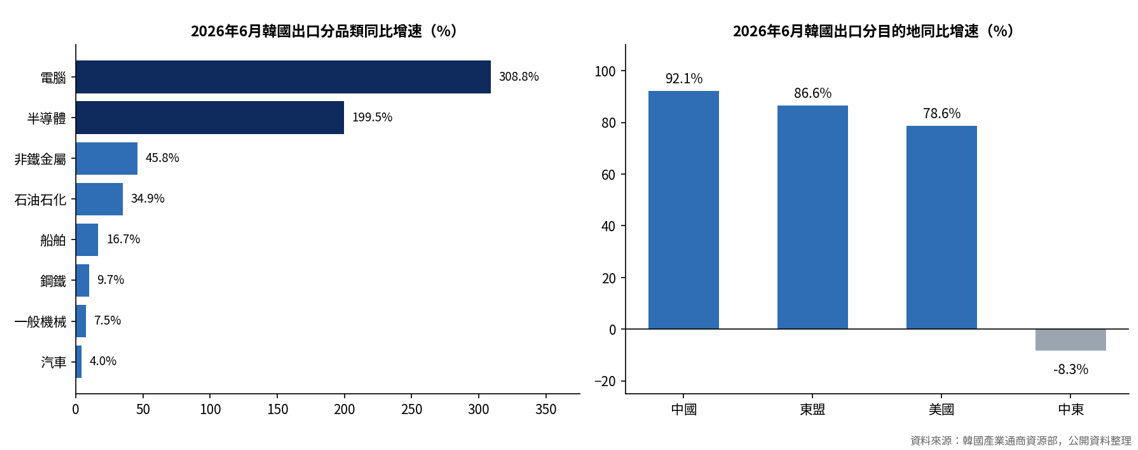

Exports farexceeded expectations. June exportstotaled USD102.25 billion — the first time monthly exports have ever crossedthe USD100 billion mark — up 70.9% year-on-year (vs 53.4% in May) and wellabove the Bloomberg consensus of 60.9%. The narrow AI chain (semiconductorsplus computers) contributed roughly 80% of the month's export growth:semiconductor exports reached USD44.8 billion, up 199.5% year-on-year — a sixthconsecutive month of triple-digit growth — while computer exports rose 308.8%.

The boom isspreading upstream. Steel exportsrose 9.7%, the first positive reading since April 2025, driven mainly byconstruction materials for data center build-outs; non-ferrous metal exportsgrew 45.8%, consistent with improving demand for power and data-center upstreammaterials. Traditional sectors also improved at the margin: petroleum andpetrochemical exports rose 34.9%, auto exports turned positive at 4%, andgeneral machinery turned positive for the first time in five months.

Broad-basedstrength across destinations. Exportsto the US rose 78.6%; exports to China climbed to 92.1% (with semiconductorexports to China more than tripling), lifting China–Korea bilateral trade to arecord USD36.4 billion; exports to ASEAN grew 86.6%. Korean semiconductorexports and Chinese integrated-circuit exports are moving in close resonance,pointing to China's June IC export growth rising from 110.9% toward roughly120%.

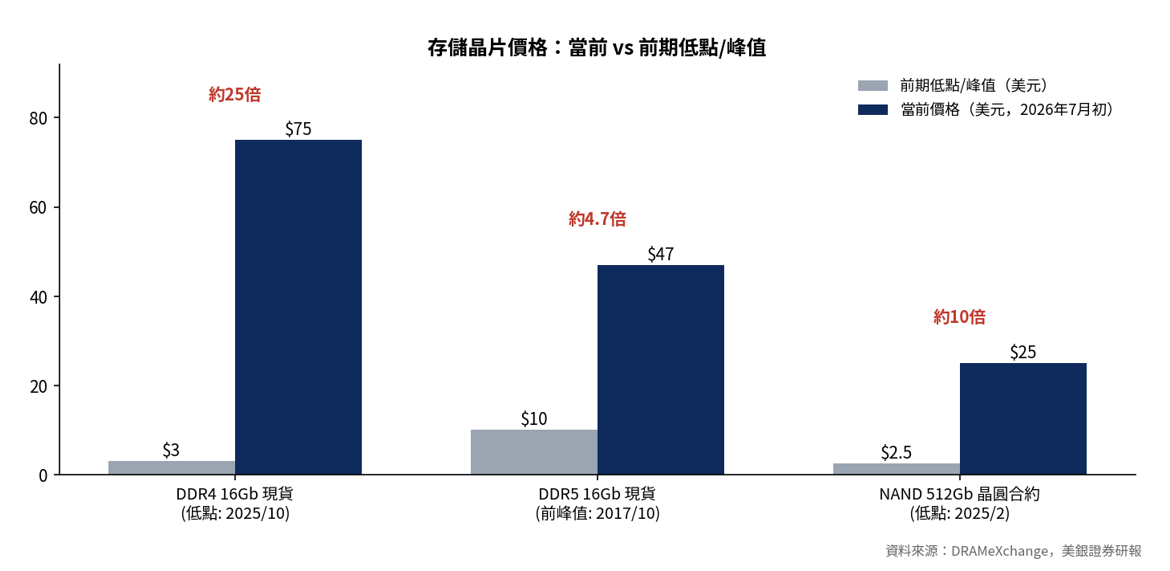

Price effectsare amplifying nominal growth. Korea'smemory export prices rose 17% month-on-month in May, and prices of major memorycategories kept climbing in June. Per DRAMeXchange, the 16Gb DDR5 spot pricehit a record USD47 in early July — more than three times the 2017 peak — while512Gb NAND wafer contract prices of about USD25 stand roughly 10x above theFebruary 2025 trough. TrendForce has sharply raised its Q3 DRAM ASP forecastfrom 3–8% to 13–18%.

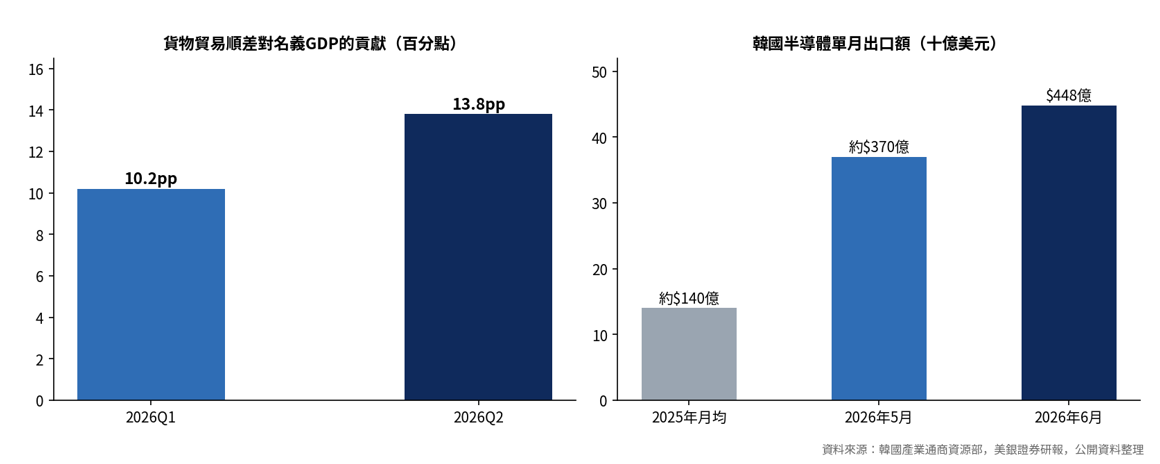

The surplus ispulling nominal growth even harder. TheQ2 goods trade surplus reached USD86.9 billion, contributing 13.8 percentagepoints to nominal GDP — up markedly from 10.2 points in Q1 — with theseasonally adjusted annualized surplus estimated at 16.8% of 2026 nominal GDP.External demand's boost to nominal growth and corporate earnings is stillstrengthening.

Fears of a"cycle peak" look overdone. Someinvestors read the KRW800 trillion Southwestern fab plan as a signal that thememory upcycle is ending. BofA Securities counters that the new cluster isunlikely to generate meaningful output before 2033 — it is a long-term plansequenced after the Yongin/Pyeongtaek expansion (2026–2035) — and thus haslimited bearing on the near-to-medium-term supply-demand balance. On the demandside, BofA expects the four big US hyperscalers' combined 2026 capex to growroughly 80% to about USD700 billion, approaching USD1 trillion in 2027–2028.The Philadelphia Semiconductor Index — which leads Korean semiconductor exportsby roughly four months — remains elevated year-on-year, pointing to continuedexport strength.

IV. History as Mirror:This Is the Second "Great Leap Forward"

The naming is noaccident. In 1973, Park Chung-hee issued the "Heavy and Chemical IndustryDeclaration," pushing Samsung, Hyundai, SK and other chaebol into tenstrategic industries — steel, shipbuilding, autos and more — on the strength ofstate-guaranteed low-interest loans. The results speak for themselves: Koreanper-capita GDP rose from USD94 in 1961 to USD1,772 by 1979, the "Miracleon the Han River" was written, and Korea's world-class competitiveness insemiconductors, autos and shipbuilding today rests on foundations laid in thatera.

The two GreatLeaps share the same underlying logic — the state picks the champions, thechaebol march to battle, and national resources are concentrated on a singlelane deemed vital to the nation. The key difference lies in where the chipscome from. Back then, the wager ran on bank credit backed by state guarantees;today, Samsung and SK's investment confidence comes from hard operating profits(Samsung Electronics' Q1 2026 operating profit surged 756% year-on-year).Corporate self-funding capacity is far stronger than fifty years ago.

But history leftthe other half of the lesson too. By 1997, the average debt-to-equity ratio ofthe top 30 chaebol had breached 500%. When the crisis hit, more than 30,000companies went bankrupt, Daewoo — then the second-largest chaebol — collapsed,and growth plunged from above 8% to -5.13%. The dividends and the risks of anation-scale mobilization have always been two sides of the same coin.

V. Risk Checklist: What toWatch

Structuralconcentration risk. Outsidesemiconductors, Korea's other export sectors remain relatively weak, deepeningthe economy's dependence on a handful of industries and firms. Samsung Group's2024 revenue equaled roughly 13% of Korean GDP; SK Hynix commands over 50% ofthe global HBM market and has overtaken Samsung Electronics as Korea's mostvaluable listed company. If the AI capex cycle turns, the shock will be highlyconcentrated.

Wealthdistribution and asset bubbles. InQ1 2026, Korea's real GDP grew 3.8% while real GDI surged 13.2% — thepurchasing-power windfall from chip price gains far exceeds real output growth,and it is concentrated in a few industries and households. In Dongtan, GyeonggiProvince, an 84-square-meter apartment jumped from KRW998 million to KRW1.12billion within two weeks; Seoul apartment prices have now risen for 72consecutive weeks. The Bank of Korea is holding its policy rate at 2.5% with ahawkish tilt, walking a tightrope between supporting the industrial boom andcontaining asset bubbles.

The gapbetween headline scale and true incremental spending. Some projects are not entirely new investment, andKorea's semiconductor equipment is heavily import-dependent (equipment importswere already up 42.4% year-on-year in June). Net of equipment imports anddouble counting, the plan's actual boost to nominal growth is likely to fallwell short of the headline KRW2,061 trillion (about USD1.3 trillion).

Execution andtimeline risk. The government pressrelease gave no clear timeline for the Southwestern cluster; the Physical AItargets — a proprietary foundation model within three years, global No.1 by2030 — are extremely ambitious; and whether power (100GW of new renewables) andtalent can keep pace remains to be seen.

VI. Conclusion: FromCanary to Mega Player?

Back to the titlequestion. Korea's role in the global AI map to date has been that of anirreplaceable chokepoint supplier — the memory boom has made it one of theclearest beneficiaries of this AI wave, and the "canary" for globalAI trade. The intent of the Three Mega Projects is to extend that advantagefrom "selling shovels" into AI data centers, an NPU ecosystem andPhysical AI — a leap from supply-chain node to industrial platform.

Near term, theanswer leans positive: exports,prices, the surplus, corporate earnings and fiscal revenue are reinforcing oneanother in a virtuous loop; the AI chain's impact is spreading from exportsinto investment and domestic demand; Q2 nominal GDP looks set to sustaindouble-digit growth; and leading indicators do not support an imminent cyclepeak.

Over themedium to long term, becoming "the next Mega" hinges not on the sizeof the investment but on three things: first,whether Korea can build genuine new pillars — NPUs, Physical AI — beyond itsmemory advantage and escape dependence on a single product cycle; second,whether the wealth effect can spread beyond the "semiconductorcorridor" into the broader economy, avoiding a rerun of the old script ofindustrial boom, housing surge and distributional strain; and third, whetherleverage and capacity discipline can hold — the lesson of 1997 is that thegreatest risks of nation-scale mobilization are sown at the cycle's mosteuphoric moment.

In one sentence:the Three Mega Projects have bought Korea a ticket to become a "Mega"of the AI era — but cashing it in depends on whether this Great Leap Forwardcan replicate the execution of the Han River Miracle while steering clear ofthe road to 1997.

Also, AIinfrastructure and related investments have already become a matter of nationalsecurity at the sovereign/state level. While Korea has made a big splash withthese mega investment announcements, almost all developed countries,individually or collectively, have ramped up efforts to do something similar(the US in particular has been doing so via the MAGA campaign). Competitionwill surely go beyond the company level and onto a much bigger scale viaindustry collaboration or government-led schemes.