The AI You Can’t Buy - When Conviction Outruns Access

Ask a single family office (SFO) today whether artificial intelligence will reshape the global economy, and the answer is almost unanimous: yes. Ask that same SFO how much of its portfolio is exposed to the companies building that future, and the room goes quiet. Herein lies the paradox of the 2026 SFO. Conviction on AI has never been higher, yet exposure to the layers where the value is truly being created has rarely been thinner. The problem, it turns out, is not belief. It is access.

Value Now Accrues Before the IPO

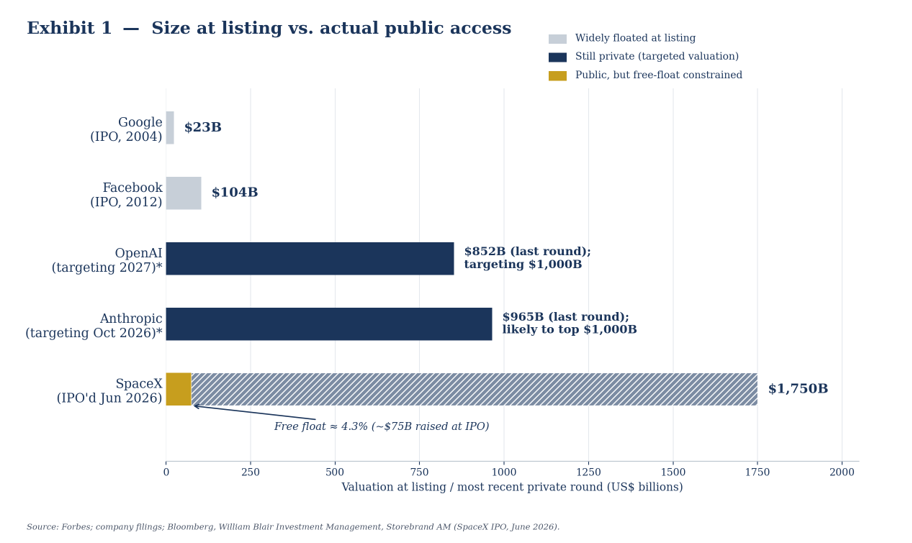

For most of market history, companies that defined a technological era went public early and grew up in front of public investors. Google listed at a valuation of roughly US$23 billion; Facebook at about US$104 billion. The bulk of their appreciation happened on the public tape, where any investor could participate. That model has quietly broken.

Today the defining companies of the AI era are reaching extraordinary scale while still private, and the timeline keeps shifting. OpenAI’s most recent private round, in March 2026, valued the company at US$852 billion; it has confidentially filed for an IPO but is reportedly leaning toward delaying its listing until 2027 rather than accept anything below its US$1 trillion target. Anthropic has since overtaken it: a US$65 billion round in May 2026 valued the company at US$965 billion, and Anthropic filed its own confidential S-1 four days later, targeting a Nasdaq listing as early as October 2026 — potentially beating OpenAI to market and crossing US$1 trillion at the point of listing. Companies are simply staying private far longer: the median age of a company at IPO has drifted out to around 13 years, from roughly 10 years in 2018, as abundant private capital removes the need to list. And that capital is pouring into one theme. AI-related startups absorbed roughly half of all global venture funding in 2025 and, in the first quarter of 2026, an extraordinary share approaching 80%, anchored by OpenAI’s US$122 billion round, the largest private financing on record. With global private-market assets already well into the double-digit trillions and still growing at a healthy clip, the machinery to keep companies private is only getting stronger.

The implication for allocators is uncomfortable but simple. The steepest part of the value-creation curve now sits in private hands. By the time these businesses reach the public market — if they reach them at all — the earliest and often largest gains have already been captured by those who held the shares before the bell.

Public Markets Offer Only the Second Order

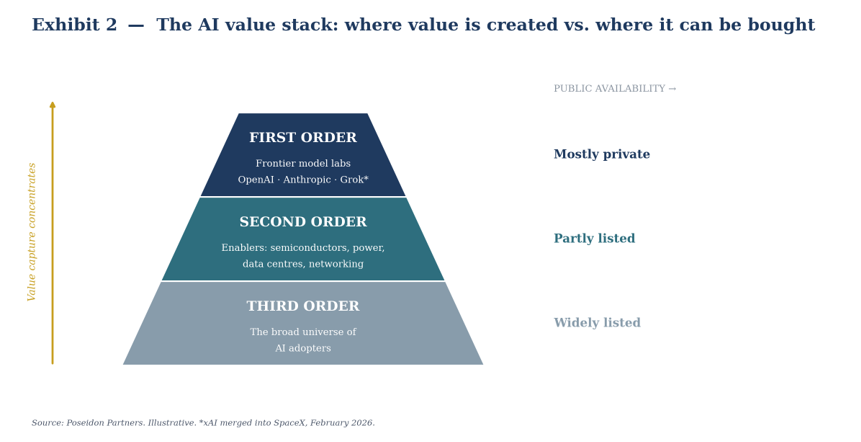

It helps to picture the AI opportunity as a stack of three layers. The first order is the frontier itself — the model labs such as OpenAI and Anthropic, along with Grok, which was folded into SpaceX after Musk merged xAI into the rocket company in February 2026 — and it is almost entirely private. The second order is the enabling infrastructure: the semiconductors, power, networking and data centers that the frontier consumes; here a handful of names are listed, but they are the picks-and-shovels, not the gold. The third order is the broad universe of businesses that will eventually adopt AI. When an SFO says it is “invested in AI,” it is almost always describing the second and third orders.

The structure of public markets reinforces this. Even when a private giant finally lists, index mechanics limit how much its investors own. Because major benchmarks weight companies by their freely traded shares, a business worth US$2 trillion but with only US$50 billion of free float would enter a large-cap index at a weight of just 0.08%. The access problem does not disappear at the IPO — it simply changes shape, and it no longer needs to be argued hypothetically. SpaceX went public in June 2026 in what ranked as the largest listing in history, pricing at a valuation near US$1.75 trillion. Yet an estimated 95% of its shares remained locked up at the open, leaving a public float of only around 4% of shares outstanding; S&P Dow Jones held the stock back from the S&P 500 pending the profitability and seasoning criteria it requires even as other benchmarks fast-tracked it in at a capped weight. For allocators who had waited for the IPO to finally gain scale exposure, the listing itself turned out to be another form of the access wall, not the end of it. It is also, since Musk folded xAI into SpaceX five months earlier, the only public route to Grok and the rest of what was once xAI’s frontier model business.

None of this is hypothetical. Of the ten companies that contributed most to venture investors’ returns this year, nine remain privately held — the highest proportion in the history of that ranking. A portfolio built purely from listed AI names is buying the derivative of the theme, not its source.

The Gap, in the Data

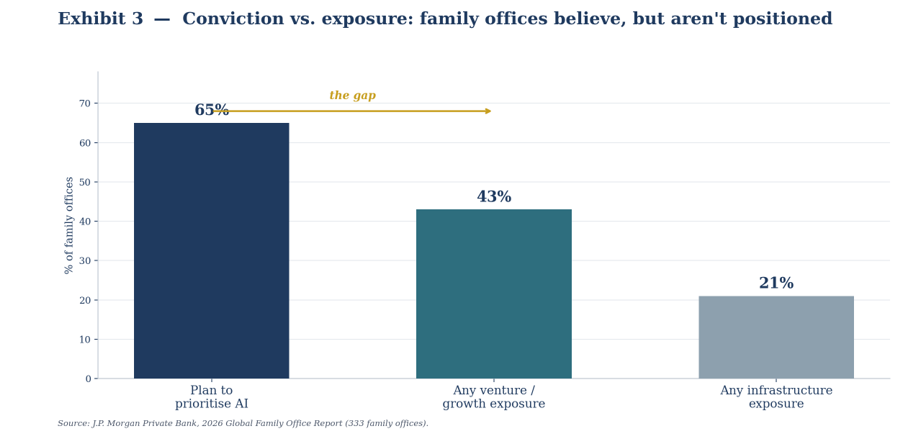

This is where conviction and exposure part ways, and the numbers are striking. According to J.P. Morgan’s 2026 Global Family Office Report, around 65% of the family offices it surveyed — the large majority of which are SFOs — intend to prioritise AI. Yet only 43% hold any exposure to venture capital and growth equity — the channel through which most frontier value is created — and where they do, it averages barely 3.3% of the portfolio. Direct exposure to infrastructure, the physical backbone of AI, is rarer still: only about one in five hold any at all. J.P. Morgan’s own estimate puts the value of the top ten AI companies at roughly US$1.5 trillion, the great majority of it created and held outside public markets.

Read together, these figures describe a near-universal belief sitting alongside an almost-absent position. SFOs are not skeptical about AI. They are simply not invested where AI’s value actually lives.

Why the Gap Is Rational: Four Walls

It would be easy to read this as negligence. It is not. The gap persists because four very real walls stand between conviction and position — and understanding them is the first step to scaling them.

1. The structural wall. Value is increasingly captured before a company ever lists, so the public market simply offers fewer and later entry points into the names that matter.

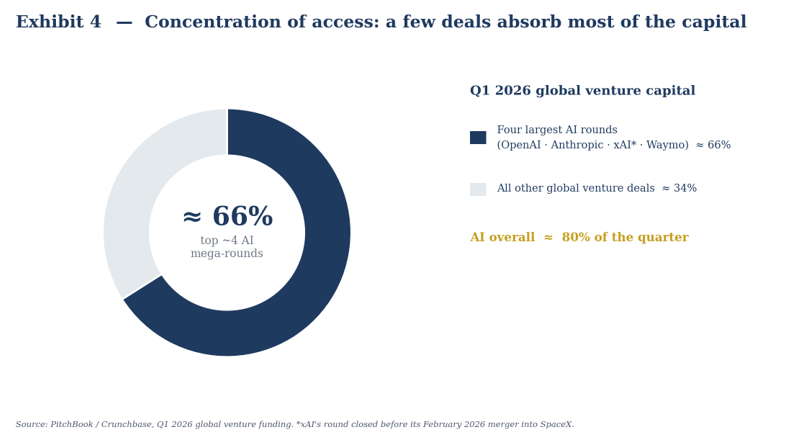

2. The access wall. Beyond minimums and qualified-investor thresholds, the best opportunities are allocation-constrained. A small circle of elite venture managers, alongside sovereign wealth funds commanding more than US$12 trillion, absorbs the marquee rounds — in the first quarter of 2026, roughly four deals accounted for close to two-thirds of all global venture capital. In this environment, a seat at the table has become one of the scarcest assets in the market.

3. The liquidity wall. Private positions demand multi-year lock-ups that sit awkwardly against a family’s liquidity needs, and the escape valve is still narrow: only around 2% of unicorn value trades in the secondary market.

4. The selection wall. Returns in private markets are enormously dispersed. Choosing the wrong fund or the wrong vintage can leave an investor with the theme’s risk and none of its reward, which makes manager selection decisive rather than incidental.

These are genuine frictions, not failures of will. And that is precisely the point: because the walls are real, the ability to scale them is valuable.

Where the Doors Are Opening — and How an SFO Walks Through Them

The encouraging development is that the toolkit for closing this gap is maturing quickly. Each route below suits a different profile of SFO, and most programmes end up combining more than one.

1. Secondary marketplaces. Platforms such as Forge Global and Hiive now provide indicative pricing and matched trades in pre-IPO shares of companies including Anthropic and OpenAI, sourced mainly from departing employees and early investors. This is currently the most direct route into single-name exposure to the frontier labs themselves, though allocation size is opportunistic and pricing carries a liquidity discount or premium depending on demand at the time.

2. Feeder vehicles and SPVs. Specialist venture platforms pool capital from multiple SFOs into a single-purpose vehicle that then buys into a specific round or share block, lowering the effective minimum ticket from the tens of millions a lead investor might require to a fraction of that. The trade-off is an added layer of fees and reduced direct negotiating power over terms.

3. Evergreen and interval funds. A growing set of semi-liquid venture and growth-equity funds offer periodic — usually quarterly — redemption windows instead of a fixed ten-year lock-up, and accept subscriptions well below traditional venture minimums. These are often the easiest entry point for an SFO’s first allocation, though redemption capacity is typically capped at a small percentage of fund NAV per quarter and cannot be relied on in a liquidity crunch.

4. Continuation funds and GP-led secondaries. As venture funds age without an exit, general partners increasingly roll their strongest positions into continuation vehicles, giving existing and new LPs a chance to buy in at a priced mark rather than wait for an eventual IPO. This is a growing route for an SFO to gain exposure to a maturing AI holding without waiting for the sponsoring fund’s original life to run its course.

5. Direct co-investment through private banks and EAMs. Where a private bank or EAM has an existing relationship with a venture manager or corporate, it can occasionally bring SFO clients in as co-investors alongside a lead round, on the same terms and without an additional layer of fund fees. Access here is relationship-driven and typically reserved for larger or longer-standing clients.

6. Structured and private-wealth wrappers. Tender-offer funds and other interval-fund structures marketed through wealth channels package late-stage and pre-IPO exposure — including to AI names — into a single ticket with lower minimums, professional manager selection, and simplified reporting. These trade some manager-selection control for convenience and diversification.

For an SFO weighing these six routes, the practical question is less “which is best” than “which matches our size, time horizon and appetite for illiquidity” — and increasingly, the right answer combines more than one of them.

From Conviction to Position

Insight, in the end, has been commoditized. Every serious investor now knows that AI is the defining theme of the decade; the view is no longer a differentiator. What remains scarce is execution — sourcing genuine access, choosing the right structures, selecting managers with discipline, and integrating illiquid positions into the wider portfolio with due regard for sizing, liquidity and risk. This is the quiet work that turns a conviction into a position, and it is precisely where an SFO’s adviser earns its keep. The gap between what SFOs believe about AI and what they own is not a story of doubt. It is an access problem — and closing it, thoughtfully and in the right size, is the value we exist to add.