2026 H2 Global Economic Outlook (II) — China & Japan

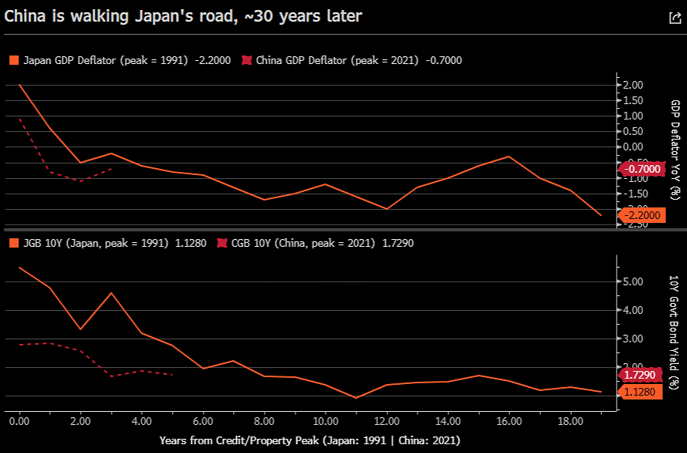

Japan's Yesterday, China's Tomorrow

Summary — One Road, Two Travelers

We always write China and Japan together, and this quarter the reason is the whole thesis. China is walking a version of the road Japan travelled a generation ago: a property super-cycle that turned, a balance-sheet recession the authorities are reluctant to name, deflation that has outlasted every forecast, and a demographic tide going out. Japan is what that road looks like thirty years on — and, lately, what the far end of it can look like when an economy finally stops fighting the diagnosis and starts to normalize. China is Japan's past; Japan is, in many respects, China's future.

But a shared road does not mean a shared destination right now — and that is the part the consensus keeps missing. The two are at opposite ends of the same arc, which is precisely why the trades diverge. China is early in the deflationary descent, with policy still pointed at the supply side and an equity market that is cheap for a reason. Japan is climbing out the other side: a central bank finally at 1.00%, banks compounding on normalization, and a currency so undervalued it has become the most asymmetric — and most frustrating — trade in macro. Our job is not to admire the symmetry. It is to trade the gap between yesterday and tomorrow.

The cross-asset spine runs straight out of Part I. Our highest-conviction US call is that the next Fed move is not a hike, and that the market's drift toward hikes is the misprice of the second half. When that unwinds, the US rate differential compresses — and that, not anything happening in Tokyo or Beijing, is the engine under both a stronger yen and a stable renminbi. So Part II is the Asian expression of the same macro view, with one deliberate outlier: China, where we stay structurally cautious regardless of what the Fed does, because China's problem was never American interest rates.

Before we lay out the book, the ledger.

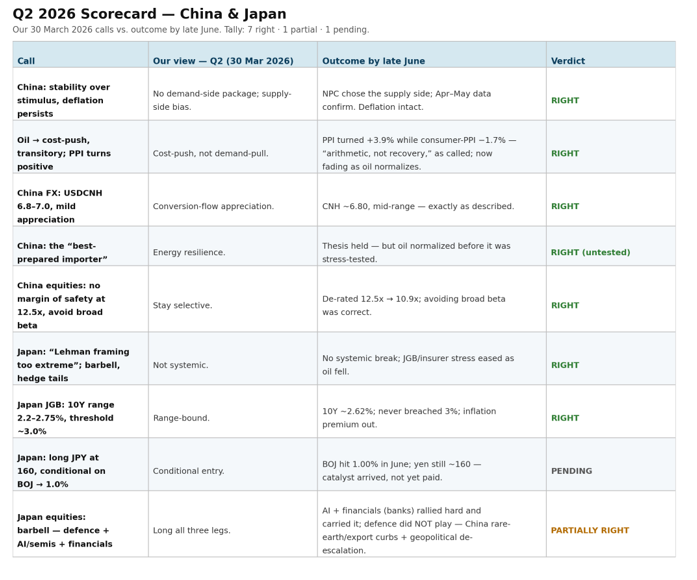

Scorecard — What We Got Right and Wrong

Our Q2 China/Japan note ("Two Economies, Two Fragilities") made nine calls. The fragilities we flagged were largely energy-shock-driven; that shock has since resolved, which makes this a good moment to mark them honestly.

1. China: stability over stimulus, deflation persists, no demand-side package. Status: Right. The National People's Congress chose the supply side, and nothing since has changed it. April and May confirmed it in the data.

2. Oil → cost-push CPI/PPI, transitory; PPI turns positive. Status: Right. The call played out exactly: PPI turned positive (+3.9% in May) while consumer-goods PPI sat at −1.7% — the “arithmetic, not recovery” story we described — and, as we said it would, the uplift now fades as oil normalizes, with PPI rolling back over in H2.

3. China FX: USDCNH 6.8–7.0, mild appreciation on conversion flows. Status: Right. CNH sits ~6.80, mid-range, exactly the conversion-flow dynamic we described.

4. China as the "best-prepared importer." Status: Right, untested. The thesis held, but oil normalized before the resilience was ever stress-tested.

5. China equities: no margin of safety at 12.5x, avoid broad beta, stay selective. Status: Right. MSCI China de-rated from 12.5x to ~10.9x — avoiding broad beta was the correct call, and it is the reason this section is not a victory lap on valuation.

6. Japan: "the Lehman framing is too extreme," barbell and hedge the tails. Status: Right. No systemic break. As oil fell, the JGB and insurer stress eased and the tail we were asked to fear never fired.

7. Japan JGB: 10Y range 2.2–2.75%, systemic threshold ~3.0%. Status: Right. The 10Y sits ~2.62%, never breached 3%, and the energy-driven inflation premium has come out.

8. Japan: long JPY at 160, conditional on the BOJ reaching 1.0% in H2. Status: Pending — the catalyst just arrived. The BOJ hiked to 1.00% in June, but the yen is still ~160. The condition we set has been met; the trade has not yet paid. This is the live, unresolved setup that headlines our Japan view.

9. Japan equities: barbell — long defence, AI/semiconductors, and financials. Status: Partially right. AI and financials (banks) rallied hard and carried the book; defence did not play — China's rare-earth and dual-use export curbs weighed on the supply chain, and the geopolitical premium faded as Iran de-escalated. Two of three legs worked; we evolve the barbell below.

China Macro — The Balance-Sheet Recession

Start with the diagnosis, because everything downstream follows from it. China is in a balance-sheet recession dressed up as a growth target, and the authorities are treating a structural problem with cyclical tools. The root is property, and property's problems are not cyclical — they are the three slow-moving forces that broke Japan.

First, affordability. A generation of Chinese households bought homes because prices only rose; that reflexive demand is gone. Prices remain high relative to incomes, and the cohort that should be forming households can no longer underwrite the purchase the way it did over the past twenty years. Second, urbanization has plateaued. The rate has climbed from roughly 19% at the start of reform to about 66% today — the great migration that manufactured housing demand for three decades is largely complete. The remaining gap to developed-economy levels (~80%) is real but slow, and much of it is gated behind hukou reform: the household-registration rate is still only ~48–49%, so the migrants already in the cities lack the urban status that would unlock their demand. Third, demographics. The population is now shrinking, and quickly. Absent large-scale foreign labor — which is not politically on the table — the buyer base contracts from here. The over-built second- and third-tier cities, the ones that financed themselves on land sales, face supply that dwarfs demand for years. Tier-1 cities, which siphon people and capital, hold up better, but even there the long-term trend is down.

When the property engine stalled, China lost the leading driver of two decades of growth, and the inertia of that growth broke with it. Layer on the demand scar from COVID, and you get the spiral we are now in: deflation feeds involution, involution keeps PPI, CPI, and incomes from rising, weak income depresses consumption, weak consumption compresses corporate revenue and earnings — and falling earnings feed back into the next leg down. This is not a forecast; it is the mechanism already running. A-share non-financial ex-oil earnings have now contracted for four consecutive years — a sequence almost without precedent — and the 2025 equity rally was multiple expansion, not an earnings recovery.

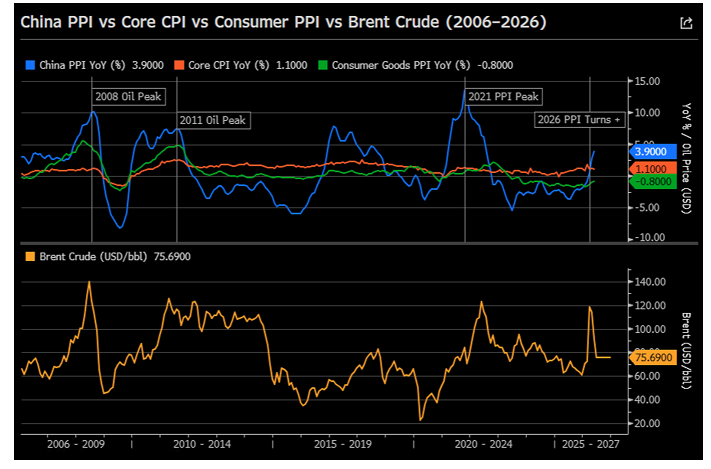

The oil shock briefly papered over this. It pushed PPI to +3.9% in May, and some read that as reflation. It is not. With the output gap deeply negative and capacity utilization near record lows, upstream price increases cannot transmit downstream — consumer-goods PPI was still −1.7%, the most negative reading on record for this episode. So the cost-push bump squeezes mid- and downstream margins without generating revenue, and our episode work is clear that these bumps fade: across the comparable oil-shock episodes, PPI rolls from peak back to zero in a median of ~10 months. With Brent now back near $79, the arithmetic points to PPI rolling over through H2 and the deflationary signal reasserting into 2027.

Why won't policy break the cycle? Because the policy is the cycle. Fiscal leverage has gone into cyclical fixes for a structural problem — propping up investment and subsidizing supply — rather than into household balance sheets; the money never reaches the consumer's pocket. And in the opening year of the 15th Five-Year Plan, the leadership's attention is on "new productive forces," not on stabilizing demand. Worse, because the Q1 GDP beat and a steadily rising export share gave policymakers confidence, they tightened at the margin — stepping up tax collection, easing off fiscal intensity, defending the rate floor, and tolerating renminbi appreciation. The space for a new easing cycle is also genuinely limited: the banking system's net interest margin has fallen to ~1.4%, now below the ~1.5% non-performing-loan ratio, and the macro leverage ratio has reached ~309% — higher than Japan's in the late-1990s-to-2008 stretch. There is not much room, and what room exists is being husbanded.

This is the distinction that matters for H2: there is a demand recession underneath the headline, and exports are masking it. April–May retail sales and fixed-asset investment were negative in real terms; even adding goods exports, total demand grew only ~1.6% year-on-year — a reading seen only in the early-2020 pandemic shock. Yet industrial production and exports stayed strong on subsidies and external demand, so the internal/external imbalance is widening, and the economy's near-term stability is increasingly hostage to one leg: exports.

We should be careful with the Japan analogy, though, because China is not a carbon copy. It is, if anything, a faster and harder version, run under tighter control. China is moving on the supply side far earlier and more aggressively than Japan did with its zombie banks; its demographics are deteriorating faster and from a lower per-capita income, so the buffer is thinner; but it also has capital controls and a managed currency, tools Japan never had to lean on. The road rhymes; the speed and the steering do not.

One asymmetry keeps us from being outright bears: the central put. The leadership cannot comfortably miss a 4.5–5% growth target in the first year of a new Plan. If Q2 prints below 4.5% and no new measures arrive, the second half starts to look like late-2024 — and that is politically hard to accept. So a stimulus response is a live tail; the worse the data, the higher its probability. But its timing and scale are genuinely uncertain, it would likely be weaker than the late-2024 package given the NIM and leverage constraints, and cyclical stimulus still cannot fix a structural problem. We treat it as a catalyst to monitor — in the data and in the official language — not as a base case.

China Equities — Cheap, But Not a Buy

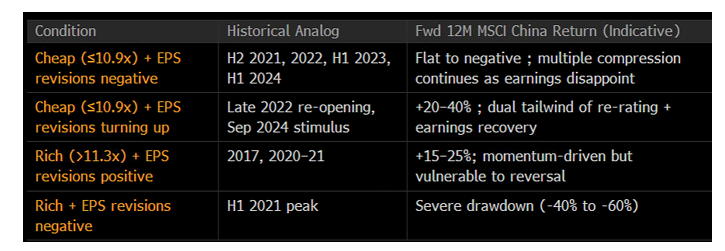

The bull case on Chinese equities is one number: ~10.9x forward earnings, below the long-run mean. We think that number is a trap, and the history is unambiguous about why. Cheap isn't enough. MSCI China traded below 10x for most of 2022–2024 and still delivered negative returns, because earnings-revision breadth was negative the entire time. In our valuation-breadth work, "cheap + revisions falling" produces flat-to-negative forward returns; the only configurations that pay are "cheap + revisions turning up" (the 2022 reopening, the September-2024 stimulus: +20–40%). Today we are in the first bucket, not the second. The signal that would change our mind is not a lower multiple — it is earnings-revision breadth turning, which requires either demand-side stimulus or a genuine end to the deflation, neither of which is our base case.

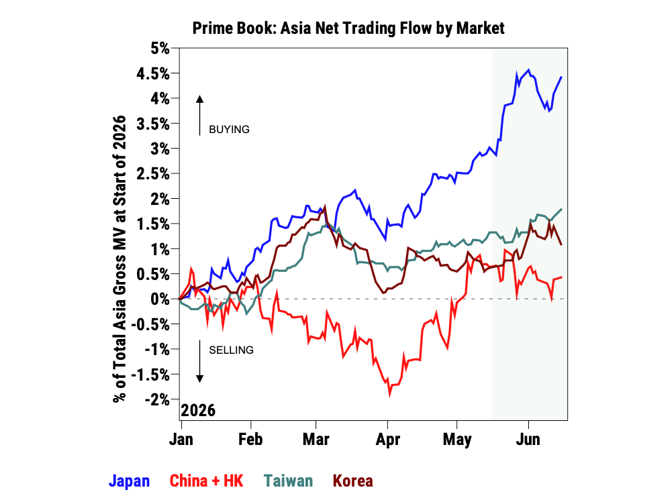

There is a second driver of the underperformance that we think is the most underappreciated, and it is a flow story sitting on top of the fundamental one. China has become the funding leg of Asia's AI trade. Foreign capital is using an underweight (and in places outright short) China to finance overweights in the North-Asia AI complex — Korea and Taiwan — which is why China can fall 3% in a week while Korea rallies 14% and Taiwan 5%, and why global allocators now prefer North Asia over China by a wide margin. Onshore, the same drain is happening: domestic and southbound liquidity is being pulled into the handful of AI beneficiaries and the wave of new IPOs absorbing fresh supply. This, more than any single data point, is why the index grinds lower even as global equities make highs. It is a liquidity vacuum, and until the central government signals it is adding to stimulus, we expect the grind — the slow bleed — to continue.

But a flow story cuts both ways, and this is where we part company with the outright bears. Positioning this light — foreigners underweight, onshore drained, sentiment at a floor — is exactly the fuel for a violent reversal. If a central put arrives and earnings-revision breadth turns, the same crowded funding trade unwinds, and the re-allocation can drive a 15–25% squeeze of the kind we saw in September 2024. So our stance is structurally cautious but tactically alert: keep beta light and wait, but be ready to flip fast on the catalyst. There is even a portfolio benefit hiding here — because China is the short/funding leg of the AI trade, it is a partial hedge to the crowded-AI risk we flagged in Part I: in an AI-led risk-off, the funding trade reverses and China would likely outperform.

So the equity book is selective, not absent. We hold what the government is actually supporting and where revisions are positive: AI and the cloud/data-center build (the RMB2tn national data-center plan is the one place in China with a genuine capex and revenue tailwind), banks and high-dividend names (TINA, with the 10-year government bond at ~1.7%, and the structural migration of household savings out of property and into financial assets), and genuinely-stabilizing Tier-1 property-adjacent names where the recovery is real rather than statistical. We do not own the index. The trade in China is not the beta.

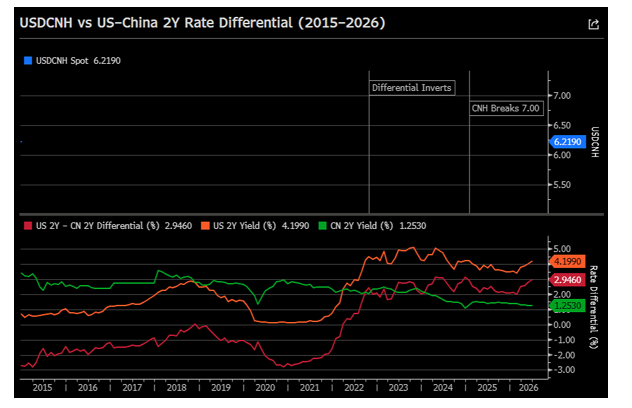

China FX — The Wrong Kind of Strength

The renminbi's firming earlier this year was, at heart, a soft-dollar trade — the market then leaning toward Fed easing — amplified by heavy exporter conversion flows and a PBOC content to let it grind. That driver has since flipped: after the Iran shock and the hawkish Warsh repricing, the market moved to pricing Fed hikes, the dollar firmed, and the renminbi gave some of the move back to ~6.80. So this was never a vote of confidence in the economy — it is the dollar/Fed path expressing itself through a managed currency. The tie to the yen is one of engine, not timing: both are levers on the US rate path, and both currently sit on the wrong side of a market pricing hikes. Our constructive case on each is the same forward bet — that those hikes don't materialize — with the renminbi the lower-beta, PBOC-smoothed version: Beijing sets the pace, caps the spikes either way, and leans against anything disorderly.

Here is the refinement that matters for H2, and it is the one that finally makes our currency call consistent with our macro call: because the macro is deteriorating and exports are the only engine still stabilizing growth, Beijing has every incentive not to let the renminbi appreciate quickly. A rapidly rising currency would undercut the one thing holding the economy up. So we do not expect a repeat of the rapid appreciation of late 2025. We see USDCNH range-bound between 6.7 and 6.9 — pressured toward the weaker end in the near term on a firmer dollar, soft data, export-competitiveness needs, and the risk of funding outflows, with only a slow structural appreciation over the longer term as conversion flows and current-account liberalization play out. In positioning terms, this is not a level to chase a long at 6.80; it is a low-beta, structurally-mild-appreciation lean, best accumulated near the weak end, and it serves the book as the stable, policy-anchored counterpart to the higher-octane yen trade.

Japan: BOJ & JGB — Normalization on Track

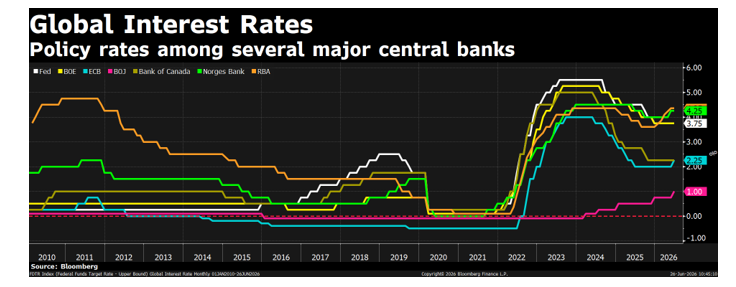

If China is yesterday's Japan, today's Japan is the more hopeful end of the road: a central bank that has stopped pretending and started normalizing. The BOJ hiked to 1.00% in June — the level our Q2 note made the condition for the yen trade — with a slightly dovish guidance tweak and a reflationist dissent from the Takaichi-appointed Asada, a reminder that the political tilt is toward caution on the terminal rate. Our base case (and the GS house view) is that the next hike waits until early 2027, with the risk skewed earlier if the yen stays weak enough to push underlying inflation through 2%.

The important point for the book is what didn't happen. The JGB stress that defined our Q2 note has eased. As oil fell, the energy-driven inflation premium came out of the curve, the "naphtha-flation" overshoot the BOJ feared looks contained (cumulative CPI impact ~0.2–0.3pp), and the 10-year sits at ~2.62% — comfortably inside our range and far from the ~3.0% level we identified as the systemic threshold for forced insurer selling. The 30s and 40s remain elevated (~3.7–3.8%) on fiscal supply, and the near-term risk is a bear-steepening of the super-long end on light central-bank buying, which keeps a modest 10s/30s steepener sensible as a tactical overlay. But the tail we were asked to hedge in Q2 — the "Lehman moment" — has receded with the oil price. Japanese normalization is proceeding without a financial accident, and that is the backdrop the rest of the Japan book is built on.

Japan FX — The Value Yen, on the World's Hardest Trade

Long yen is the single most asymmetric idea in this note, and we want to be precise about both why and how, because it has frustrated everyone who has touched it.

The why is value, and it is extreme. The yen's real effective exchange rate sits at ~65.6 — the 1st percentile of its 26-year history, roughly 40% below its long-run average, and more undervalued than at any prior episode we can find. Decompose the move and the asymmetry is even clearer: the yen is currently trading some 10–15 figures weaker than the US–Japan rate differential alone would imply, the residue of the oil shock and a persistent carry bid — and the oil drag is now gone. This is a currency stretched to a generational extreme with one of its two weights removed.

The how is where discipline matters, because the yen is a pure-market, carry-driven currency, and FX trends run far longer and harder than equity trends. The Japan side of the convergence is now largely spent — the BOJ is at 1.00% and signaling patience — so from here the trade leans on the US side: it pays when the priced Fed hikes unwind and the US 2-year falls. In other words, long yen is the highest-octane expression of our Part I Fed call, not an independent Japan story.

And here the history is genuinely encouraging, because it answers the obvious objection — that a strong US economy and an "AI premium" will keep siphoning capital into the dollar regardless. Across every episode since 1990 where the market priced Fed hikes that were not delivered, the dollar weakened in the following 3–6 months in nearly every case — even when US growth stayed strong and the US was outperforming. The dollar tracks the change in rate expectations, not the level of rates or growth. The closest analog to today — the 2023–24 "higher-for-longer" episode that resolved into cuts — saw USDJPY fall ~9% even as the US kept outperforming. We may be near peak hawkishness right now (a hawkish Warsh debut, a full hike priced by October); historically, the 3–6 months after that point are where the dollar tops and the yen turns.

So we run it as a window trade with three rules. The trigger: don't anticipate the peak — wait for the first soft inflation prints that confirm the hikes won't be delivered, which is the signal we are past peak hawkishness and the 3–6 month window has opened. The expression: lead with convexity (yen-calls screen cheap given low vol, which converts the negative carry into a defined premium) and add modest spot once triggered, sized as a lever on the front-end Fed position rather than a standalone bet. The exit: take profit before the 12-month mark, because the same history shows the dollar signal degrades at a year — if US growth re-accelerates and a new hawkish catalyst emerges, the siphon reasserts. The honest caveats: this all requires the Fed to actually hold (if it hikes, we are wrong), and being right is not the same as being early — which is exactly why we size and structure it the way we do.

Japan Equities — Own the Normalization & Bottleneck

Our Q2 barbell — long defence, long AI materials, underweight consumer — did its job. But the energy shock that powered the defence leg is now resolving, and that changes the trade. The data is blunt about it: across stress episodes, the defence outperformance collapses once the shock fades, and over the full 2022–2026 period the defence trade has been roughly flat-to-modest while the geopolitical premium came and went. Japanese defence names ran hard on the Iran spike (Kawasaki up ~40%); we take that gain rather than press a premium that fades as the Strait reopens.

What we keep, and lean into, is the trade that has quietly compounded through the entire normalization: banks. TOPIX Banks are up more than 360% since the start of 2022, and the acceleration maps almost exactly onto the BOJ's normalization milestones — the YCC tweak, the first hike, and now 1.00%. With rates only at 1% and rising, net-interest-margin expansion has further to run, so banks stay the core of our Japan equity book — with the honest caveat that after a move this large, this is "ride the normalization," not deep value. Alongside banks we hold the semiconductor and electronic-components complex — MLCCs, substrates, power semis, the names like Murata, Resonac, Nitto Boseki, Ibiden and Kioxia — which is both supported by the AI capex cycle and the direct bridge to the "bottleneck" theme from our US note; the same compute build that we own through memory and MLCCs in Part I, we own through Japanese components here. Insurers we keep on watch: J-ICS volatility has eased with the JGB curve, and a stabilized 10-year below 3% makes the oversold names a tactical opportunity rather than a solvency worry.

So the Japan equity book for H2 is: banks as the core normalization compounder; the components/semis complex as the AI-bottleneck bridge; defence trimmed as the war trade fades; insurers as a tactical watch. And unlike China, we like Japan at the index level too — the broad market has normalization, a cheap currency, and the AI build behind it; we simply see the sharpest risk/reward in banks and the components complex.

Summary — Trading the Gap Between Yesterday and Tomorrow

China and Japan are the same economy at two ends of one road, and the investment conclusion is the divergence, not the symmetry. China is early in the descent — a balance-sheet recession the authorities are treating with cyclical tools, a property correction with structural roots, a demand recession masked by exports, and an equity market that is cheap because earnings keep falling and because it has become the funding leg of everyone else's AI trade. We stay structurally cautious there: light on index beta, selective in the government-supported pockets (AI and the data-center build, banks and high-dividend, genuine Tier-1 stabilization), patient for the central put, and ready to flip fast if it comes. The renminbi we hold as the wrong kind of strength — range-bound 6.7–6.9, policy-anchored, a low-beta counterweight rather than a trend.

Japan is climbing out the other side. A central bank at 1.00% without a financial accident, banks compounding on normalization, the components complex riding the same AI build we own in the US, and a currency at a generational undervaluation that becomes the highest-octane expression of our core Fed view. We own the normalization and fade the war trade; and we run long yen as a disciplined window trade — triggered by the first sign the priced hikes won't be delivered, expressed through convexity, and harvested before the siphon can reassert.

The spine ties back to Part I: the next Fed move is not a hike, that misprice unwinds, the US rate differential compresses — and that is the engine under a stronger yen and a stable renminbi, while China stays the deliberate outlier because its problem was never American rates. Japan spent thirty years learning the lessons China is only beginning to confront. The opportunity is not to mistake one for the other — it is to trade the distance between yesterday and tomorrow.

This completes our 2026 H2 Global Economic Outlook. The roads ahead for China and Japan will not get easier — but the long road has always been the one worth walking, and it rewards those who hold their course through the fog, with conviction and a smile. To everyone who has shared a stretch of it with us, from the very first mile: thank you — and may the wind be always at your back.