THE WORLD'S NEW MAPS II — Plus One, or Plus Half?

The Indo-Pacific is being rebuilt as the world's factory — but not in the way the headlines suggest

On June 2, 2026, South Korea's main stock index closed at an all-time high of 8,801— having begun the year around 4,500, a near-doubling in five months that no other major market on earth came close to matching. Then, within days, it fell hard: down more than 4% in a single session on June 10, as a US-Iran flare-up, a soft American jobs report, and sudden doubts about AI valuations sent semiconductor shares tumbling. Taiwan's market suffered its largest-ever intraday point drop the same week, with chipmaking giant TSMC posting a record one-day decline.

That round trip — a historic melt-up followed by a violent wobble — captures the Indo-Pacific equity story in miniature. The cause of both the surge and the stumble was singular: artificial intelligence, and the chips that power it. The memory and processors at the heart of every AI data center are made almost entirely in Korea and Taiwan, and for most of 2026 the world could not get enough of them. High-bandwidth memory — the specialized chips feeding data to AI accelerators — has sold out for all of 2026, with manufacturers reporting gross margins of 60 to 70%, roughly double their normal levels. SK Hynix has reportedly contracted its entire year's output under multi-year deals.

It is tempting to read the Indo-Pacific story through this AI lens alone. That would be a mistake. The AI chip boom is the most dramatic chapter, but it sits on top of a deeper, decade-long story: the physical relocation of how the world makes almost everything. And the most important fact about that relocation is one the headlines rarely capture — it is far less complete, and far more dependent on China, than the word "diversification" implies.

In Part I of this series, we looked at how the Gulf is positioning itself as the connective tissue of global trade — the middle layer through which capital, energy and goods increasingly flow. This piece moves to where the goods themselves are made. And the central question for investors is deceptively simple: has the world really built an alternative to Chinese manufacturing, or has it just built a thinner disguise?

The assembly line moved. The supply chain behind it largely did not.

The Great Migration — and Its Hidden Limit

The phrase that has driven boardroom decisions for five years is "China plus one": keep your core production in China, but add a second base elsewhere to reduce risk. After the US-China trade war, COVID, and a cascade of supply shocks, no multinational wanted a single point of failure. The strategy worked, at least on the surface.

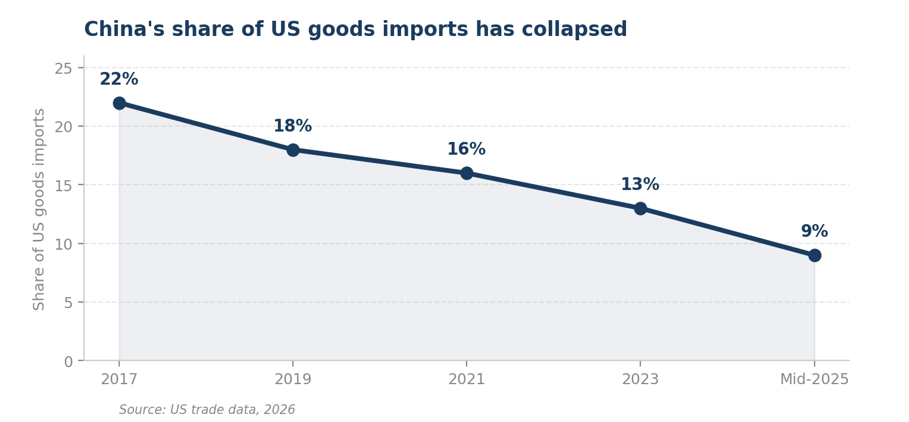

The numbers are striking. China's share of US goods imports has collapsed from a peak of 22% in 2017 to just 9% by mid-2025 — a level not seen since China joined the World Trade Organization a quarter-century ago. Production has visibly spread: Vietnam, India, Mexico, Thailand and Malaysia have all absorbed factories, jobs and capital that would once have gone to China.

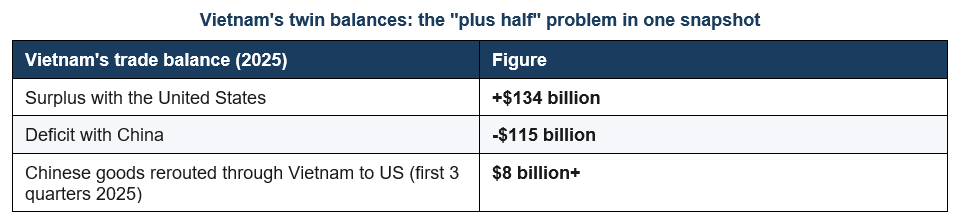

But here is the part the headline number hides. Much of what looks like diversification is, on closer inspection, rerouting. A 2026 study by researchers at Harvard, Duke and Academia Sinica found that more than $8 billion of Chinese exports were rerouted through Vietnam to the United States in just the first three quarters of 2025 — a reversal after two years of decline. As Vietnam's exports to the US have risen, so too have its imports of Chinese components and materials. Vietnam now runs a trade deficit with China exceeding $115 billion, even as it runs a $134 billion surplus with the US. The goods change their label in Hanoi; their guts still come from Shenzhen.

This is why analysts increasingly describe the reality not as "China plus one" but as "China plus half." The final assembly step has genuinely moved. The deeper layers of the supply chain — the components, the materials, the machinery — remain anchored in China. And in 2025, the US began closing even the assembly loophole, imposing transshipment tariffs of up to 40% on goods merely rerouted through third countries without genuine value added.

For investors, this is the single most important lens for the entire region. It separates the countries and companies building genuine, durable manufacturing ecosystems — which will survive the transshipment crackdown and compound over time — from those simply offering a temporary tariff arbitrage that is now being legislated away. With that distinction in hand, the Indo-Pacific resolves into three very different investment stories.

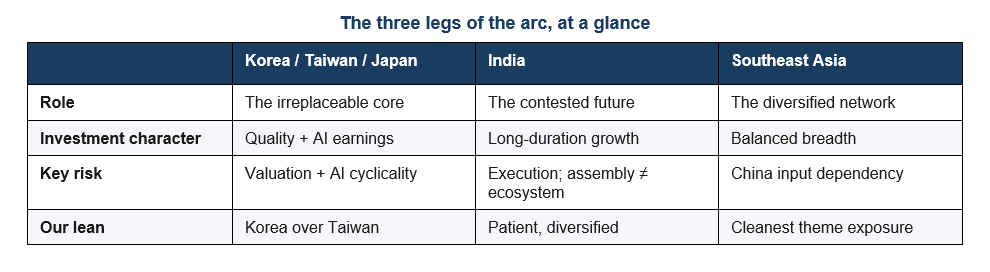

Korea and Taiwan: The Part That Cannot Be Copied

Begin at the top, because this is where the "plus half" problem disappears entirely. The most advanced chips in the world are made in Korea and Taiwan, and no amount of diversification can replicate them quickly. This is not cheap labor that can be relocated to Vietnam; it is decades of accumulated engineering, capital and supplier density that money alone cannot buy.

The AI boom turned that irreplaceability into staggering financial returns. Taiwan Semiconductor — which alone makes up roughly 40% of Taiwan's entire stock market — reported first-quarter 2026 revenue up 35% year-on-year, with net income up 58% and profit margins reaching 51%. Korea's market, dominated by Samsung and SK Hynix, was the best-performing major market on earth this year, the KOSPI roughly doubling to its June peak. The demand is real: up to 70% of all memory chips produced globally in 2026 are expected to be consumed by AI data centers. Even after the June pullback, Goldman Sachs raised its 12-month KOSPI target to 12,000, citing an "underpriced memory cycle" — though it is worth remembering that such targets are a single house's view, not a consensus.

Japan plays a quieter but equally unmoveable role. It does not dominate memory, but it controls critical upstream layers — the precision manufacturing equipment, the specialty materials and chemicals — that every chip fab on earth depends on. When a new plant is built in Arizona or Dresden, much of the equipment inside it is still Japanese.

The investment caveat is valuation and cyclicality — and the June selloff was a live demonstration of it. After the rally, Taiwan's market trades around 19 to 20 times forward earnings, above its five-year average. Korea, remarkably, still trades around 8 times forward earnings, below its historical average, because earnings have risen even faster than prices. That gap tells you where the crowded trade is and where value may remain — but memory is historically the most cyclical corner of technology, and the speed with which both markets fell in June, on nothing more than a shift in sentiment, shows how quickly today's extraordinary margins can be repriced. These are the highest-quality assets in the region and the most exposed to an eventual AI cooling.

Korea's market nearly doubled this year, then fell 4% in a day. Both moves had the same cause: AI.

India: The Great Ambition, and the Stubborn Number

If Korea and Taiwan are the irreplaceable present, India is the contested future — the country onto which the largest hopes, and the largest doubts, are projected.

The optimistic case is genuinely impressive, and Apple is its emblem. In barely five years, iPhone exports from India have gone from near zero to a record ₹2 trillion — about $22 billion — in the most recent fiscal year, making the iPhone India's single largest branded export. For the first time, in 2025, all models of Apple's newest iPhone were made in India at global launch, not just the older, cheaper ones. India now assembles close to a quarter of the world's iPhones, with Tata Electronics and Foxconn driving the build-out under a government incentive scheme that delivered a sixfold rise in electronics production.

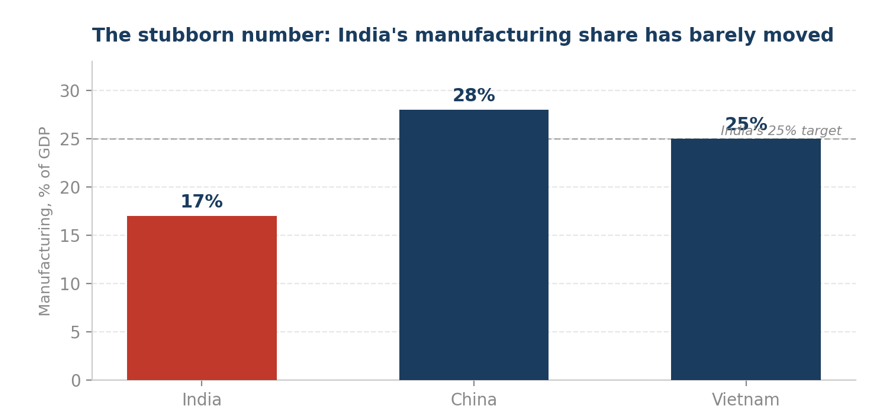

Now the stubborn number. Despite a decade of "Make in India," manufacturing's share of India's economy has barely moved — stuck between 16 and 17% of GDP, almost exactly where it was when the program launched in 2014. For comparison, manufacturing is around 25% of GDP in Vietnam and was close to 28% in China. India set a target of 25%; it has gone, in ten years, from roughly 16% to roughly 17%.

Why the gap between the dazzling Apple headline and the flat aggregate? Because India's success has been concentrated and shallow — heavy on final assembly of imported components, light on the deep supplier ecosystem that defines a true manufacturing economy. It is, once again, the "plus half" problem, in its sharpest form. India has also been an outlier in another way: while Korea, Taiwan and Japan soared on AI in 2025, India's market lagged badly, precisely because it has little direct AI-hardware exposure and investors rotated toward the chip story.

For investors, India is the region's clearest long-duration call — a vast domestic market, real policy momentum, and a genuine multi-decade runway. But it is a call on a trajectory, not a finished story, and the honest version acknowledges that the trajectory has been slower than the rhetoric for ten years running. It rewards patience and diversified exposure over single-name conviction.

Southeast Asia: The Network Effect

If India is one large bet, Southeast Asia is the most genuinely diversified manufacturing story in the world — and the one most often underestimated by investors who still picture it as a low-cost backwater.

The capital flows tell the story. Vietnam alone attracted a record $27.6 billion of realized foreign investment in 2025 — its highest in five years — with manufacturing taking nearly 60% of it. Its electronics exports reached $126 billion, a third of all export revenue, and it is now the world's second-largest smartphone exporter, producing about half of Samsung's global output. Its stock market hit record highs this year and is being upgraded by FTSE Russell to emerging-market status in September 2026, a change expected to channel billions of dollars of new investment.

But the deeper point is that each country has carved out a distinct, defensible role, and together they form a network that is far harder to disrupt than any single hub:

Vietnam — the electronics and assembly champion, climbing from pure assembly toward semiconductor packaging and testing as names like Amkor and Intel build advanced facilities.

Malaysia — the quiet powerhouse, already handling roughly 13% of the world's chip testing and packaging, now deliberately moving up into advanced packaging and chip design with Southeast Asia's largest IC design park.

Indonesia — the resource play, using its dominance in battery-grade nickel to force an EV and battery supply chain onshore rather than simply exporting raw ore.

Thailand and the Philippines — the established anchors of automotive electronics, power devices and the assembly-and-test backbone.

The whole region drew around $235 billion of foreign direct investment in 2024 — outpacing China outright. The same "plus half" caveat applies: much of the input supply chain still runs back to China, and the transshipment crackdown will test which operations have built genuine local value. But as a collective, distributed bet on the supply-chain shift, Southeast Asia is the most balanced exposure available.

No single country is replacing China. Together, Southeast Asia is building something more durable — a network, not a hub.

Our View: Following the Value, Not the Headlines

The reorganization of the Indo-Pacific is structural and durable. But the "plus half" reality means the easy narrative — that the world has cleanly diversified away from China — is wrong, and investing on that false premise is dangerous. Our framework follows where genuine, defensible value is being built.

Korea, Taiwan and Japan are the quality core. They hold the part of the chain that cannot be copied, and the AI cycle has handed them exceptional earnings. We would lean toward Korea's relative value over Taiwan's more crowded, TSMC-concentrated trade, while respecting that both are exposed to an eventual AI cooling and to the geopolitical and energy risks that come with such extreme concentration. This is the place to own quality, sized with cyclicality in mind.

India is the patient structural allocation. The runway is real, but ten years of a flat manufacturing share argues for humility on timing. Best held as a long-term position through diversified vehicles, with the explicit understanding that the assembly-to-ecosystem transition is the thing to watch — and has not yet happened.

Southeast Asia is the balanced expression of the theme. Vietnam's market re-rating and FTSE upgrade, Malaysia's semiconductor ascent, and Indonesia's resource leverage offer genuine breadth. For investors who want the supply-chain shift without a single-country bet, this is the cleanest route.

For most clients, the most sensible approach is exposure to the whole arc — through regional and Asia-ex-China equity vehicles, the semiconductor and technology complex, and the multinationals whose capital expenditure flows into the region. The migration is a tide lifting the entire Indo-Pacific; betting on the tide is usually wiser than betting on one boat.

Ways to Express the View

For clients who want to translate this into positions, the theme can be accessed cleanly through US-listed instruments, without trading directly on Asian exchanges. The vehicles below are illustrative of how the view can be expressed across the three legs of the arc, not personal recommendations.

The quality core — Korea, Taiwan, Japan

The iShares MSCI South Korea ETF (EWY) is the most direct expression of the Korea memory story — Samsung and SK Hynix together make up over 40% of it — and was among the best-performing country ETFs in the world this year even after the June pullback. The iShares MSCI Taiwan ETF (EWT) offers the Taiwan exposure but is effectively a concentrated bet on TSMC at around 20% of the fund. For the single highest-conviction names, TSMC (TSM) and Samsung and SK Hynix — both accessible via ADR — remain the purest plays on the irreplaceable end of the chain. Consistent with our view, we would lean toward Korea's relative value (EWY) over the more crowded Taiwan trade, sized with the AI cycle's volatility — on full display in June — firmly in mind.

The long-duration call — India

Given the assembly-versus-ecosystem caveat, India is best held through diversified vehicles rather than single names. The iShares MSCI India ETF (INDA) is the standard broad expression. We would treat it as a patient, multi-year allocation rather than a momentum trade — India notably lagged the AI-driven Asian rally, which is precisely why entry valuations look less stretched than Korea or Taiwan.

The balanced expression — Southeast Asia

The VanEck Vietnam ETF (VNM) is the cleanest single-country access to the region's strongest manufacturing story, and the September 2026 FTSE emerging-market upgrade is a concrete, dated catalyst worth watching. For broader exposure, an emerging-markets-ex-China vehicle captures the whole supply-chain-shift theme — Korea, Taiwan, India and Southeast Asia together — while deliberately screening out the China dependency that, as we have argued, still sits underneath all of it. For most clients seeking the theme without single-country risk, this ex-China structure is the most coherent core holding.

A reasonable framework: an ex-China EM core for the structural theme, a Korea or semiconductor tilt for the AI-driven earnings, and a smaller, patient India position for the long-duration call — sized so that an AI-cycle correction would be uncomfortable but not damaging.

What Could Go Wrong

The China dependency is the whole game. If the "plus half" reality is the central insight of this piece, it is also the central risk. Because the deeper supply chain still runs through China, a serious disruption there — whether political, economic, or around Taiwan — would ripple through every "alternative" hub simultaneously. The diversification is real at the surface and thin underneath, and investors should never mistake the one for the other.

The transshipment crackdown reprices the arbitrage. The countries that thrived simply by relabeling Chinese goods face a reckoning as US enforcement tightens. This will separate winners from pretenders — and in the messy interim, it could disrupt trade flows and earnings across the region, including for genuine manufacturers caught in the enforcement net.

Concentration and the AI cycle cut both ways — as June showed. The Korea-Taiwan earnings miracle rests on an AI capital-expenditure boom that history suggests will eventually cool. The June selloff — a 4%-plus single-day KOSPI drop and a record intraday fall in Taiwan — was a reminder that this is not a distant risk but a live one. When sentiment turns, the most concentrated, most crowded semiconductor names, and the markets built on them, correct hardest and fastest. The same chips that drove the KOSPI to double can drive it back down, and a few sessions in June are evidence enough.

A map redrawn in pencil, not ink.

The world has spent a decade and trillions of dollars trying to build an alternative to Chinese manufacturing. It has succeeded in spreading the final assembly across a wider arc — from Korean chip fabs to Indian iPhone lines to Vietnamese electronics parks — and that shift is real, investable, and durable. But it has not yet succeeded in building genuine independence from China underneath. The map has been redrawn, but in pencil, not ink.

For investors, that is not a reason for skepticism — it is the key to discrimination. The genuine ecosystems will compound; the relabeling operations will fade. The Gulf, in Part I, is building the roads. The Indo-Pacific is building the factories. In our next piece, we turn to Europe — a region trying to rebuild industrial capacity it spent thirty years allowing to wither, and asking whether ambition and money can buy back what was lost.