The Short That Broke the Consensus

The Short That Broke the Consensus

How DeepSeek Triggered Wall Street's Biggest Deleveraging Event in 16 Years --- And What It Reveals About How Markets Really Work

On the morning of 27 January 2025, traders walked into their offices to find that a paper published over the weekend by an obscure Chinese AI lab had just erased nearly $600 billion from Nvidia's market value — the largest single-day loss in market capitalization for any company in human history. By the end of the week, hedge funds had experienced the most violent deleveraging event since the 2008 financial crisis.

The culprit was not a war, a rate hike, or a recession. It was a research paper. And the reason one paper could cause that much damage has everything to do with a mechanism most investors have never thought carefully about: short selling, and the hidden architecture of the securities lending market that makes it possible.

How Short Selling Actually Works

The mechanics described here reflect how short selling operates at the institutional level — hedge funds, prime brokers, and securities lenders. Retail investors can technically short stocks through their brokers, but the scale, leverage, and systemic impact that drive the events discussed in this piece are overwhelmingly the domain of institutional actors.

Covered vs. naked. In a covered short, the seller has already arranged to borrow the shares before the sale — this is the standard institutional practice. In a naked short, the seller sells shares without first locating or borrowing them, in effect selling shares that do not yet exist in their account. Naked shorting is prohibited in most regulated markets (including the U.S. under SEC rules) because it can artificially inflate the apparent supply of a stock. Certain exceptions apply to market makers. The GameStop saga, in which short interest exceeded 100% of the available float, raised questions about whether some portion of the outstanding shorts had effectively naked characteristics — shares lent, re-lent, and sold in a chain that created more short positions than underlying shares.

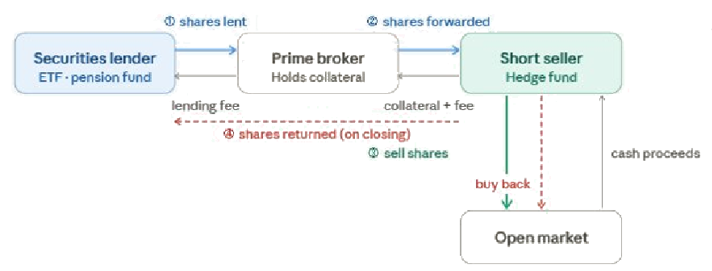

The four parties. Every institutional short trade involves four distinct actors: (i) the Short Seller — typically a hedge fund executing the directional bet; (ii) the Securities Lender — an institutional holder such as an ETF, pension fund, or mutual fund that loans out shares in exchange for a lending fee; (iii) the Prime Broker — an investment bank that intermediates the loan, holds collateral, and issues margin calls; and (iv) the Open Market — where the borrowed shares are sold and later repurchased. The diagram below shows how these parties interact at each stage.

The mechanics, step by step. It starts with borrowing. The hedge fund approaches its prime broker, which sources shares from a securities lender — typically an ETF or pension fund. The lender receives a lending fee; the hedge fund posts cash or high-quality bonds as collateral. Once borrowed, the shares are sold immediately on the open market. The short seller pockets the cash proceeds, then waits for the price to fall. If it does, they buy the shares back at a lower price, return them to the lender, and keep the difference as profit.

When it goes wrong. On every day the short position is open, the borrower must post collateral proportional to the market value of the borrowed shares. If the stock rises, the collateral becomes insufficient, triggering a margin call from the prime broker — an urgent demand for more cash. If the short seller cannot meet the margin call, the position is forcibly closed. They must buy back the shares immediately, at whatever price the market demands. That forced buying pushes the price higher, which triggers more margin calls, which forces more buying. This self-reinforcing loop is what a short squeeze is. The critical asymmetry: a long investor can only lose what they put in. A short seller, in theory, faces unlimited losses.

GameStop, January 2021: The Short Squeeze That Entered Public Consciousness

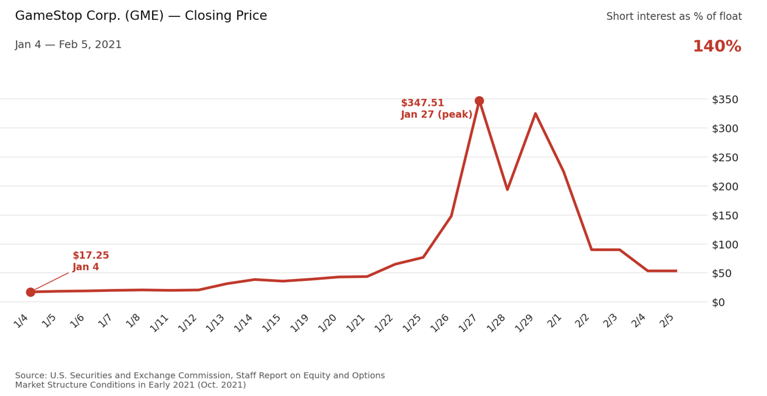

The concept of a short squeeze entered public consciousness in January 2021, when a crowd of retail investors on Reddit identified that GameStop — a struggling video game retailer — had short interest equivalent to 140% of its public float. That meant shares had been borrowed and re-lent multiple times over. Goldman Sachs analysts noted at the time that short interest exceeding 100% of float had occurred only 15 times in the prior decade.

When retail investors began buying en masse, short sellers were forced to cover simultaneously. There were simply not enough shares in existence for an orderly exit. GameStop's share price went from $17.25 at the start of January to an intraday high of $483, a rise of nearly 2,800% in less than a month. Melvin Capital, one of the largest short sellers, lost 53% of its assets and required a $2.75 billion emergency injection.

GameStop was extreme because the short interest was extreme. But the underlying mechanism — everyone trying to exit the same door at the same time — is neither rare nor limited to small-cap stocks. The chart below captures the arc clearly: the stock opened January 2021 at $17.25, surged to an intraday peak of $483 on 28 January as forced buying exhausted itself, then collapsed as rapidly as it rose. As a postscript, GME now trades at approximately $23.40 — a 95% decline from that peak, and a reminder that a short squeeze amplifies price beyond any fundamental anchor, in both directions.

DeepSeek, January 2025: When the Crowded Trade Breaks

GameStop was a story about one stock. What DeepSeek triggered in January 2025 was something structurally different and far more revealing: the simultaneous unwind of an entire market's most crowded long position.

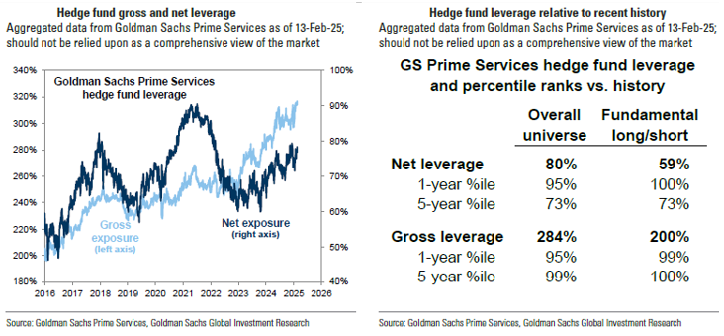

Hedge fund gross and net leverage tracked by Goldman Sachs Prime Services (as of 13 February 2025). Gross leverage reached the 99th percentile on a five-year basis at the start of 2025, marking the point of maximum crowding that preceded the DeepSeek-driven unwind. Source: Goldman Sachs Prime Services, Goldman Sachs Global Investment Research

Throughout the second half of 2024, global hedge funds had accumulated enormous exposure to AI-related technology stocks. Nvidia, Microsoft, Meta, and Alphabet were among the most concentrated positions in the industry. Goldman Sachs' prime brokerage desk noted that funds still holding AI positions at the start of 2025 had reached their highest long exposure in two years. It was precisely at this peak of exposure that they were most vulnerable.

DeepSeek's emergence shattered the consensus. If a Chinese lab could match U.S. AI capability at a fraction of the cost, the entire investment thesis underpinning hundreds of billions in positions was suddenly in question. Funds that had been gradually reducing AI exposure over the prior months avoided most of the damage. Those still fully invested had no good options.

Goldman Sachs reported that the volume of single-stock selling on 27 January was the largest it had seen in roughly six months, and among the highest levels in the past five years. Hedge funds fled technology stocks for the third consecutive session, squeezed out of long positions that had become too risky to hold. In total, hedge fund gross leverage fell 7.5% in a single day and 10% across the week — the largest active deleveraging since February 2009.

The irony was sharp: the session's biggest winners were systematic short sellers — funds that had been quietly betting against the weaker companies in the AI ecosystem. They finished the day up 1.7%, while their long-oriented peers suffered losses dropping into billions.

This is the nature of crowded positioning: when the consensus trade reverses, the exit is never wide enough.

Gold, December 2025: The Christmas Squeeze

For investors who assume short squeezes are a technology sector phenomenon, the gold market offered a reminder in December 2025 that leverage and borrowed positions can create the same dynamics anywhere.

The COMEX futures market trades vastly more "paper gold" each day than physical gold actually exists in deliverable form. Most contracts are closed or rolled before delivery is required — a functioning system, until it is not. On Christmas Eve 2025, holiday-thinned liquidity and a sudden geopolitical headline created the conditions for a classic squeeze: short sellers with nowhere to hedge, forced to cover at any price. Gold surged more than $40 per ounce in a single Asian trading session.

TD Securities noted afterward that the event exposed how fragile gold short positions had become, and that any positive news in 2026 risked triggering another rapid ascent. For HNW investors holding gold, the distinction between an ETF (paper exposure) and physical bullion matters precisely in moments like these. In a squeeze, they do not behave the same way.

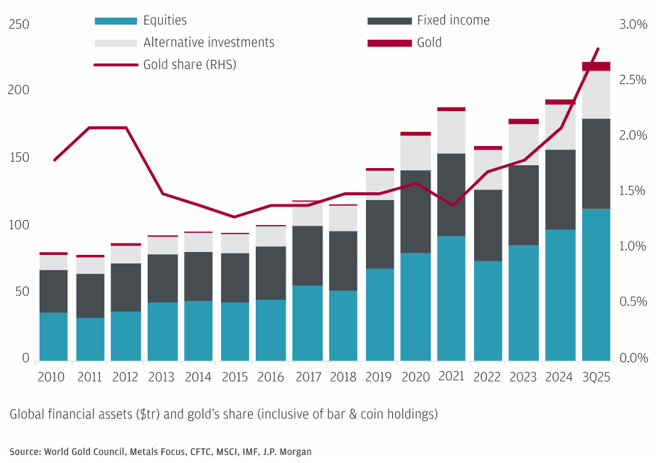

Gold’s share of global financial assets rose to approximately 2.8% as of Q3 2025, its highest level in over a decade, driven by sustained central bank accumulation and growing ETF inflows.

US/Israel–Iran, February–April 2026: Geopolitics as a Deleveraging Trigger

The most recent illustration arrived on 28 February 2026, when coordinated US-Israeli strikes on Iran killed Supreme Leader Khamenei and set off one of the most severe deleveraging episodes in recent memory. Brent crude surged toward $120 a barrel as markets priced in sustained disruption to the Strait of Hormuz; gold rallied above $5,300 per ounce. Hedge funds responded by selling global equities for a fourth consecutive month at the fastest pace in 13 years — fundamental long/short managers down over 5% in March alone, with Asia-focused funds bearing the worst of it at –7.3%. Systematic strategies, as in January 2025, finished the month in positive territory.

What separates this episode from DeepSeek or GameStop is the absence of a resolution signal. With DeepSeek, the market could model a new competitive landscape and reprice. With an active military confrontation, the range of outcomes is wide and the timeline is undefined. Funds reduce positions not because they have a view, but because they cannot afford to be wrong — and that forced selling, untethered from any fundamental reassessment, is precisely what makes geopolitical shocks so disruptive to levered portfolios.

Three Things Every Investor Should Take Away

Takeaway 1 — Crowded positioning is the market's most underappreciated risk. When everyone holds the same trade, the risk is not that the trade is wrong — it is that everyone realizes it is wrong at the same time. Goldman Sachs publishes its "Most Shorted" basket and "Hedge Fund VIP" long basket specifically to track where crowding is most acute. Elevated readings are worth watching.

Takeaway 2 — Your ETF may be a short seller's supplier. Many funds participate in securities lending programmes, earning incremental returns by lending out holdings to short sellers. This is not inherently problematic — but it means the mechanics described in this piece are not abstract. They flow through the products in your portfolio.

Takeaway 3 — In a squeeze, liquidity matters more than direction. The most violent moves happen when liquidity is thinnest — holiday sessions, early Asian hours, periods of low market volume. Leveraged positions held through these windows carry costs that compound quickly. The right question in uncertain markets is not only "am I positioned correctly?" but "can I stay positioned if the market moves against me for longer than expected?"

Short selling is not a villain in the financial system. It provides liquidity, corrects overvaluations, and, as January 2025 showed, sometimes it is the short sellers who are the calm ones in the room. The episodes described in this piece — DeepSeek, the gold Christmas squeeze, and the US/Israel–Iran deleveraging — are not anomalies. They are recurring features of a market in which leverage is always present and exits are always narrower than they appear. Understanding how short selling works — and how it can break — gives every investor a clearer picture of the forces that move markets, especially when they move fastest..