The USD/JPY Game:What Really Moves the Yen, and Why Bank of Japan Interventions Aren't a SilverBullet

.png)

The efficacy of central bank foreign exchange intervention remains one of the most contested issues in international finance. The critical question facing market participants and policymakers is straightforward yet profoundly complex: when the Bank of Japan enters the market to buy or sell the yen, does such intervention genuinely influence the exchange rate trajectory, or is it merely a symbolic gesture overwhelmed by larger market forces? This inquiry demands a multi-dimensional analytical framework that synthesizes insights from monetary policy transmission, risk dynamics, and market structure. By employing advanced econometric methodologies that move beyond mean effects to examine distributional impacts across varying market regimes, we reveal a nuanced hierarchy of drivers where intervention occupies a distinctly subordinate and context-dependent position. The evidence points toward a sobering conclusion: while interventions can serve as short-term stabilization mechanisms in specific circumstances, their sustained influence is fundamentally constrained by more powerful structural forces and often undermined by internal policy contradictions.

The Hierarchical Architecture of USD/JPY Determinants: Structural Forces Overriding Discretionary Policy

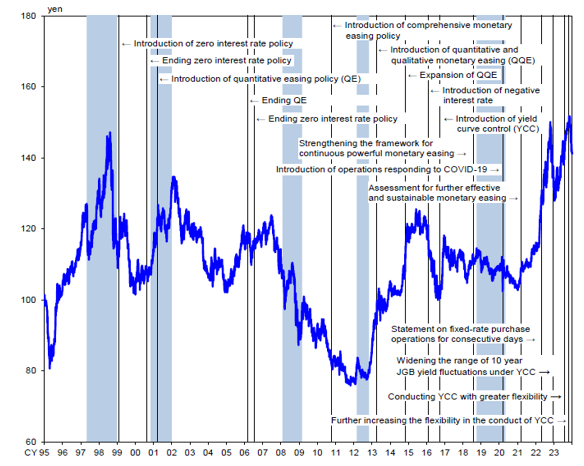

The foreign exchange market for USD/JPY operates within a clearly defined hierarchy of influences, where structural macroeconomic and financial factors consistently dominate discretionary policy actions. At the apex of this hierarchy resides the interest rate differential between the United States and Japan, a fundamental driver that channels global capital flows through carry trade mechanisms. The persistent divergence in monetary policy stances since the global financial crisis—with the Federal Reserve normalizing policy while the Bank of Japan maintained extraordinary accommodation—has created a powerful and sustained incentive structure for market participants. Empirical evidence from the Bank of Japan's working paper demonstrates that while unconventional policies affect the entire yield curve, the traditional interest rate differential channel explains only a modest portion of exchange rate responses, suggesting that other transmission mechanisms may be more significant. Most compellingly, the detailed examination of yen carry trade build-up directly correlates the post-2022 widening of the US-Japan yield spread with increased speculative positioning against the yen, confirming that this differential serves as the primary fuel for directional trends that interventions must confront.

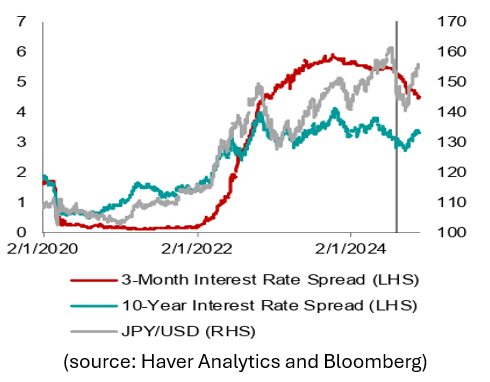

The interest rate spread is based on 3-month and 10-year government securities of Japan and the U.S. The vertical grey line marks the period of the BOJ's announcement on raising interest rates at July 31, 2024.

Simultaneously operating as a critical and often countervailing force is global risk appetite, systematically measured through volatility indices such as the VIX. The Japanese yen's entrenched status as a premier safe-haven currency creates a reflexive relationship between financial market stress and yen appreciation that frequently operates in opposition to interest rate differential effects. The Bank of Japan's analysis contextualizes this dynamic, noting that during periods of global financial crisis, safe haven flows into the yen effectively mitigated the depreciation effects that might otherwise have resulted from Japan's unconventional easing policies. The August 2024 episode, meticulously documented by AMRO, exemplifies this mechanism in action, where rising volatility triggered simultaneously carry trade unwinds and safe-haven inflows, resulting in sharp yen appreciation that temporarily overrode the still-favorable interest rate differential for dollar holdings. This dualistic framework—where interest rate differentials and risk sentiment operate as primary, often opposing forces—establishes the challenging environment within which interventions must function.

Within this established hierarchy, direct foreign exchange interventions occupy a distinctly tertiary position, their efficacy heavily contingent on alignment with or absence of strong opposition from these dominant structural forces. The application of quantile regression methodologies to intervention analysis reveals a telling asymmetry in outcomes: interventions demonstrate measurable stabilizing effects primarily during conditions of pronounced but orderly yen depreciation or during episodes of dysfunctional market behavior characterized by excessive volatility and liquidity constraints. Under such circumstances, carefully timed and adequately sized interventions can moderate the pace of decline, restore two-way price discovery, and reestablish market functioning. However, this effectiveness diminishes rapidly when interventions confront entrenched trends driven by widening interest rate gaps or when they are implemented during periods dominated by extreme speculative positioning that reflects genuine macroeconomic divergence. The Bank of Japan's finding that exchange rate responses to policy shocks are "state-dependent"—varying significantly with global financial conditions and investor herding behavior—reinforces this contingency. Thus emerges the fundamental asymmetry of intervention outcomes: while potentially effective as circuit breakers during specific market stress scenarios, interventions generally prove insufficient to counteract or reverse powerful fundamental trends sustained by structural economic forces.

The Paradox of Policy Implementation: How Internal Contradictions Undermine Intervention Credibility

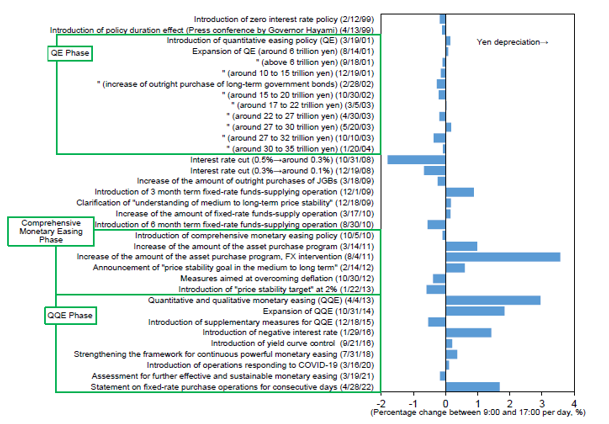

The effectiveness of foreign exchange interventions cannot be assessed in isolation from the broader policy framework within which they are deployed and herein lies a profound paradox that fundamentally constrains the Bank of Japan's operational efficacy. Japan's economic governance structure embodies a constitutional separation of authority that frequently produces conflicting policy impulses: the Ministry of Finance, exercising jurisdiction over exchange rate policy, typically authorizes interventions with the objective of curbing excessive yen weakness to manage import costs and domestic inflationary pressures. Yet this objective exists in stark, almost irreconcilable tension with the Bank of Japan's longstanding commitment to an ultra-accommodative monetary policy stance characterized by negative policy rates, yield curve control, and massive balance sheet expansion—all policies that inherently promote yen depreciation through the perpetuation of interest rate disadvantages relative to major trading partners.

This internal contradiction creates a credibility deficit that market participants quickly internalize and arbitrage. When interventions are perceived as fighting against the fundamental thrust of monetary policy, they are essentially attempting to strengthen a currency that the central bank's primary policy tools are designed to weaken—their psychological impact diminishes, and their financial sustainability becomes questionable. The Bank of Japan's own analysis indirectly acknowledges this tension through its documentation of how non-interest rate channels, particularly shifts in market expectations and narratives, often dominate the exchange rate response to policy announcements. When interventions lack narrative consistency with the overarching monetary policy framework, their capacity to alter expectations sustainably is severely compromised. Market participants rationally question whether the authorities possess either the commitment or the resources to maintain intervention efforts indefinitely against the tide of monetary divergence, particularly when such efforts directly conflict with domestic price stability objectives.

Furthermore, the specific mechanics of intervention implementation often reveal additional constraints that limit effectiveness. Sterilized interventions—the predominant modern approach—merely alter the currency composition of central bank assets without affecting domestic monetary conditions, thereby diluting their impact on interest rate differentials. Unsterilized interventions, while potentially more powerful through their monetary transmission channels, directly conflict with the Bank of Japan's yield curve control framework and could destabilize domestic bond markets. This operational bind means that interventions are frequently designed and executed as limited tactical operations rather than strategic commitments, a reality that sophisticated market participants recognize and incorporate into their positioning strategies. The result is a predictable pattern of short-term volatility suppression followed by eventual reversion to fundamental trends, a pattern that further entrenches the market's hierarchical assessment of drivers and diminishes the long-term credibility of the intervention tool itself.

Empirical Patterns and Market Regimes: When Interventions Work and When They Fail

Historical analysis of Bank of Japan intervention episodes reveals distinctive patterns that correspond to specific market regimes, providing empirical validation for the contingency framework outlined above. During periods characterized by moderate interest rate differentials and contained volatility, what might be termed "normal" market conditions, interventions typically demonstrate limited and transient effects, with exchange rates reverting to pre-intervention trends within days or weeks. In such environments, the dominant structural forces lack sufficient momentum to create extreme positioning, and interventions can temporarily influence price action through liquidity and signaling effects. However, their impact remains superficial rather than transformative.

Contrastingly, during "directional stress" regimes are dominated by rapidly widening interest rate differentials and strong consensus positioning—such as the 2022-2024 period of sustained Fed tightening versus BOJ accommodation—interventions consistently demonstrate minimal efficacy. The Bank of Japan's own research identifies this limitation through its finding that while expansionary monetary policy shocks generally produce yen depreciation, the conventional interest rate channel explains only a small portion of the response, with non-interest rate channels dominating. In such regimes, interventions face what might be termed a "force mismatch": the financial incentives created by hundreds of basis points of yield differential generate capital flows of such magnitude that even large-scale interventions represent merely a fractional counterforce. The market recognizes this imbalance and accordingly the intervention impact of discounts, treating announcements as temporary noise within an established trend.

The most favorable regime for intervention effectiveness emerges during "disorderly market" conditions characterized by extreme volatility, collapsing liquidity, and potentially self-reinforcing price movements that deviate from fundamental valuations. Their effectiveness derives not from overpowering structural forces but from addressing market failures: by providing liquidity when private participants have withdrawn, by establishing credible price boundaries that contain panic-driven feedback loops, and by coordinating market expectations around central bank commitment to functionality.

Implications for Market Participants: A Disciplined Analytical Framework

For financial market participants operating in the USD/JPY market, the hierarchical model of exchange rate determination demands a disciplined analytical framework that prioritizes structural drivers over discretionary policy actions. The primary focus of analysis must remain firmly on monitoring and interpreting the evolution of US-Japan interest rate differentials across the yield curve, with particular attention to forward-looking expectations embedded in derivatives markets. This differential serves not merely as an observable data point but as a powerful predictor of capital flow direction and magnitude, with widening spreads favoring dollar strength and narrowing spreads potentially supporting yen recovery.

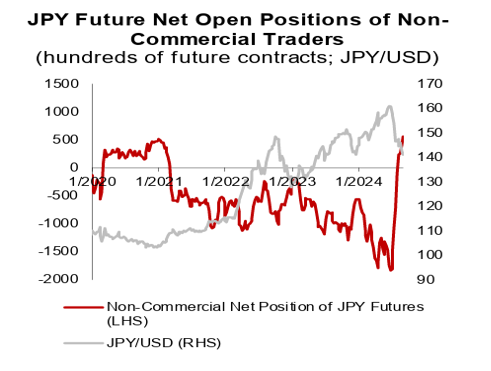

Concurrently, systematic tracking of global risk sentiment through the VIX and related volatility measures provides crucial insight into potential countervailing forces that may temporarily override interest rate effects. Gregory's quantification of the VIX-exchange rate relationship offers empirical validation for incorporating volatility metrics into trading models and risk management frameworks. Furthermore, monitoring speculative positioning through Commitment of Traders reports, net open interest in yen futures, and indications from the offshore lending market—all methods employed in the AMRO study—offers valuable signals regarding market crowding and vulnerability to sudden reversals.

Within this comprehensive analytical structure, announcements of central bank intervention should be interpreted through a strictly conditional lens. Rather than viewing interventions as autonomous signals of trend reversal, market participants should assess them as tactical operations whose likely impact depends critically on their alignment with the prevailing market regime. Interventions implemented during disorderly market conditions with extreme volatility may present opportunities to fade exaggerated moves, while those deployed against powerful directional trends driven by fundamental divergence are likely to provide only temporary respites. Most importantly, the consistency—or lack thereof—between intervention objectives and the broader monetary policy framework must be evaluated, as contradictory policy signals dramatically diminish intervention credibility and staying power.

Conclusion: Intervention as Conditional Stabilizer Within a Structural Hierarchy

Structural financial variables—principally relative interest rates and global risk sentiment—constitute the dominant determinants of USD/JPY exchange rate dynamics, establishing a powerful hierarchy that discretionary policy actions must acknowledge and accommodate. Within this hierarchy, central bank interventions function not as primary drivers but as conditional stabilizers: potentially effective in specific market regimes characterized by disorderly conditions and exaggerated movements but fundamentally subordinate to more powerful and persistent structural forces. For market practitioners, this reality demands analytical discipline that prioritizes structural drivers while incorporating interventions as tactical factors whose impact depends on regime conditions.

Ultimately, the question of whether Bank of Japan intervention "works" receives a nuanced but definitive answer: We believe that it works conditionally, temporarily, and within strict boundaries defined by larger structural forces. This conditional effectiveness, properly understood and implemented, represents not a policy failure but a realistic assessment of what discretionary exchange rate management can reasonably achieve in deeply integrated global financial markets. The true measure of policy sophistication lies not in denying these constraints but in operating effectively within them, using interventions as precision instruments rather than blunt forces, and recognizing that sustainable exchange rate stability ultimately depends more on coherent macroeconomic frameworks than on discrete market operations.

Anyway, foreign exchange trading is not a casino; it is a rigorous discipline that demands careful consideration and profound respect for market dynamics. Unlike games of chance where outcomes depend on random probability, currency markets operate within a framework of macroeconomic fundamentals, geopolitical developments, and intricate financial interdependencies. Each trade represents an exquisite decision based on analysis of interest rate differentials, inflation trajectories, central bank policies, and global risk sentiment—not a mere gamble on short-term price movements.