Stock Market Weather Forecast — VIX

In financial markets, the VIX (Chicago Board Options Exchange Volatility Index) is almost universally recognized, often dubbed the “Fear Index.” Headlines typically scream “VIX surges, investor panic” whenever equities sell off. But to view VIX purely as a sentiment barometer is overly simplistic.

For professional investors, VIX is far more than a mood gauge — it’s a core tool for risk management, portfolio construction, and even systematic arbitrage. This note takes an institutional perspective to unpack what the VIX really measures, why it matters, and how it is practically applied.

The Essence of VIX

The VIX was introduced in 1993 to provide a standardized measure of expected volatility. Unlike equity indices, it isn’t the outcome of buying and selling but a model-derived number based on a basket of S&P 500 options.

In plain terms, VIX doesn’t predict whether stocks will go up or down. Instead, it answers: how much are investors willing to pay for “insurance” on the S&P 500 over the next 30 days?

To understand VIX, you must first understand implied volatility (Implied Volatility, IV). Historical volatility looks backward at realized price swings, while Implied volatility looks forward, inferred from option prices via the Black-Scholes model. When investors scramble for puts to hedge against a selloff, option prices rise, IV spikes, and so does the VIX. Just like insurance premiums rise when risk is perceived to be higher.

How the VIX Is Calculated?

The VIX comes from the following steps:

1. Option selection: Near- and next-month S&P 500 options expiring in 23–37 days are included.

2. Strike coverage: A broad strip of calls and puts across strikes are used.

3. Variance inference: Prices are used to derive the market’s implied distribution of returns.

4. Conversion: Variance is annualized and square-rooted into volatility — the VIX.

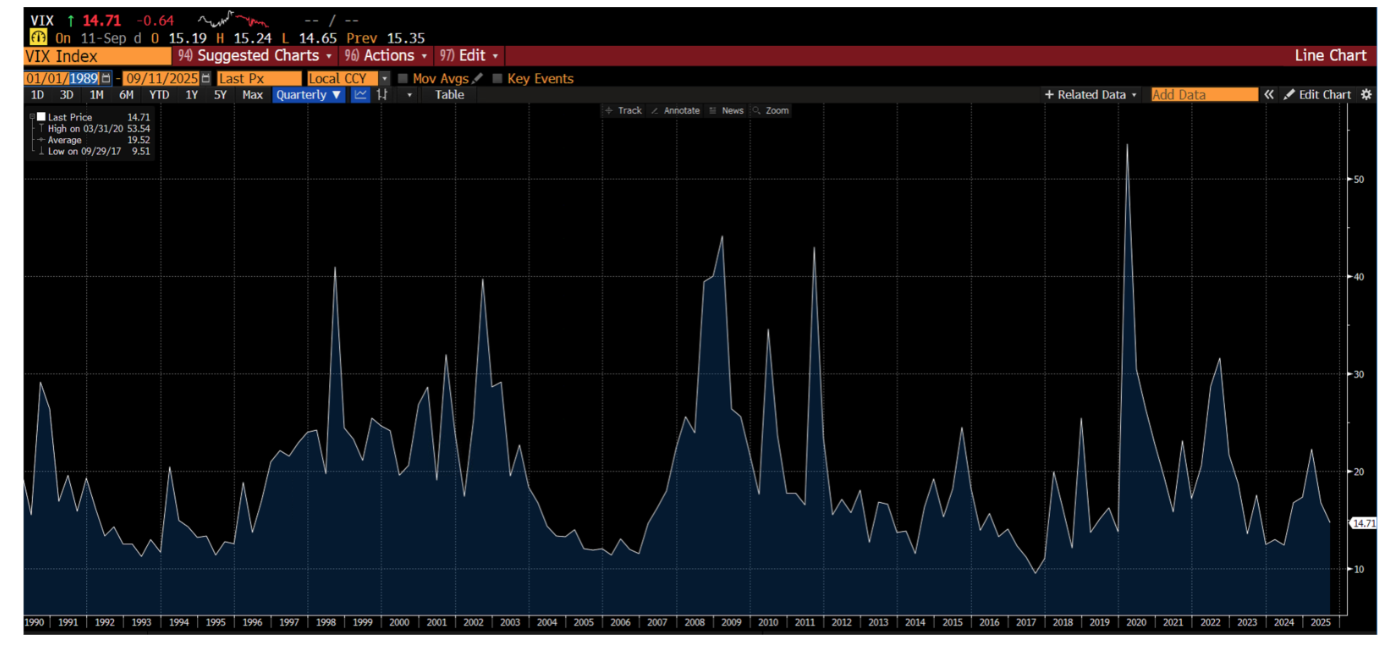

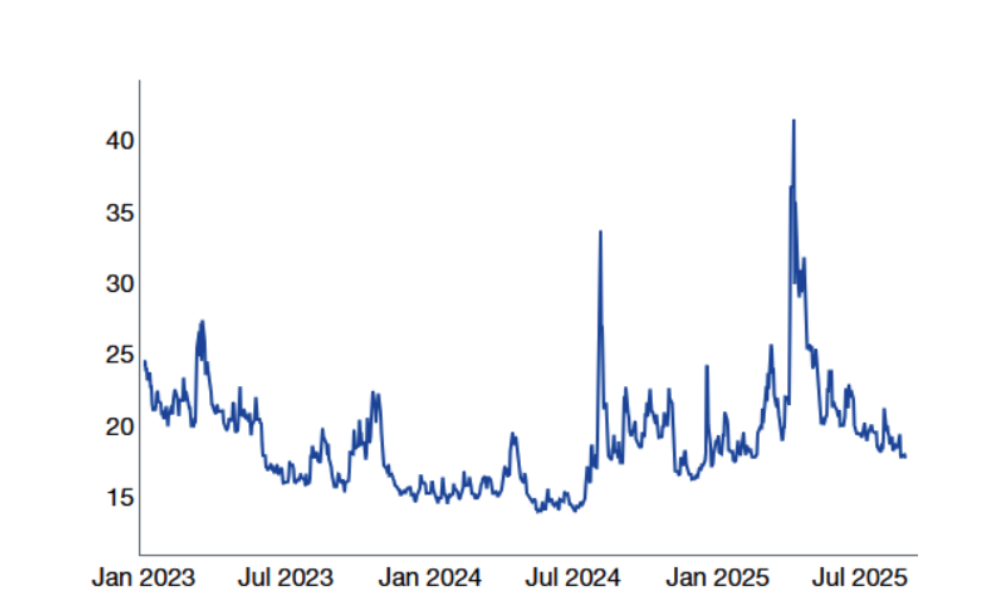

As seen above, VIX is essentially the collective wisdom of the options market, not a prediction from any single trader. Historically, VIX sits in the 10–40 range, but can spike beyond 80 in crises (e.g., 2008, 2020).

For example: a VIX of 20 implies the market expects the “annualized volatility” of the S&P 500 over the next 30 days to be about 20%. Converting to daily volatility gives about 20 ÷ √252 ≈ 1.25%, implying the market expects the S&P 500 to fluctuate about ±1.25% per day over the next month.

In summary: when the stock market plunges, investors rush to buy protective options → option prices rise → VIX surges; when the market rises, demand for insurance falls → VIX declines. This is why VIX is often called the “Fear Index” by the media.

Importantly, VIX rises far faster in selloffs than it declines in rallies — fear is asymmetric. For volatility traders, this “mean reversion” creates trading opportunity.

How Institutions Use VIX?

Although VIX itself is not tradable, its ecosystem of futures, options, and ETFs makes it investable. Institutions typically use it in three ways:

1. Hedging Tail Risk

The most established use case for VIX is as tail-risk protection. Funds holding sizable equity exposure often allocate a small portion of capital to long-dated, out-of-the-money VIX calls when premiums are inexpensive. The payoff profile is highly convex: in the event of a market shock, equity losses can be partially offset as VIX spikes and option values expand exponentially. This asymmetric protection is why VIX calls are widely regarded as an efficient form of “portfolio insurance” against low-probability, high-impact events.

2. Trading the terms

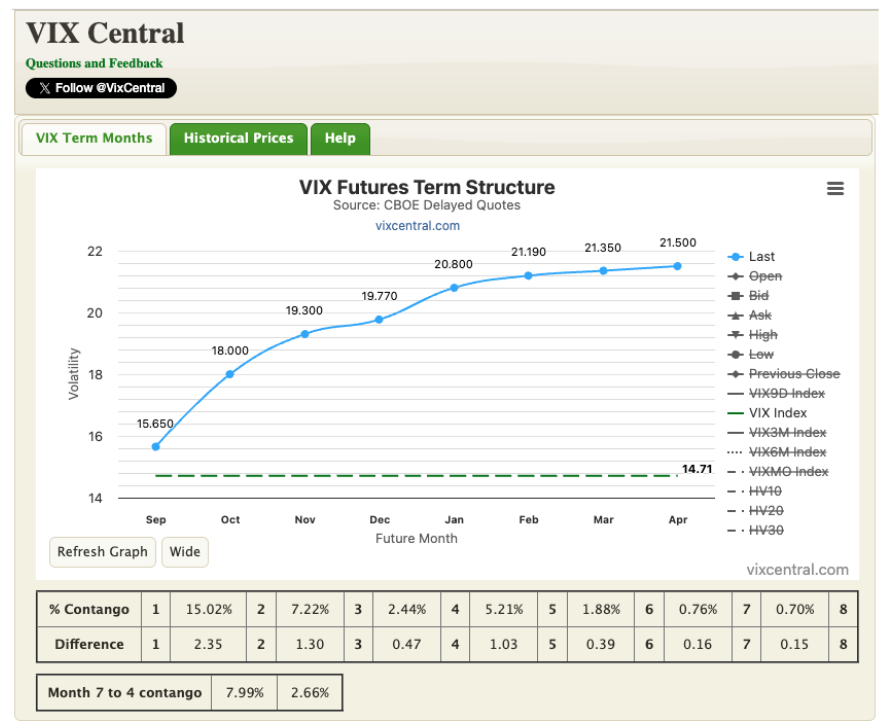

Institutional investors rarely limit themselves to simply going long volatility during periods of stress. A more sophisticated approach is to trade the term structure of VIX futures. In normal environments, the curve is upward-sloping (contango), reflecting expectations that near-term volatility will subside over time. During periods of acute market stress, however, the curve can invert into backwardation as demand for short-dated hedges surges.

Hedge funds actively arbitrage these dislocations — for instance, shorting elevated near-dated futures or volatility-linked ETFs (e.g., VXX, UVXY) — to capture the volatility risk premium, which exists because markets consistently overprice fear in the short run.

3. Asset Allocation

Beyond hedging and trading, VIX also plays a structural role in portfolio construction. As it tends to rise sharply during equity drawdowns, VIX is effectively uncorrelated — and often negatively correlated — with traditional asset classes such as stocks and bonds. This makes it a valuable diversifier and “shock absorber” in institutional asset allocation models. Incorporating VIX-linked instruments can improve portfolio resilience by cushioning downside risk when other assets fail to do so.

Structural Features of VIX

These features are often overlooked by retail investors but highly valued by institutions:

1. Mean Reversion

• VIX shows a clear mean-reverting tendency. Its long-term average is about 15–20, reflecting normal-market implied volatility levels.

• During major events (like a pandemic or financial crisis), VIX can spike to 40–50 or higher but rarely stays there long, as panic cannot persist indefinitely.

• For institutions, this means shorting VIX at high levels and going long at low levels often has a statistical edge. This forms the basis of many volatility-arbitrage strategies.

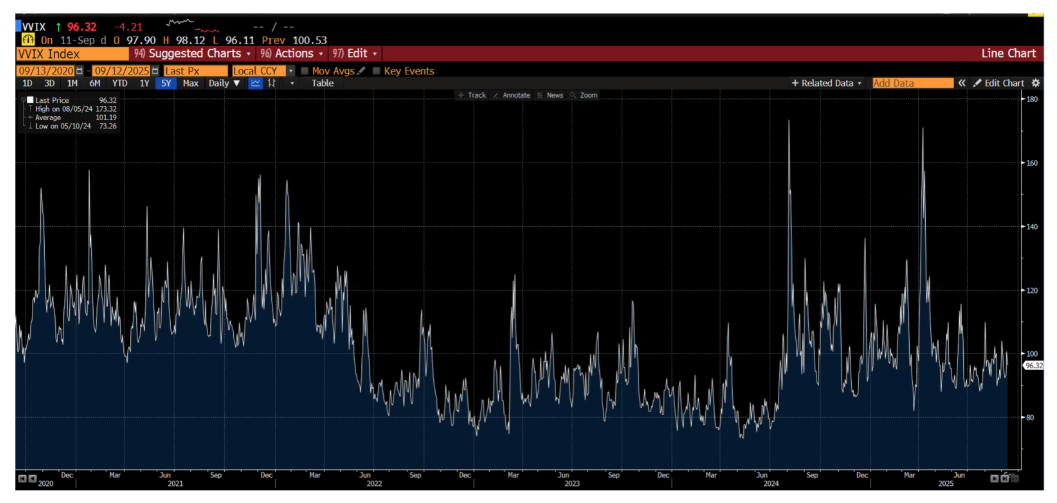

2. VVIX — The Volatility of Volatility

While the VIX measures implied volatility on the S&P 500, even volatility itself can be volatile. That’s what VVIX tracks — the implied volatility of VIX options. In effect, VVIX tells us how much investors are paying for uncertainty around “fear itself.”

When VVIX climbs in tandem with VIX, it suggests markets are not only pricing in fear, but also elevated anxiety about its persistence. Historically, this combination often precedes outsized swings in risk assets. For this reason, institutions track VIX and VVIX together as a way to separate short-lived panic from systemic risk episodes.

3. Term Structure and Roll Decay

The VIX is an index, but to trade it you need to use VIX futures. Prices across maturities form a term structure, which is normally in contango (far-dated futures > near-term futures) since volatility is expected to subside over time.

For exchange-traded products like UVXY, this creates a structural headwind: the fund must roll its futures exposure by selling cheaper expiring contracts and buying more expensive longer-dated ones. Over time, this “buy high, sell low” roll mechanic erodes NAV — a phenomenon known as roll decay. Leveraged products such as UVXY suffer this erosion even more acutely. This is why professional investors typically avoid long-term holdings in VIX ETFs and instead trade futures and options directly for cleaner exposure and precise hedging.

4. Volatility Risk Premium

A well-documented feature of markets is that implied volatility (VIX) consistently trades above realized volatility. Put differently, investors systematically overpay for insurance, just as auto insurance premiums exceed actual accident probabilities.

Institutions harvest this spread — the volatility risk premium — by selling options or shorting volatility-linked products. Strategies range from writing S&P 500 puts to selling straddles or shorting VIX futures. Over time, VRP has proven to be one of the most durable sources of return available to hedge funds and insurers, reflecting the market’s structural demand for protection.

How Can Investors Hedge with VIX?

If your portfolio has been concentrated in tech this year, you’ve probably enjoyed strong gains. But with valuations stretched and risk events building, it makes sense to dedicate a small portion of capital to hedging. The traditional approach is to use ETF put options, but VIX-linked instruments — particularly calls — are worth considering. The right tool depends on the risk you’re trying to manage.

VIX instruments are best in volatility-driven scenarios. Around major event risks — U.S. elections, FOMC decisions, earnings season — even modest market swings can trigger sharp increases in implied volatility. In those cases, VIX calls often deliver better protection per dollar than SPX puts.

They’re also useful when VIX is trading at historically low levels. Buying VIX calls when volatility is “cheap” is akin to buying black swan insurance — a small premium can provide outsized payoff in a crisis. Another edge is that VIX calls avoid the “directional decay” of puts. For example, if equities rally first, SPX puts can quickly lose value, and may not recover enough even if the market later corrects. VIX calls, by contrast, can still appreciate as volatility rises.

If the concern is a direct, sizable drawdown in equity prices — say 10%–20% — SPX puts are the cleaner hedge, since they track index performance more directly. They also allow you to structure explicit downside floors. For example, a 95% OTM put ensures your portfolio won’t fall below a pre-set level — something VIX options can’t replicate. Structured variants like put spreads or collars can also reduce premium costs while providing targeted protection.

At present, the VIX is trading around 14–15 — low by historical standards. While no one has a crystal ball, the setup is clear: markets are fully priced for Fed cuts, sentiment borders on complacency, and earnings (e.g., Oracle, Broadcom) are fueling AI optimism. With VIX’s strong mean-reversion tendencies, today’s low levels are unlikely to persist indefinitely.

For portfolios with concentrated exposures, we recommend considering VIX calls as a tactical hedge. They remain inexpensive (VVIX trading at 96) and can deliver asymmetric payoffs in stress scenarios. To control cost, investors can also look at VIX call spreads — for instance, buying the 15 strike and selling the 20 strike. This caps the upside but meaningfully reduces the premium outlay while still providing robust convexity to a volatility spike.