2025 Q4 Global Economic Outlook (II) - Japan & China

Big Picture

Since the LDP’s loss of both houses in July, market attention has centered on three questions: first, whether Japan could secure a constructive trade deal with the US; second, whether Ishiba would ultimately step down; and third, under such uncertainty, who will succeed as the next LDP leader — and when the BOJ will resume hiking. The first two questions now have clear answers; the third is quickly approaching the spotlight.

To frame our outlook, it is worth revisiting Japan’s trajectory over the past few years. Since March 2022, when the Fed began its most aggressive hiking cycle in history, the yen — as the world’s key negative-yielding funding currency — depreciated sharply against the dollar, sliding from 115 to 150 within just seven months. The carry trade was widely viewed as the main driver. While the weaker yen eroded purchasing power, it simultaneously boosted inbound tourism and, alongside fiscal expansion and the legacy of Abenomics, helped pull Japan out of decades of deflation. Rising inflation, in turn, drove stronger outcomes in the Shunto wage negotiations, with household wages climbing 5–6% yoy.

This virtuous cycle has been critical for Japan, and policymakers appear intent on sustaining it at almost any cost. Yet inflation has become increasingly difficult to manage. The Russia–Ukraine war amplified food prices for import-dependent economies, and despite nominal wage growth, real wages have remained negative. This deterioration in household purchasing power has fed into mounting dissatisfaction with the LDP. The absence of a strong leadership figure since Abe’s assassination in 2022 has further weakened the party, leaving even the LDP–Komeito coalition a minority in both houses.

The BOJ has, from an investor’s perspective, consistently lagged and failed us. With inflation persistent and the yen structurally weak, the rationale for maintaining ultra-loose policy has diminished. By global standards, the BOJ is “behind the curve.” Still, the BOJ appears guided by a different calculation: preserving the fragile gains of inflation. Having suffered through decades of deflation and wage stagnation, policymakers fear that tightening prematurely could extinguish this momentum. Their strategy has been to tolerate public frustration, accept a weaker yen, and maintain an exceptionally cautious tone — even at the risk of credibility — in order to entrench inflation expectations and secure a durable escape from deflation.

All Eyes on Oct 4

The Liberal Democratic Party (LDP) will hold its presidential election on October 4 following Prime Minster Shigeru Ishiba’s resignation announcement. With the official notice issued on September 22, five Diet members registered as candidates. Among them, Shinjiro Koizumi and Sanae Takaichi are widely regarded as the frontrunners.

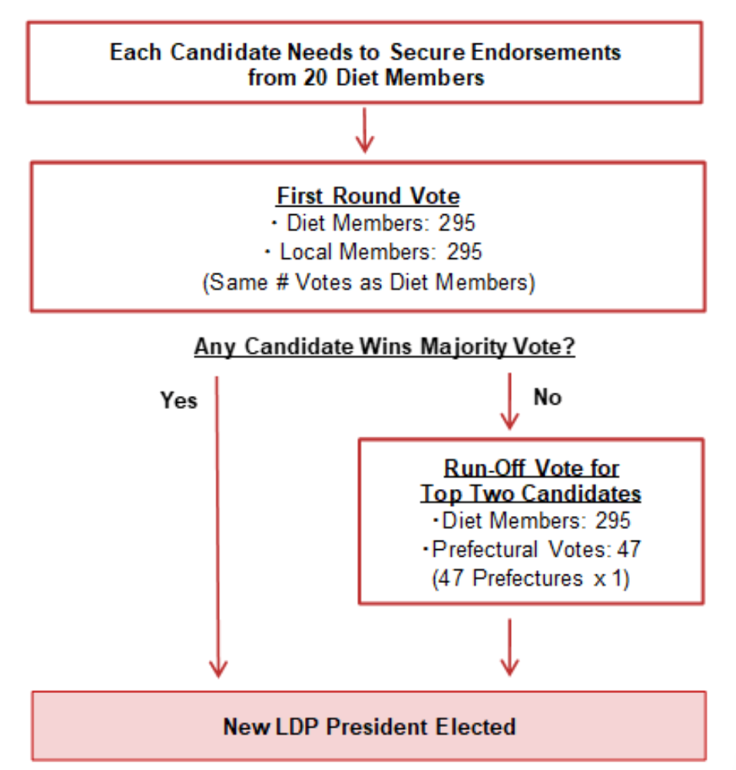

This will be a “full spec” election, with votes from both LDP Diet members and local party members. In total, 590 votes are cast: 295 from Diet members (one each) and 295 collectively from about one million party members. If no candidate wins a majority in the first round, the top two face a run-off, where Diet member votes remain at 295 but local party votes are reduced to 47 (one per prefecture), sharply increasing the influence of Diet insiders. With five candidates in the race, a run-off is highly likely.

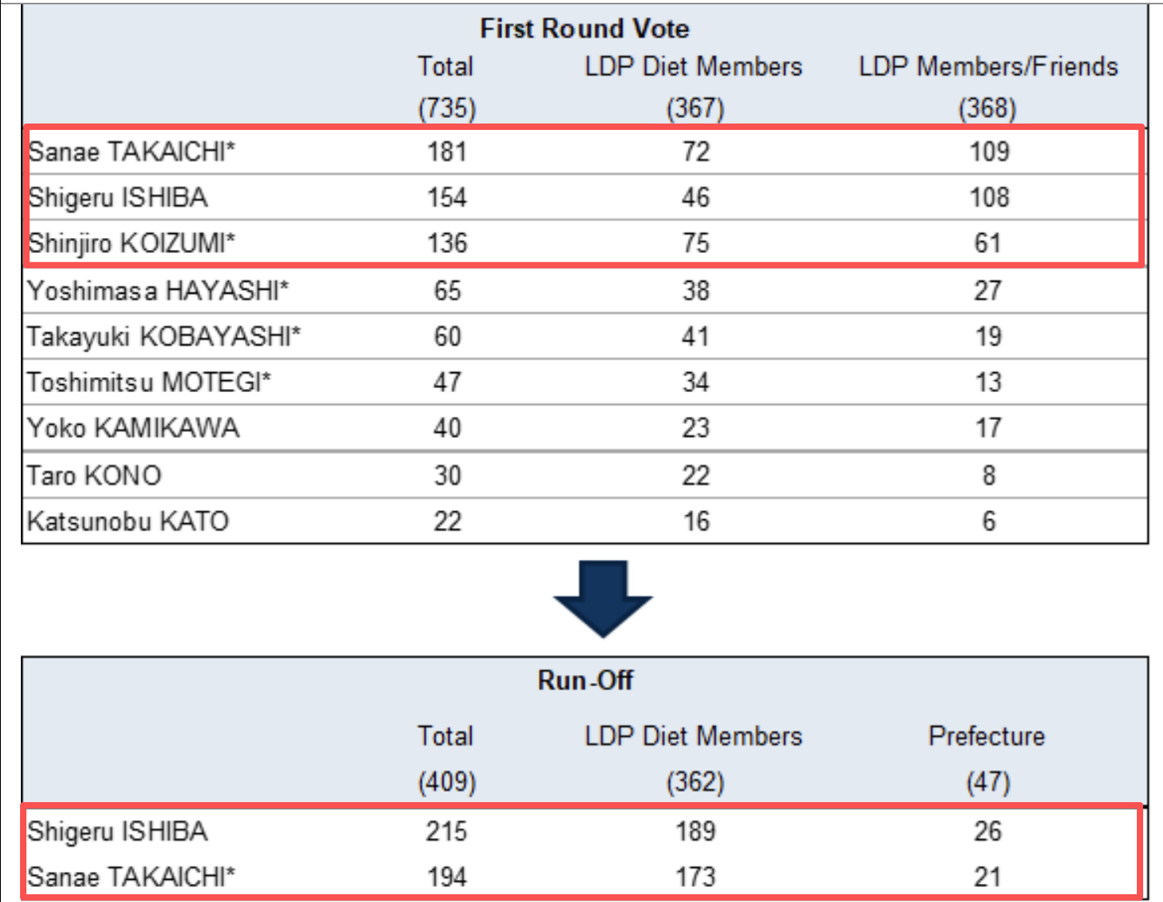

In last year’s election, Takaichi led in Diet member votes during the first round, but Ishiba ultimately prevailed in the run-off due to stronger consolidated support. Similarly, Shinjiro Koizumi topped the Diet member tally in the first round, highlighting his appeal within the parliamentary ranks.

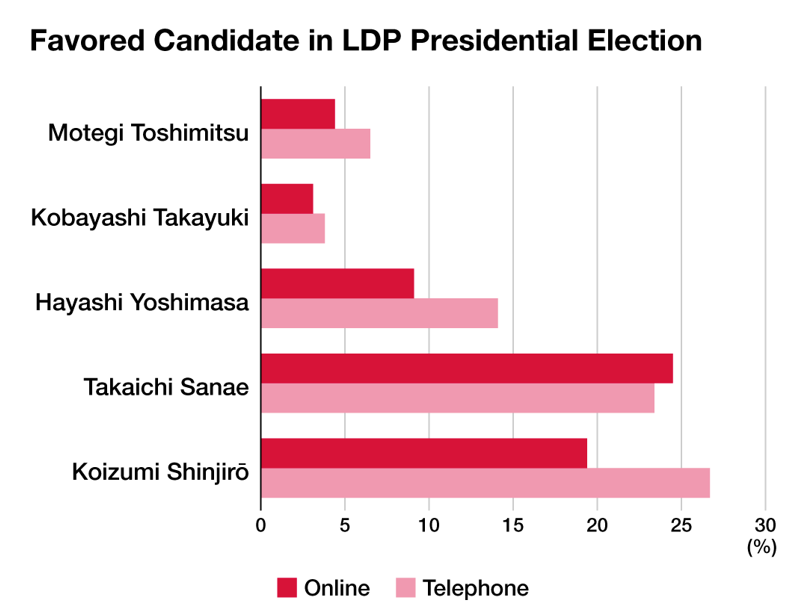

Turning to this cycle, Takaichi currently holds a narrow lead in nationwide opinion polls (23% vs. Koizumi’s 22%). However, the decisive factor will be the redistribution of support among LDP insiders given the voting nature. Notably, Ishiba met with former Prime Ministers Yoshihide Suga and Junichiro Koizumi (Shinjiro Koizumi’s father) just before his resignation. This suggests that a meaningful share of Ishiba’s backing could migrate toward Koizumi, especially given their policy alignment and shared hawkish stance on BOJ policy. Moreover, as a traditional major party, it remains uncertain whether the LDP is ready to accept both a female leader and a fiscal dove like Takaichi. Based on these factors, we judge that continuity- or centrist-aligned candidates such as Shinjiro Koizumi or Yoshimasa Hayashi have higher odds of winning.

On the policy front, inflation remains a dominant public concern. Should Takaichi pursue her expansionary fiscal agenda—typically associated with yen depreciation and upward inflation pressures—public dissatisfaction could intensify. Even if she were to win, she may be compelled to adopt a more hawkish stance to balance market stability with voter sentiment. In aggregate, we believe the LDP is inclined to select a centrist candidate to safeguard both political continuity and economic stability. Let’s see tomorrow!

BOJ Tightening?

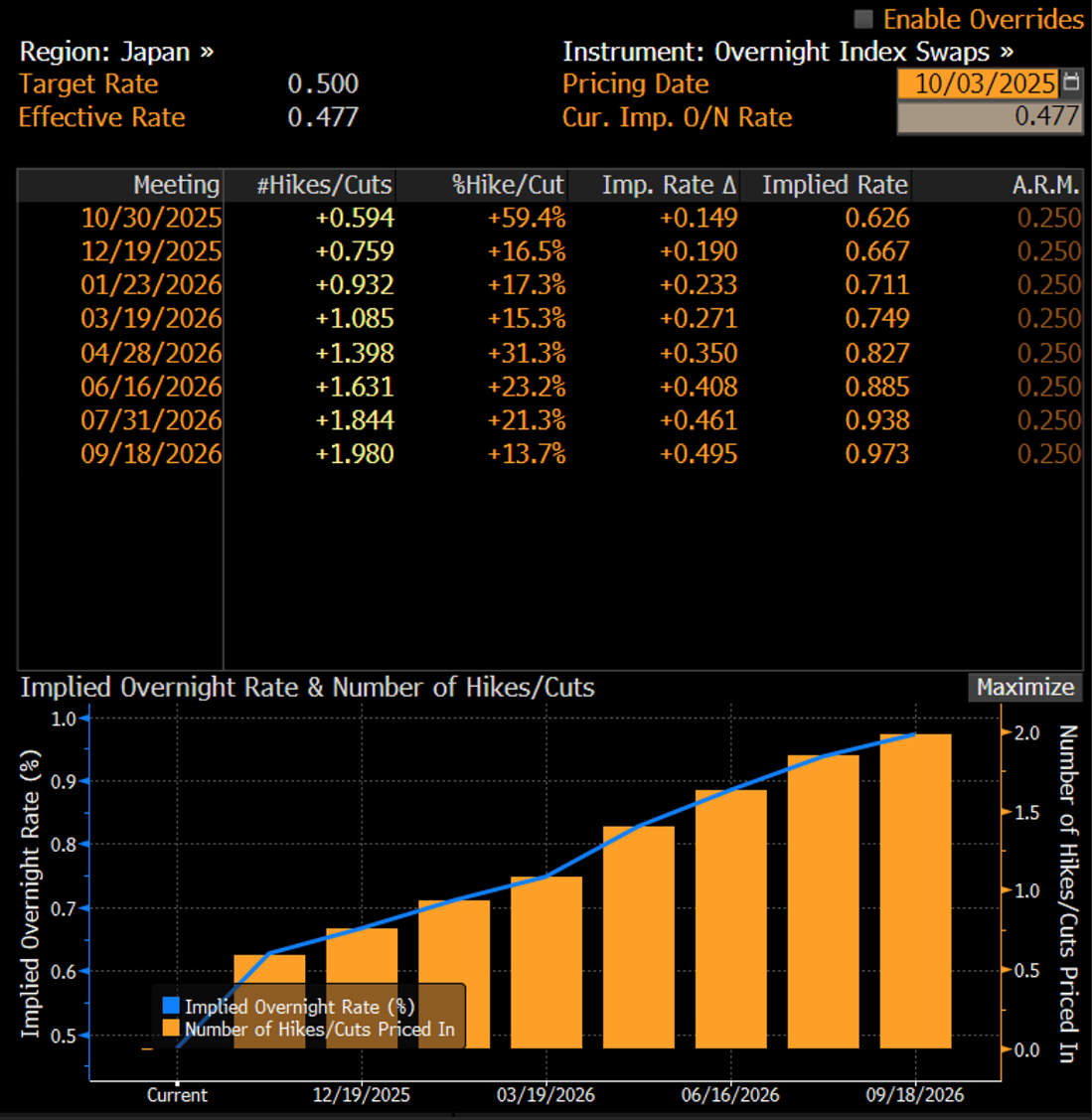

Our conviction remains unchanged from June: the BOJ is unlikely to deliver further hikes in H2 2025, even though markets are pricing ~20bps by year-end. The case for restraint has, if anything, strengthened.

The recent leadership change within the LDP leaves the political backdrop fluid. In this environment, the BOJ has strong incentives to avoid adding uncertainty. “Inaction as stability” is the best course for Ueda, particularly as the new administration seeks to consolidate its footing. A policy surprise now risks amplifying volatility across both FX and JGB markets at a time when the political establishment cannot afford fresh instability. BOJ Governor Ueda has consistently shown a preference for caution. Even in recent MPM meetings, he declined to hint at any imminent tightening, reinforcing his reputation as one of the most conservative central bankers among the majors. His guiding principle remains patience: waiting for clearer data confirmation before moving, rather than reacting to transitory signals. This approach has disappointed markets but is consistent with his pattern since taking office.

Additionally, the impact of US tariffs is beginning to filter through. Corporate profit margins, particularly in the export-heavy manufacturing sectors, are already under strain. Adding higher borrowing costs into this environment would amplify downside risks. At a time when Japanese corporates are being squeezed externally, a rate hike would appear less like policy normalization and more like policy miscalculation.

Perhaps the most compelling reason for restraint is found in the bond market. Long-dated JGB yields have already surged in recent months, reflecting both sticky inflation and global duration repricing. Further hikes from the BOJ would accelerate this rise, tightening corporate financing conditions and curbing loan demand. For an economy that has only recently managed to escape deflationary gravity, such a cooling of credit transmission is a dangerous risk.

In short, the BOJ continues to operate behind the curve, but deliberately so. Ueda’s calculus is that sustaining inflation momentum matters more than aligning with market expectations. In a fragile political environment, with tariffs biting and the JGB curve already steepening, restraint is not only the path of least resistance but also the policy most consistent with preserving stability. We do not see any hike within the year.

JPY Strategies

At present, the yen trades firmly within what can be described as the government and BOJ’s “comfort zone.” A further depreciation beyond current levels risks stoking public discontent, while an excessive appreciation would undermine the hard-won progress in escaping deflation. Against this backdrop, we see the 140–150 range as a pragmatic equilibrium, both politically and economically. In practice, a tactical strategy of buying near 150 and selling near 140 has already delivered strong results in our execution.

For more advanced strategies, selling USDJPY volatility also looks compelling. Our conviction is that, with the yen anchored inside this comfort band, price swings are unlikely to resemble the extreme volatility of recent years. A combined approach — incorporating delta, gamma, and vega exposure around the 140–150 range — offers an attractive risk-reward profile, allowing investors to monetize range-bound dynamics while maintaining optionality.

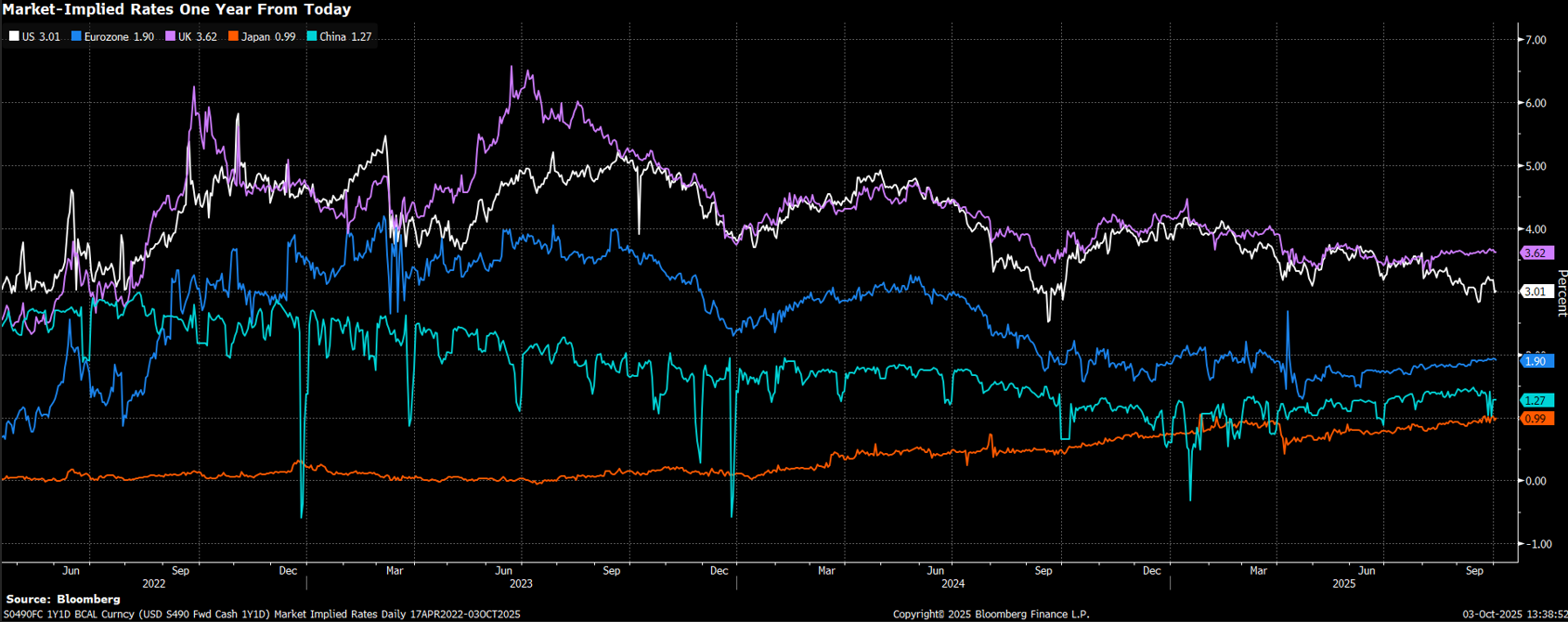

From a structural perspective, we continue to see the yen on a long-term appreciation path, supported by fundamentals. However, in the near term — particularly through Q4 — we lean toward a weaker bias. BOJ Governor Ueda remains cautious and conservative, showing little appetite to hike further despite market pricing of ~20bps. Should Ueda once again disappoint yen bulls in October, a retreat toward 150 appears highly likely.

At the same time, markets are overly optimistic about the pace of Fed cuts (see our US Outlook last week). If the Fed delivers fewer or slower cuts than priced, dollar strength could reassert itself. In such a scenario — stronger USD, weaker JPY — Q4 may offer a timely opportunity to buy JPY on dips, building medium-term long exposure at more attractive entry points.

China Summary

Both the Hang Seng and Hang Seng Tech indices have refreshed four-year highs, with the HSI breaking above 27,000 on October 2. Meanwhile, onshore equities also saw the SSE Composite index reach a five-year high. From a global perspective, China’s equity market performance this year has moved largely in line with other non-US markets, suggesting a common underlying driver: elevated expectations for aggressive Fed rate cuts, sustained USD depreciation, and a weaker US growth outlook.

However, we believe that the market has become overly optimistic about the scale of Fed easing and the extent of USD weakness. Current market pricing assumes an almost linear path of rate cuts and dollar depreciation, leaving little room for negative surprises. If expectations reverse—whether due to stickier US inflation, firmer growth data, or a slower-than-anticipated pace of Fed easing—the resulting adjustment could exert meaningful valuation pressure on Chinese equities, particularly in offshore markets where foreign flows remain the dominant force.

Macro Weakness

In the first half of 2025, China delivered 5.3% real GDP growth. Yet beneath the headline figure, disinflationary pressures remained evident. Aggregate revenue growth across all listed Chinese companies (A-shares, H-shares, and ADRs) was essentially flat, while net profit growth was just 4%. The slowdown became more pronounced in Q2: overall corporate earnings growth decelerated to 2%, with A-share non-financials posting negative earnings growth of –2.1%, and the CSI 1000 Index suffering an 11% earnings contraction. Looking ahead to the second half, in the absence of a fresh round of large-scale stimulus, economic growth is likely to slow materially, placing further pressure on corporate profitability.

From a year-on-year perspective, both CPI and PPI have stayed in negative territory for much of 2025. High-frequency data from July and August point to a clear loss of momentum relative to H1, most notably: fading fiscal impulse, a sharp slowdown in infrastructure investment, and weaker sales of autos and home appliances. On the external front, exports to the US fell by 33% due to tariff effects and the fading of front-loaded shipments. However, offsetting this drag, exports to other regions have shown resilience, supported by weak domestic demand and a sharp depreciation in the RMB’s real effective exchange rate.

On the price front, although the central government launched an “anti-involution” campaign in July aimed at curbing excessive competition, the absence of complementary demand-side measures meant that upstream price gains failed to pass through downstream. As a result, the positive impact on PPI was both temporary and marginal, while CPI continued to underperform seasonal norms.

Equity Bubble

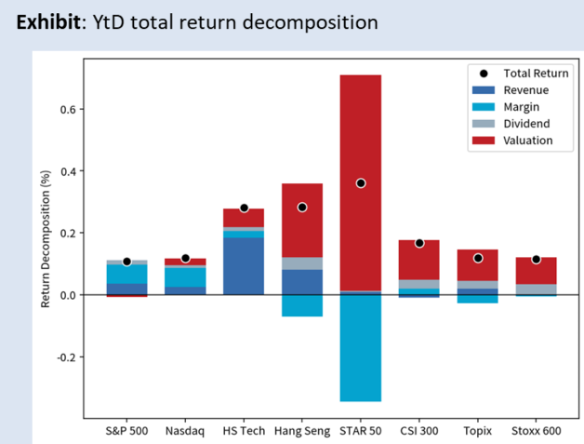

In sharp contrast to the sluggish macro backdrop and muted corporate earnings, China’s equity markets have staged a powerful rally. Year-to-date, the MSCI China Index has gained over 30%, broadly in line with the strength seen across other global equity markets. However, it is important to note that this surge has been almost entirely driven by valuation expansion. The current A-share PE (TTM) stands at 22.3x—near the 92nd percentile of the past 15 years—suggesting valuations are already close to historical extremes. Without a corresponding earnings recovery, further multiple expansion risks creating financial instability. The chart below illustrates why, despite stretched valuations, we continue to prefer US equities, and underscores our cautious stance on China at this stage.

Implicit in this sharp re-rating is a highly optimistic earnings outlook. For 2026, consensus expects MSCI China earnings growth of 16%—a pace surpassed only in 2017 and 2021 over the past decade. From a macro perspective, achieving this trajectory would require China to return to mild inflation and significantly narrow its output gap. Given today’s economic conditions, such assumptions appear overly ambitious.

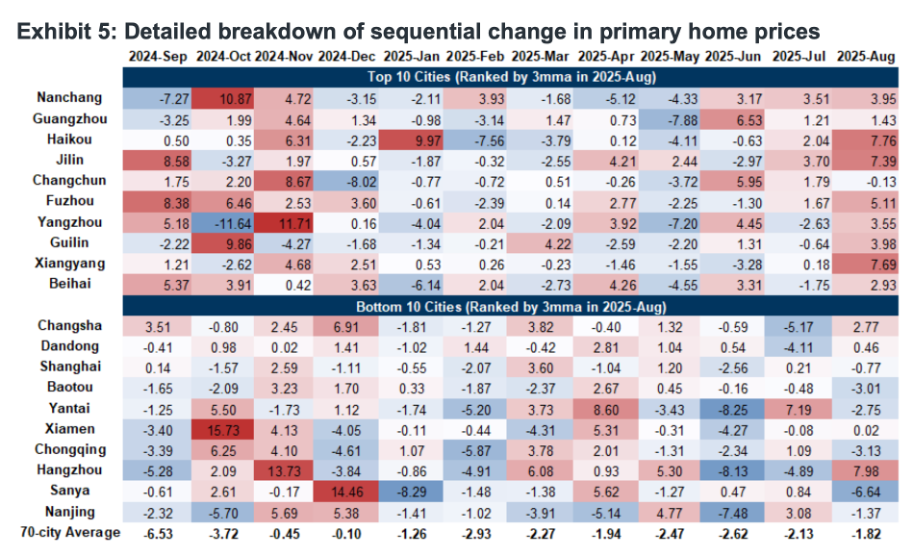

Policymakers have to some extent embraced equities as part of China’s “soft budget constraint,” seeking to boost household wealth and confidence through rising asset prices. Yet equities play only a marginal role compared with real estate, where household exposure is roughly ten times larger. With secondary home prices already down about 5% nationwide this year, the positive wealth effect from equities is insufficient to offset the drag from housing. Meanwhile, ROE for listed companies has trended lower since 2018, with weak or negative earnings growth leaving major indices stuck in long-term trading ranges. History suggests that when equity prices diverge too far from earnings fundamentals, the eventual outcome tends to be wealth redistribution and wider income inequality—undermining, rather than supporting, policy objectives around confidence and consumption.

Looking ahead, in the absence of a clear earnings recovery, liquidity and sentiment will remain the dominant drivers of Chinese equities. Investors are pinning hopes on continued monetary easing and ample liquidity to sustain valuations. The argument rests on two points: first, household savings rates have risen significantly since the pandemic; second, a large volume of time deposits will mature in 2025. Combined with falling deposit rates and the relative appeal of equities, this may encourage rotation into risk assets. Indeed, July–August flows show signs of funds moving from deposits to equities and non-bank financial institutions. Still, we view this as more a byproduct of prior market gains than a fundamental catalyst. With real rates elevated, property prices under pressure, and corporate earnings still weak, a liquidity-driven rally alone is unlikely to prove durable.