Europe and Japan's Defense Ramp Same thesis, different stage

On March 2, as news broke of Iranian strikes on commercial vessels in the Strait of Hormuz, something unusual happened in financial markets. Almost everything sold off. Oil spiked. Equities dropped. Bond yields jumped.

Since the conflict began, defense has been one of the few sectors holding its ground as broader markets sold off — the sector's resilience in a volatile tape is itself the signal.

It would be easy to read that as a reflex — geopolitical shock triggers a defense trade, prices spike, then fade when the headlines move on. That has been the pattern for much of the past decade.

But we think something more structural is happening. And it starts with a simple observation: the world outside the United States has spent the past three years quietly committing to defense budgets that will take a decade to fully spend.

The money is committed. The factories are still catching up.

In our February article, we argued that US defense had transitioned from an event trade to something closer to infrastructure — long contracts, sticky budgets, predictable cash flows. That same logic is now playing out in Europe and Japan. But the two stories are at very different points in that journey, and understanding the difference matters more than simply buying the sector.

The Simple Frame

Think of it this way. Europe and Japan are both rearming, but for different reasons, at different speeds, and with very different industrial starting points.

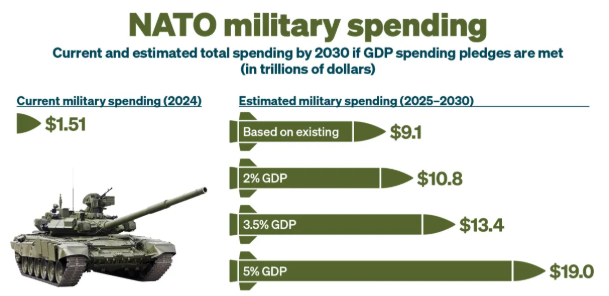

Europe is catching up from three decades of underinvestment. After the Cold War ended, most European governments spent the 1990s and 2000s steadily cutting defense budgets. The implicit assumption was that the US would provide the security umbrella and that major conflict on European soil was a thing of the past. Russia/Ukraine conflict in 2022 shattered that assumption. Germany reversed its constitutional debt brake — a fiscal rule that had been in place for over a decade — and unlocked hundreds of billions in new spending. NATO raised its target from 2% to 3.5% of GDP for core defense. The money is now committed. The challenge is that European defense industry, after thirty years of shrinking, does not yet have the factories, the workforce, or the supply chains to deliver on it quickly.

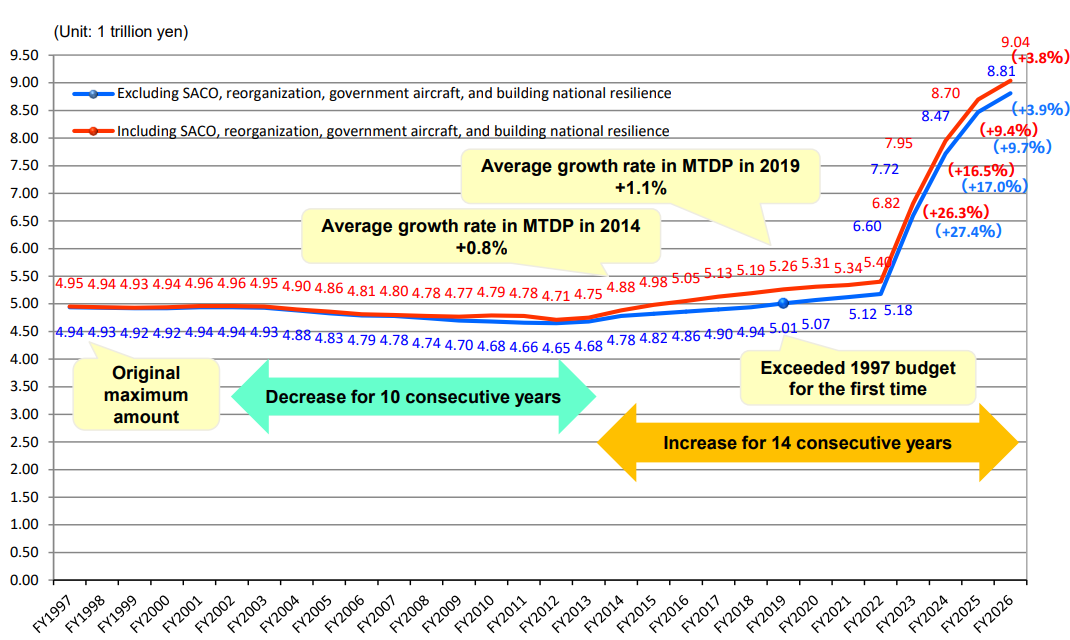

Japan is doing something it has never done before in the post-war era: becoming a defense exporter. Japan's pacifist constitution and decades of cultural resistance to military spending meant its defense industry was always domestic, always limited, and largely invisible to global investors. That is changing fast. Defense budgets have risen for fourteen consecutive years. Japan is on track to become the world's one of largest defense spenders. And in August 2025, Australia selected Mitsubishi Heavy Industries to build its next generation of frigates — a contract that would have been almost unimaginable a decade ago. Japan's defense companies are crossing from domestic suppliers into global exporters, and the market is only beginning to price that transition.

Same broad theme — rearmament as a structural, multi-year trend. Two very different investment stories.

Europe: Big Promises, Harder Delivery

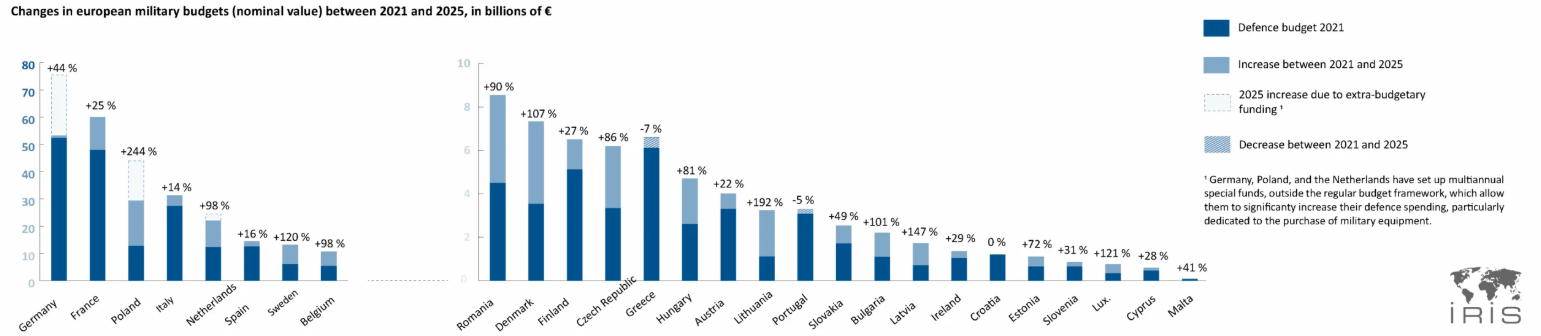

The numbers in European defense are genuinely impressive. The six largest European defense contractors — Rheinmetall, BAE Systems, Leonardo, Thales, Hensoldt, and Saab — grew their combined revenues by an average of 57% between 2021 and 2025. Order intake across those same companies grew by 135% on average over the same period. Rheinmetall alone is guiding for revenue growth of 40-45% in 2026.

When budgets are rising and backlogs are building, that kind of top-line growth is exactly what you would expect.

But here is what is less discussed: delivering on that growth is harder than booking it. Rheinmetall, Europe's most talked-about defense name, missed its own sales targets in 2025 — revenues came in 8% below expectations, and operating profit fell short of guidance. The reason was not a shortage of orders. It was a shortage of capacity. Factories cannot be doubled overnight. Skilled workers in precision manufacturing take years to train. Supply chains for specialized components are long and fragile.

This is not a reason to avoid the sector. It is a reason to understand what you are buying.

European defense is not a trade on what governments are spending today. It is a trade on what industry can produce over the next five years.

The budget commitments are real and locked in — German fiscal rules, NATO targets, and the political reality that no mainstream European government can afford to be seen cutting defense right now all point the same direction. The question is how quickly industrial output can catch up to the spending. That gap is where the earnings growth lives — and where the execution risk lives too.

Quick overview: European defense

Revenue growth: revenues across major European primes have roughly doubled on average since 2021, with order intake growing even faster — today's orders are tomorrow's revenues.

Spending floor: NATO's 3.5% GDP defense target and Germany's debt brake reversal lock in a multi-year budget commitment that is politically difficult to reverse.

The binding constraint: factories and workforce, not budgets. Industrial capacity is what limits how quickly the spending becomes earnings.

The risk: Rheinmetall, Europe's flagship defense name, missed its own 2025 sales targets. The thesis is intact — but execution is the variable to watch.

Japan: The Quieter, Less Crowded Story

If Europe is the loud story — big numbers, prominent names, constant headlines — Japan is the one that sophisticated investors are quietly gravitating toward.

The reason is simple: Japan's defense rearmament is earlier in its cycle, less owned by global investors, and has a specific catalyst that Europe does not — the emergence of Japanese companies as serious defense exporters for the first time in the post-war era.

The Australia frigate contract is the clearest single illustration of what is changing. Mitsubishi Heavy Industries was selected to upgrade Australia's fleet of frigates — a multi-billion dollar program, a decade-long relationship, and a template for what could follow with other Indo-Pacific partners seeking high-quality, technologically advanced defense equipment from a trusted ally. Japan revised its export rules in 2025 specifically to enable this kind of international program. The Spring 2026 reform — the formal abolition of restrictions on defense equipment transfers — opens the door wider still.

Mitsubishi Heavy Industries is the flagship name. It is not simply a defense company — it is also one of Japan's leading energy infrastructure businesses, giving it a dual engine of defense and energy that provides earnings resilience across cycles. The valuation is not cheap in absolute terms, but it looks justified when compared to global peers operating with a similar mix of long-cycle defense programs and energy infrastructure. The more interesting detail is that market estimates on MHI's earnings are still materially below what the fundamentals suggest — meaning the re-rating has not fully happened yet.

Kawasaki Heavy Industries tells a slightly different story, and in some ways a more interesting one for patient investors. Defense represents over 30% of its business profits, but management deliberately refuses to frame the company as a defense business. Instead, it positions itself around a broader mission: solving security and social challenges through aerospace, robotics, energy, and defense as an integrated platform. That framing matters because it insulates the investment case from the political sensitivities that still surround Japanese rearmament, and because it means the company is building capabilities — in missile engines, in naval propulsion, in high-specification aircraft — where it will hold 100% domestic market share in Japan and growing export opportunities internationally.

Defense margins at KHI are improving steadily: currently running at around 8%, expected to cross 9% from next fiscal year as a new generation of higher-value contracts comes to dominate the order book. The Australia gas turbine win — where KHI supplies propulsion systems for the frigates that MHI is building — means the two companies are often working the same programs from different angles.

Japan's defense industry is crossing from domestic supplier to global exporter. The market is only beginning to price that transition.

What makes Japan particularly compelling right now is the catalyst calendar over the next twelve months. Defense export reform completing in Spring 2026. The Australia frigate contract formally signed. A new Defense White Paper in July. A revision of Japan's three core national security documents by late 2026. Each of these is a potential re-rating moment — not because the spending suddenly increases, but because the policy architecture that enables Japan to act as a genuine defense partner to allied nations continues to be built out. Sophisticated global investors are viewing the recent share price volatility as an entry point rather than a warning.

Quick overview: Japan defense

Budget trajectory: 14 consecutive years of record defense spending, on track to become the world's one of the largest defense spenders.

The export shift: Australia's selection of MHI for its next frigate fleet is the first major signal that Japan has crossed from domestic supplier to global exporter.

MHI: defense and energy as a dual engine — the earnings trajectory is still underpriced by the market.

KHI: defense margins improving steadily, missile engine business holds 100% domestic market share, management targets 10% company-wide margin by FY3/31.

Catalyst calendar: export reform (Spring), Australia contract signing (Spring), Defense White Paper (July), Security Document revision (late 2026) — multiple re-rating moments ahead.

Poseidon's View: Japan First, Europe Selectively

The global defense rearmament theme is real, it is structural, and it is not going away regardless of what happens in the Middle East over the coming weeks. The Iran conflict is an accelerant — not the thesis. The thesis was in place before February 28 and will remain in place after a ceasefire.

Within that theme, our view is straightforward.

Japan is the preferred expression. It is earlier in its cycle than Europe or the US. It is less owned by global institutional investors. It has a specific, time-bounded catalyst in the form of defense export liberalisation that creates multiple opportunities for re-rating over the next twelve months. And the companies themselves — MHI and KHI above all — have earnings trajectories that the market is still underestimating. The valuation, while not cheap in absolute terms, is justified relative to global peers doing structurally similar things.

Europe is real but requires selectivity. The broad European defense story is well-understood and widely owned — the most prominent names have priced in a great deal of the good news. That does not mean the theme is exhausted, but it does mean the easy money has been made. If picking individual names, the best risk-reward sits in the ammunition and electronic solutions businesses — where demand is most structural and margins are improving most reliably — rather than in vehicle systems, where execution has been the weakest link.

The US names remain the anchor. As we wrote in February, US defense is the most mature expression of this theme — reliable cash flows, deep backlogs, proven management teams. For clients already holding US defense exposure, Europe and Japan are the natural extensions, not replacements.

What Could Go Wrong

Three risks are worth naming clearly.

A Ukraine ceasefire would test European conviction. Much of the political urgency behind European rearmament is driven by the ongoing war in Ukraine. A negotiated ceasefire — while genuinely positive for Europe as a whole — would temporarily reduce the sense of immediate threat that has given defense spending its political momentum. Budget commitments would remain, but the pace of acceleration could slow, and markets would likely re-price some of the geopolitical premium out of European defense names. Japan's thesis is more insulated from this scenario, as its primary driver is Indo-Pacific deterrence rather than European security.

Execution remains the critical variable in Europe. The gap between order intake and delivery is where investors get burned. Rheinmetall's 2025 miss was a reminder that even the best-positioned companies in a strong cycle can disappoint when industrial scaling is the bottleneck. The companies that manage their supply chains and workforce expansion most effectively will be the ones that close the gap between backlog and earnings; the ones that struggle will find that patience is tested more quickly at these valuation levels.

Yen strength is Japan's double-edged sword. A meaningful appreciation of the yen — which becomes more likely as the Bank of Japan gradually normalises rates — would mechanically reduce the yen value of overseas contracts and weigh on the share prices of Japanese exporters including defense names. This is a known and manageable risk, but it is real. Investors with a view on USD/JPY should factor it into their position sizing.

The defense supercycle is not a US story. It never was.

It is a story about governments around the world recalibrating how much security costs in a world that has become less predictable. Europe and Japan are both early in that recalibration — Europe rebuilding industrial capacity it spent thirty years running down, Japan building an export industry it spent seventy years avoiding.

The Iran conflict reminded markets of that this month. But the reminder will outlast the conflict itself.