AI - Bubbles, Dreams or Reality?

Introduction: From Technological Revolution to Investment Anxiety

The explosive ascent of artificial intelligence (AI) over the past three years has brought back vivid memories of the dramatic turbulence of the internet boom twenty-five years ago. From the sudden arrival of ChatGPT and the exponential advancement of large model capabilities, to the increasingly heated competition for computing power among tech giants, AI is no longer a niche topic discussed only within technology circles. It has instead become a central focus of the global economy, industrial transformation, and capital markets.

But the higher the attention rises, the more doubts inevitably surface. Over the past year, questions have emerged repeatedly: “Is AI a bubble?”, “Is this starting to look like 1999 again?”, “Is it still safe to buy tech stocks?” These concerns reflect investors’ ambivalence: they are impressed by the speed of technological progress, yet fearful that history might repeat itself.

To answer whether AI is indeed a bubble, we must return to fundamentals. Is demand real? Are investments sustainable? Are valuations divorced from earnings? Is the current expansion built on leverage? In other words, the AI revolution must be understood through structural data rather than market sentiment.

I. Why This AI Boom Is Fundamentally Different from Previous Tech Frenzies

We observe a key distinction: the current surge is driven by genuine profits and genuine demand—not by speculative narratives or dreams of distant monetization.

During the dot-com bubble more than two decades ago, the rally was fueled largely by imagination—companies with no revenue, no users, and no clear business models could still reach public markets by telling a compelling story. Today’s leaders in AI—whether they build GPUs, train frontier models, or construct data centers—are all standing on solid cashflows and mature commercial infrastructures.

Over the past two years, the revenues of certain key companies have grown more than fourfold. Their margins have remained exceptionally high, and their cashflows are strong enough to fund capital expenditures in the hundreds of billions of dollars entirely on their own. This means the current market performance is not detaching from reality; it is the result of a genuine commercial explosion triggered by breakthroughs in model capabilities.

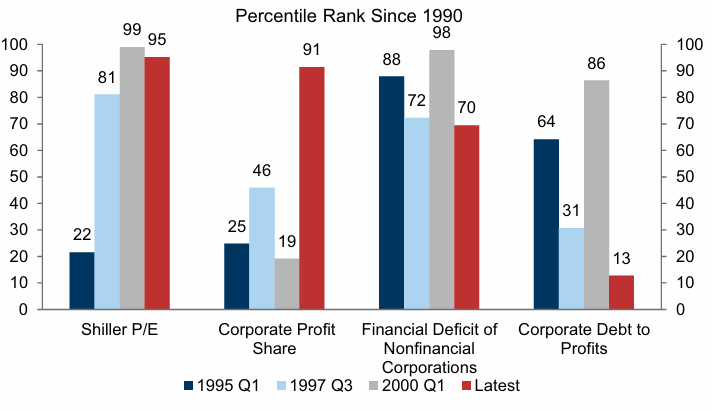

We also observe that although valuations have risen, they remain below historical extremes. Metrics such as P/E ratios, P/B ratios, and profit growth alignment show a healthier profile compared to those of 1999. When profits are truly expanding at double- or even triple-digit rates, valuation expansion becomes structurally grounded.

Equally important, this wave of AI investment has not been built on leverage. Tech giants are financing data-center buildouts and chip procurement with their internal cashflows, rather than relying on fragile external funding. The robustness of their balance sheets is one of the biggest distinctions from the dot-com era.

From a fundamental perspective, the current phase of AI development looks much more like the early acceleration stage of a technological cycle, rather than the speculative peak of one.

II. The Power of Real Demand: Computing, Data, and Productivity as Reinforcing Engines

To understand why the AI boom is not merely a speculative cycle, one must recognize a structural reality that is difficult to reverse: data volumes are growing at an unprecedented rate, and AI is the only tool capable of managing this expanding stream of information.

AI’s “explosive demand” is not something created by hype. It is rooted in three converging forces that have reshaped the digital and physical economy.

1. Exponential Data Growth: Computing Power Becomes a Global Necessity

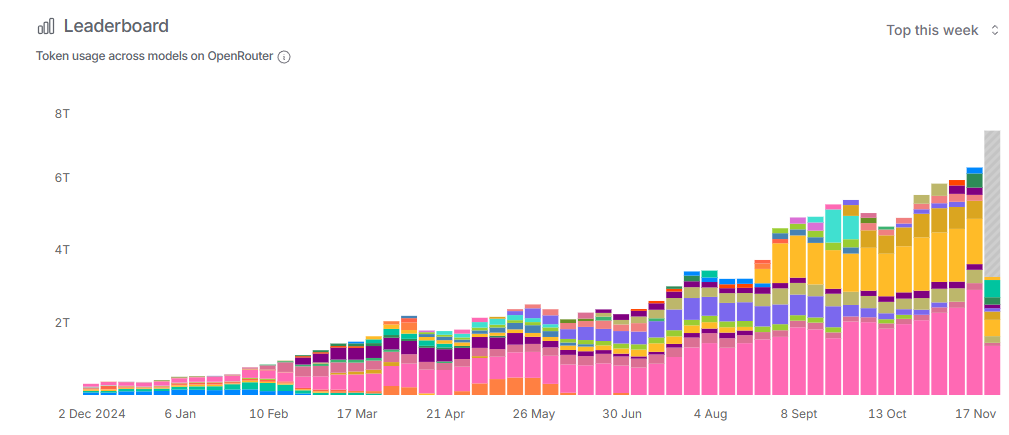

Across global AI platforms, usage has continued to climb at a breathtaking pace. Monthly token processing has grown geometrically. Large models require longer and increasingly complex training cycles. At the same time, enterprises have begun deploying AI agents to handle multi-step operational tasks, pushing inference workloads upward in both scale and complexity.

None of this is theoretical. It is behavior that takes place millions of times every day across enterprises and user environments worldwide. Data behaves exponentially, and such growth magnifies the importance of computing power. For the first time, compute is taking on the role that electricity played during the industrial revolution and the role the internet played in the information age. It is becoming foundational.

Seen in this context, the global construction of data centers and the massive procurement of AI-focused hardware is not speculative over-investment but a direct organizational response to a structural demand shock.

2. Productivity Gains Are Now Visible Across Industries

Unlike the early days of the internet—when business models were still immature and productivity benefits uncertain—AI is already demonstrating quantifiable improvements. Studies show that new employees using AI tools can raise productivity by more than 30 percent in the short term. Departments report smoother knowledge transfer, more efficient task collaboration, and meaningful reductions in time spent on repetitive work.

These improvements are not limited to a few hours saved here or there; they represent a deeper shift in human-machine collaboration. Knowledge flows more efficiently through organizations, and this efficiency compounds over time. While macro-level productivity statistics may not yet fully capture these shifts, micro-level benefits are accumulating and will eventually manifest in broader economic performance.

3. The Beginning of an Infrastructure Supercycle

The current wave of AI investment is fundamentally different from speculative booms. It resembles the early days of railway expansion, electrification, or the construction of the global telecommunications backbone. Large-scale infrastructural forces are taking shape.

AI’s infrastructure now spans massive GPU clusters, high-density data centers, power and cooling facilities, transmission networks, and cloud-based platform services. Across this ecosystem, we observe industries entering a heavy-asset, cross-border construction cycle that may last a decade or more. This is not a narrative-driven bubble; it is the early acceleration phase of a structural megatrend.

III. Why Markets Feel “Excited Yet Anxious”: The Economics Behind Investor Sentiment

1. The outsized weight of tech giants amplifies market volatility

Today, a handful of major technology companies account for an unprecedented share of major market indices. When the performance of the entire index hinges on the trajectory of only a few firms, markets naturally become hypersensitive. Even small valuation fluctuations in these giants can generate broad market swings, magnifying both optimism and anxiety. This structural concentration makes the market feel more fragile, even when fundamentals remain strong.

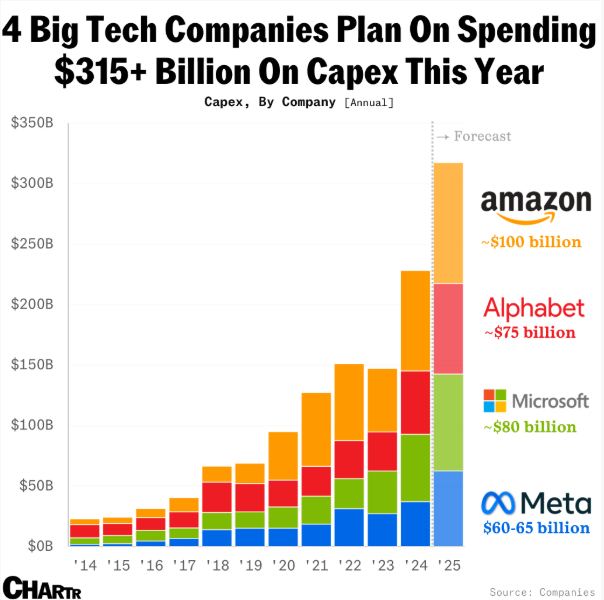

2. The extraordinary pace of capital expenditure triggers concerns about sustainability

Capital spending on data centers, AI chips, and supporting infrastructure has reached historic highs—hundreds of billions of dollars annually. Although these investments respond to legitimate demand, investors cannot help but worry about whether such expansion can remain aligned with actual usage. If demand unexpectedly slows or enterprises adopt more efficient model architectures, some of today’s newly built compute capacity may face temporary underutilization. Such worries echo memories of the early 2000s, when vast fiber-optic networks lay idle for years after the dot-com crash. These historical scars intensify present-day caution.

3. The rise of “conceptual AI companies” intensifies skepticism

As with every transformative technology cycle, AI has attracted numerous companies eager to associate themselves with the trend despite lacking substantive capabilities. Many firms now describe their strategies using the language of AI, even though their business foundations remain unchanged. Markets are keenly aware of this discrepancy. When overall enthusiasm lifts valuations rapidly, these “story-driven” companies become the first to break down, reinforcing fears that AI as a whole might be heading toward a bubble.

Yet from a structural standpoint, such firms represent noise rather than the core of the AI economy. True technological cycles always feature a mix of leaders, fast followers, and speculative outsiders. The latter do not define the trajectory of the trend—they merely accompany it.

IV. Could a Bubble Form? Key Risk Pathways Over the Next Two to Three Years

Although we do not believe AI is currently in a bubble, we acknowledge that certain dynamics warrant close observation. Technological revolutions rarely move in straight lines; they follow patterns of acceleration, overheating, correction, and reacceleration. AI now appears to be in the mid-stage of such an acceleration cycle—analogous in some respects to the late 1990s.

We see three structural variables that will determine whether bubbles may form: the pace of capital expenditure, the durability of demand, and the strength of profit conversion.

1. Rapid capital expansion risks future mismatches if demand and supply fall out of sync

The current scale of infrastructure buildout—land acquisition for data centers, unprecedented power requirements, GPU server clusters, cooling systems, fiber networks—resembles an industrial-level mobilization. This is not inherently problematic. However, if supply grows faster than demand for a sustained period, mismatches may emerge.

For example, if frontier model training becomes more efficient or enterprise applications shift toward lighter-weight architectures, part of today’s capacity may not be utilized immediately. While this is not yet a concern—enterprise adoption remains in its infancy—it is a variable that could shape the industry’s medium-term trajectory.

2. Strong demand must continue to prove itself through commercial outcomes

AI’s long-term economic value depends not on the sheer size of models but on the depth of real-world usage. If enterprises conclude within the next two to three years that AI does not materially improve efficiency, reduce costs, or generate new revenue, budget tightening will follow. Historically, every major technology shift—from automation to ERP systems—has

V. Understanding AI’s Long-Term Logic: From Tech Euphoria to Industrial Restructuring

1. AI is no longer “a tech sector story” but a foundational capability for every industry

When we strip away short-term price movements and examine AI as an industrial phenomenon, we see a deeper, structural transformation. AI is becoming the foundational layer across energy, finance, healthcare, manufacturing, transportation, retail, creative industries, and government services. Its influence already exceeds that of many past innovations.

This transition extends beyond the digital world. As highlighted in the energy analysis you provided, surging data-center demand is reshaping the physical energy grid in the United States. Regions face power shortages; utilities and regulators are reevaluating generation and transmission plans. This “spillover from virtual to physical infrastructure” signals that AI is driving a genuine reordering of economic systems.

2. The structural mismatch between exponential demand and linear supply will define the next decade

AI’s compute needs grow exponentially—but electricity generation, land development, server manufacturing, cooling capacity, and grid expansion grow only linearly. This mismatch creates long-term scarcity of computing resources and fuels competition among firms and nations. Future competitive advantage will derive not only from model capabilities but also from access to energy, hardware, and data—making compute itself a strategic asset.

3. The value chain is shifting from software back toward infrastructure

In the internet era, software captured the highest margins. In the AI era, however, the center of gravity is moving downward: toward compute providers, chip designers, power suppliers, data-center operators, and the cloud platforms that orchestrate these resources.

This shift implies that infrastructure players—long overlooked in past tech cycles—may hold the most durable strategic value in the years ahead. Conversely, models themselves may become more interchangeable as the ecosystem matures.

4. AI’s macroeconomic impact remains in its early stages

AI is simultaneously generating investment effects (through infrastructure spending), wealth effects (through rising tech equity valuations), and productivity effects (through workflow efficiencies). These forces operate with lag but tend to reinforce each other. Their combined impact on GDP growth will likely unfold gradually over the next five to ten years, rather than immediately.

VI. Navigating a World Where Trends and Volatility Coexist

1. Short-term volatility is noise; long-term trends are structural

AI is a highly deterministic long-term trend. It will continue to reshape industries, enhance productivity, and contribute to economic expansion. But such deterministic trends often exhibit considerable short-term volatility—especially when markets react to valuation concerns, competitive shifts, or temporary fluctuations in demand. These fluctuations reflect sentiment more than underlying structure.

2. Long-term value will come from foundational capabilities, not narrative-driven stories

In the competitive landscape ahead, the most enduring value will be held by companies with true foundational advantages: computing power, energy access, advanced chips, grid and storage infrastructure, and deeply integrated enterprise AI systems. Concept-driven companies without substantive capabilities may rise briefly during periods of excitement but seldom survive the transition into deeper phases of industry maturation.

3. Patience is essential; understanding the trend matters more than predicting its every fluctuation

AI’s evolution will have ups and downs, but its trajectory is clear. Investors who focus obsessively on short-term price movements may miss the structural transformation underway. The most meaningful long-term returns will accrue to those who distinguish signal from noise, understand the underlying drivers, and maintain conviction through cycles.