2026 Q2 Global Economic Outlook (I) — US - Before the Fog of War Clears - Between the Strait and the Ballot Box

Before the Fog of War Clears - Between the Strait and the Ballot Box

US Summary — A Quarter of Crosscurrents

In our last quarterly update, we closed with an optimistic note: 2025 had ended with sails up, the Fed was cutting, liquidity was improving, and the AI cycle appeared firmly in its buildout phase. We entered 2026 expecting alpha to separate from beta—and that the year would reward selectivity over direction. Three months later, the reality has been far messier than anyone anticipated.

The first quarter of 2026 will be remembered as one of the most disorienting periods in recent market history. What began as a continuation of late-2025’s constructive tone was upended in February when escalating tensions between the US and Iran culminated in the partial closure of the Strait of Hormuz—triggering the largest oil supply disruption since the 1970s. Brent crude surged past $100 for the first time since 2022, US gasoline prices spiked to the highest level in two years, and inflation expectations—which had been steadily anchoring lower—reversed course abruptly. The damage was not contained to energy. The oil shock propagated across every major asset class in rapid succession. Here is how it unfolded.

January: Before the Storm Arrived

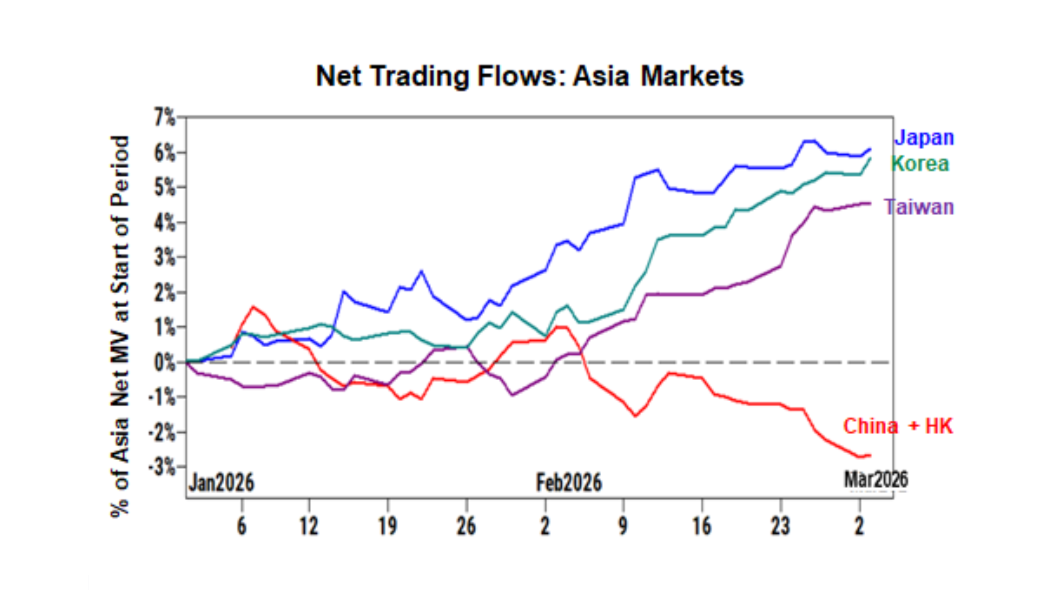

The year opened with unmistakable euphoria. Japanese and Korean equity flows were exceptional—foreign capital poured into both markets at a pace not seen in years, driven by a powerful convergence of structural narratives. In Korea, the memory trade was on fire. SanDisk’s blowout results reignited animal spirits across the semiconductor supply chain, and Korean retail investors—always a force in memory cycles—piled in aggressively. For a few weeks in January, it felt like the AI hardware buildout thesis had moved from conviction to consensus. US equities pushed to fresh all-time highs as well, carried by FOMO and a macro backdrop that still looked benign: the Fed had delivered three consecutive cuts in the back half of 2025, markets were pricing two more for 2026, and the consensus was that the easing cycle would resume by mid-year.

Then, on January 20, the political landscape shifted. Kevin Warsh was nominated to succeed Jerome Powell as Fed Chair, with Powell’s term set to expire on May 15. We had flagged Warsh in our December outlook as having stronger market credibility than Kevin Hassett, and the nomination broadly confirmed the administration’s preference for a Fed chair who would be sympathetic to its growth agenda. Markets digested the news calmly—Warsh was seen as a steady hand—but the longer-term implications, particularly his known advocacy for a smaller Fed balance sheet, quietly began to inform how institutional investors thought about term premia.

February: The Curtain Draws

The mood shifted in February. On the surface, markets were still constructive—Korean memory names continued to attract extraordinary retail flows, and the SanDisk-led momentum extended further into the supply chain. But beneath the surface, something was building.

In early February, the US began deploying additional carrier strike groups to the Persian Gulf. What had been low-grade diplomatic tension with Iran escalated visibly as naval assets moved into position. By mid-February, the Pentagon confirmed the repositioning of the USS Eisenhower and supporting fleet into the Strait of Hormuz corridor—a signal that the administration was preparing for a more direct confrontation. The market initially shrugged it off, as it has with most geopolitical posturing since 2022. Oil moved higher but not dramatically. Equities wobbled but held.

In hindsight, February was the month when everyone should have been paying closer attention. The deployment was not a bluff. The administration’s rhetoric was escalating in lockstep with the military positioning. And the market’s complacency—still fixated on memory stocks and AI flows—created the conditions for what came next.

March: The Strike, the Strait, and the Sell-Off

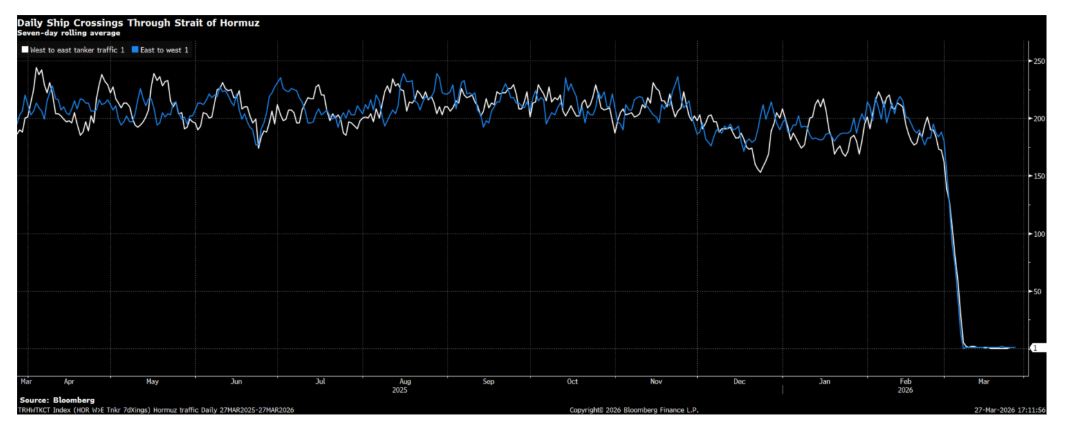

March was when it all broke. The US launched strikes against Iranian nuclear and military infrastructure starting from 28 Feb, and Iran responded with a strategy designed to inflict maximum economic pain: the partial closure of the Strait of Hormuz and coordinated attacks on Gulf state oil infrastructure. The Strait—through which roughly 20% of global oil supply transits—became the epicenter of a supply shock that markets had treated as a tail risk for decades but never seriously priced.

Brent crude surged past $100 for the first time since 2022. Iran’s attacks on Saudi and Emirati facilities disrupted not just transit but production, creating the largest supply dislocation since the 1970s oil embargo. The speed of the move caught nearly everyone off guard. Within days, the shock propagated across every major asset class: equities sold off relentlessly, the long end of the Treasury curve repriced on inflation fears, credit markets widened as hedgers rushed for protection, the dollar surged on safe-haven flows, and gold—paradoxically—suffered its worst drawdown in over forty years as forced liquidation overwhelmed fundamentals.

The March FOMC capped the quarter with a hawkish exclamation point. The Committee held, as expected, but the dot plot priced just one cut for 2026—down from three in September. OIS markets moved even further, wiping out all cuts entirely and embedding roughly 10bps of tightening. In the span of a single quarter, the market went from pricing an easing cycle to pricing a policy error.

To summarize, Q1 delivered a correlated stress event across energy, rates, equities, credit, gold, and FX—the kind of quarter that leaves most portfolios with nowhere to hide. It has been, by any measure, one of the more difficult quarters for multi-asset investors since the COVID crash.

Our view on Iran Unfolding

Yet beneath the chaos, we see the outline of a resolution — one that markets have not yet fully priced.

The central question for Q2 is not whether the current backdrop looks ugly (it does), but whether it is structurally different from the 2022 energy crisis or merely a high-severity, low-duration supply shock that the global system can absorb. We believe the latter.

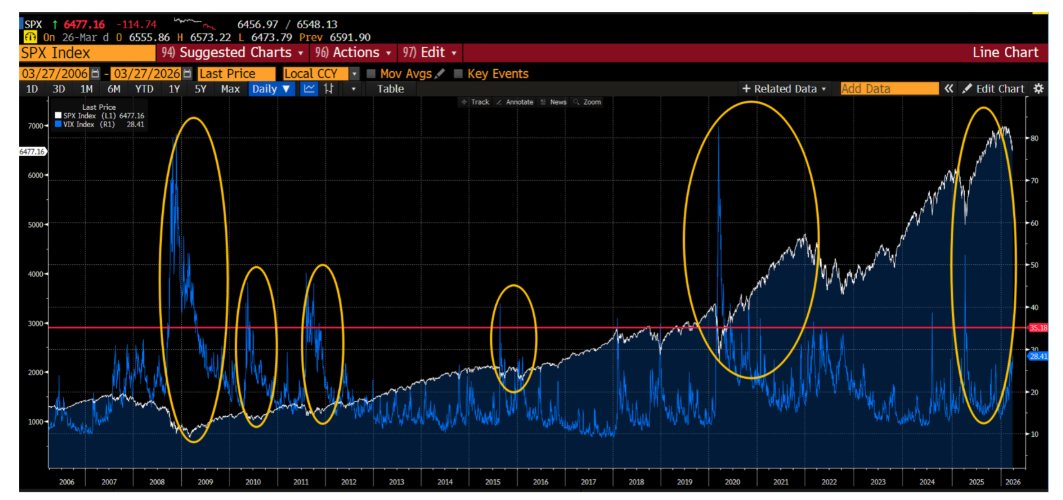

Our conviction rests on a simple political observation: President Trump cannot afford to enter the 2026 midterm cycle with $100 oil, a 5% long bond, a weak stock market, and rising inflation expectations. The Trump Administration's track record — from tariffs to trade wars to the various fiscal standoffs of 2025 — shows a consistent pattern: escalation followed by TACO once markets force his hand. We expect the same playbook to apply here. Our base case is that Iran is a one-off crisis, not a regime shift. And when the fog of war clears — with net exposure across the street already at depressed levels — the assets that have been indiscriminately sold will reprice sharply, driven by both short covering and re-leveraging History offers a useful reference: when the VIX has breached 35, it has consistently marked a strong entry point with the sole exception of the 2008 global financial crisis. We do not believe this conflict rises to that level of systemic risk.

On the other side of the table, we should give Iran credit where it is due. Tehran has played its hand more effectively than most expected. By targeting Gulf state infrastructure and production facilities directly — rather than limiting disruption to the Strait itself — Iran found Trump's pressure point: oil prices. We believe this was, in fact, beyond the white house's initial expectations. The calculus was that decapitating Iran's leadership would weaken the regime; instead, it consolidated the IRGC's grip on the state. Yet Iran faces its own constraints. Oil revenue remains critical to the regime's domestic legitimacy, and a prolonged supply disruption ultimately hurts Tehran as much as anyone. What Iran is doing, in our view, is leveraging the Strait and the oil price impact as bargaining chips — adding cards to the negotiation table in exchange for more favorable terms in any eventual agreement.

The most likely outcome, in our assessment, is an asymmetric resolution: both sides declare success, a temporary ceasefire is reached, and the immediate supply disruption fades. But we should be clear-eyed — the underlying tension does not disappear. The risk of a second escalation will linger well beyond any initial agreement, and markets will need to price a structurally higher geopolitical premium in energy for the foreseeable future. For now, however, we believe the direction of travel is toward de-escalation, and that is what matters for positioning.

In the following sections, we begin where we always do: with a candid scorecard of what we got right and wrong in December, followed by our updated views on the Fed, rates, credit, FX, gold, and equities.

Scorecard — What We Got Right and Wrong

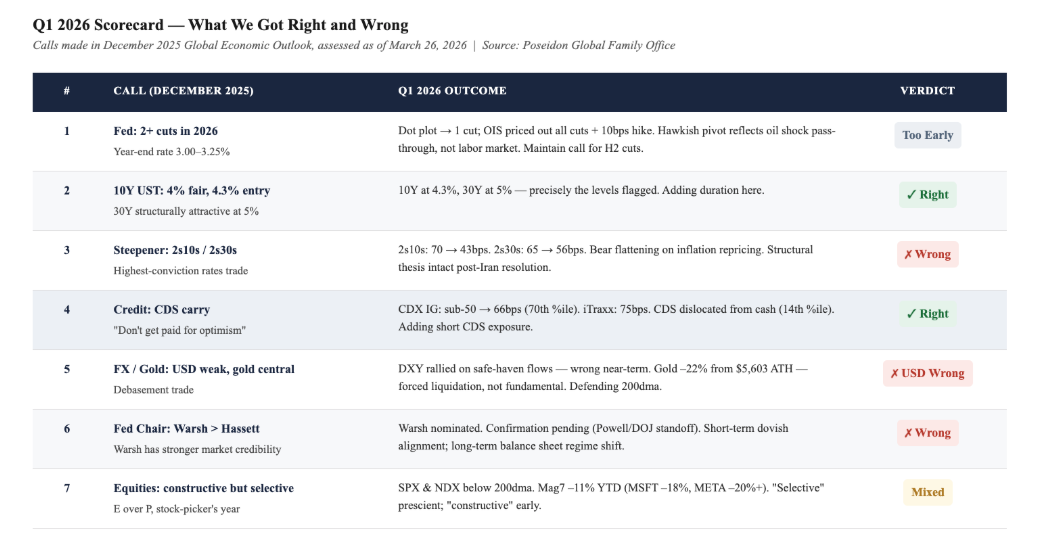

In our Q1 2026 outlook published December 22, we laid out seven core views. Three months in, the honest accounting is mixed—directionally sound on several structural calls, but caught by the magnitude and speed of the Iran shock on others. Here is the ledger:

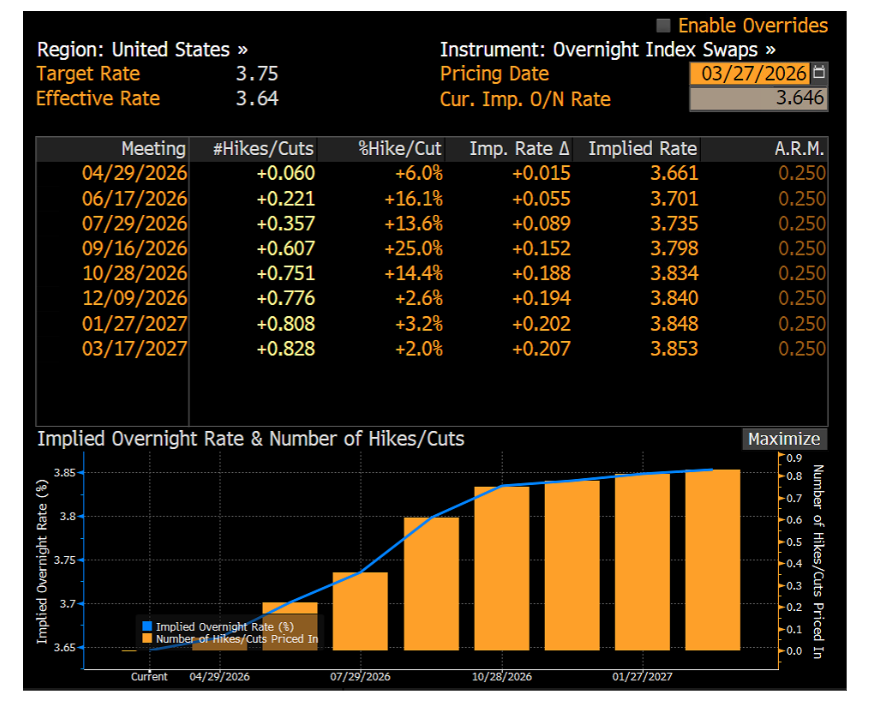

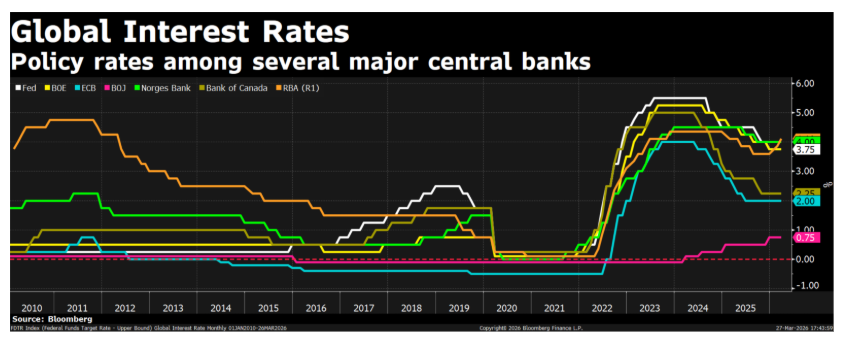

1. Fed: 2 cuts in 2026, year-end rate 3.00–3.25%. Status: Too early to score, but the backdrop has shifted. The March FOMC held as expected, with the dot plot pricing just one cut this year. OIS markets have moved further—pricing out all cuts and embedding roughly 10bps of tightening. The hawkish pivot reflects the oil shock’s pass-through into inflation expectations, not a fundamental reassessment of the labor market. We still believe two or more cuts are coming in H2 as the supply shock fades, and we note that the short end at 3.88% already reflects significant pessimism relative to a neutral rate near 3.5%.

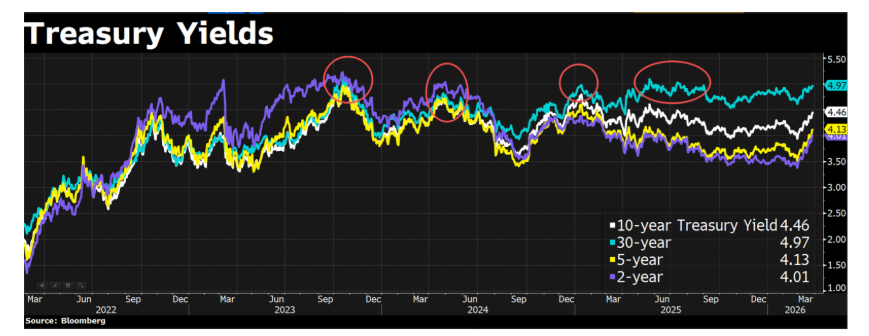

2. 10Y UST: 4% fair anchor, 4.3% attractive entry. Status: Correct on framework, now actionable. The 10Y sits at 4.3%—precisely the level we flagged as an attractive entry point in December. The 30Y has reached 5%, a level we consider extremely compelling on a structural basis. We are adding duration here.

3. Steepener (2s10s, 2s30s) as highest-conviction trade. Status: Partially wrong on direction. The 2s10s has flattened from 70bps to 43bps, driven by the long end selling off faster than the front end as inflation fears repriced term premia. However, the structural thesis remains intact: once the Iran shock passes and the Fed resumes its cutting path, the curve will re-steepen. The trade is temporarily underwater, not broken.

4. Credit: CDS indices for carry. Status: Right on instrument, now significantly more interesting. CDS IG has widened from sub-50bps to 66bps (70th percentile of the 10-year range), while iTraxx Main sits at 75bps. The critical observation is that CDS has dislocated from cash credit—investment-grade cash bonds remain at only the 14th percentile of spread, reflecting heavy issuance absorption. This technical divergence is exactly the setup we favor for adding short CDS exposure.

5. FX: USD structurally vulnerable, debasement trade, gold central. Status: Wrong on dollar direction short-term, right on gold structure. DXY has strengthened on risk-off safe-haven flows—the opposite of what our debasement thesis implied for Q1. The dollar’s rally is classic crisis behavior: when the world gets scared, capital flows into USD regardless of long-term fundamentals. We maintain that this reverses once the geopolitical shock passes. On gold, the 10% drawdown—its largest since 1983—was not in our base case. That said, the liquidation was forced risk-off selling (margin calls, position reduction), not a fundamental reassessment. Gold has been defending its 200-day moving average well this week, EM central bank buying remains structural, and we view this as a buying dip opportunity.

6. Fed Chair: Warsh stronger market cred. Status: Wrong. Kevin Warsh has been eventually nominated—the candidate we identified as having stronger market credibility. The market implications are nuanced: short-term, Warsh is likely aligned with the market’s pro-growth bias (and will lean dovish ahead of midterms). Long-term, his advocacy for a smaller Fed balance sheet represents a meaningful regime shift that could structurally alter how markets price term premia.

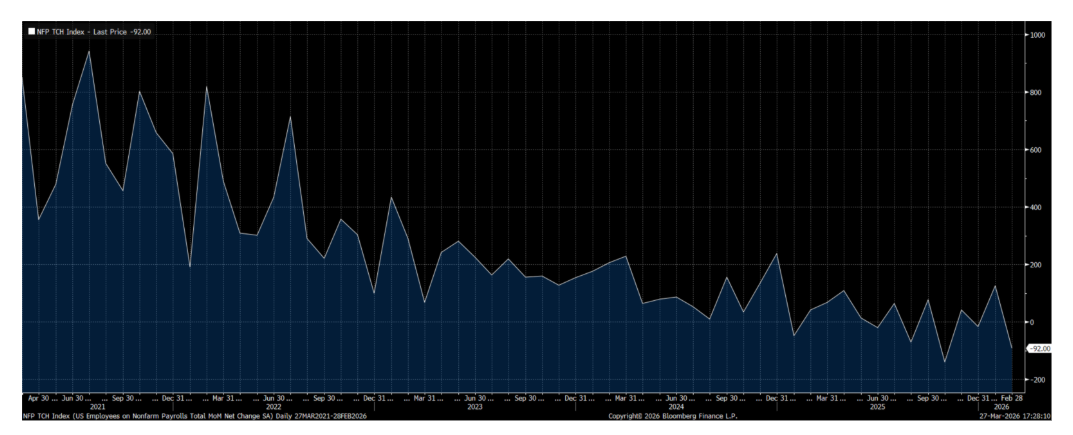

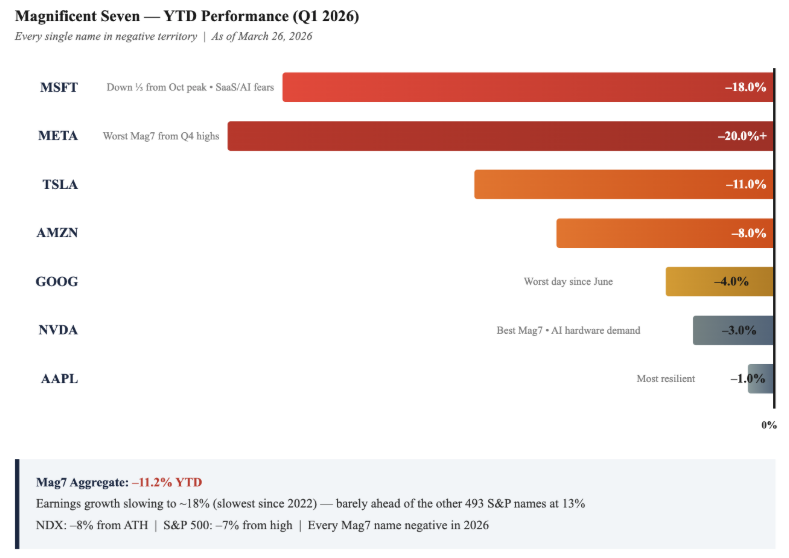

7. Equities: constructive but selective, E over P. Status: The “selective” part was prescient; the “constructive” part required patience. SPX and NDX have both broken below their 200-day moving averages. The AI narrative has not changed, but the market is now firmly in “proof” mode. We continue to believe this correction creates opportunity, not a regime change.

Fed & Liquidity — 2026 Is Not 2022

The March FOMC was exactly what it needed to be: a hold. With Brent above $100 and headline CPI expectations ticking higher on energy pass-through — though the full transmission into inflation data typically takes several months given reporting lags — the Committee had no choice but to maintain its hawkish posture. The dot plot printed one cut for 2026, and Chair Powell’s press conference was deliberately measured—acknowledging the supply shock while refusing to validate a sustained inflation narrative.

We think the market is overreacting. The current oil shock is fundamentally different from 2022 in three critical respects:

First, 2022 was a demand-pull structural inflation crisis compounded by supply disruption. Today’s shock is purely supply-side—a one-off geopolitical event, not a structural shift in global energy markets. The US shale complex is better capitalized, SPR releases are an available tool, and global inventories, while not abundant, are not depleted.

Second, the transmission mechanism is weaker. In 2022, energy costs amplified through wages, housing, and services in a tight labor market. Today, the labor market has already cooled meaningfully—unemployment at 4.6%, wage growth decelerating, bargaining power firmly back with employers. The second-round effects that turned transitory into persistent in 2022 are far less likely to repeat.

Third—and most importantly—the political cycle argues for resolution. Trump cannot enter midterms with $100 oil. His negotiating playbook is well-established: maximum pressure followed by a deal. The Hormuz situation will almost certainly de-escalate before it entrenches. When it does, the inflation premium embedded in rates will unwind rapidly.

Against this backdrop, we maintain our call for two or more cuts in H2 2026. The front end is pricing zero cuts — OIS and futures have wiped out all easing and even embedded roughly 20bps of tightening by year-end. We believe this is an overreaction driven by the war premium in energy, not a fundamental reassessment of the economy. There is alpha in fading this pessimism. Our logic is simple: Trump will take every means available to wind down the conflict, lower real rates, and bring inflation expectations back to earth before the November midterms. The midterms are not just an election — they determine whether the Republican majority holds, whether his legislative agenda survives, and ultimately whether his legacy is cemented or faces the embarrassment of impeachment proceedings in his final two years. From this perspective, the Fed's hawkish dot plot is a snapshot of today's uncertainty, not a forecast of where we will be in six months. That is why we stick to our Q4 stance despite the unexpected turn in Iran.

The Warsh Transition — More Complex Than It Appears

The Warsh nomination is the right call for markets in the long run. His historical advocacy for a smaller Fed balance sheet and rules-based policy addresses one of the market's deeper anxieties — Fed independence. In a world where the previous administration tested the boundaries of central bank autonomy, Warsh's intellectual framework provides a credible anchor. This is, in our view, a genuine regime shift: a Fed chair who is philosophically committed to a leaner balance sheet will structurally change how term premia are priced, and over time, how M2 growth evolves. The implication is that the liquidity tailwind we enjoyed in the post-COVID era — abundant reserves, aggressive balance sheet expansion, rapid M2 growth — may not return to the same degree. From a flows perspective, this matters for asset demand across the board.

However, the near-term picture is messier than the headline suggests. Warsh's Senate confirmation has not yet been scheduled — his financial disclosure paperwork has not been submitted, and Senator Tillis is blocking all Fed nominees over the headquarters renovation dispute. Meanwhile, Powell has made his own position clear: following the DOJ's criminal investigation into the Fed (which a federal judge has already called out as harassment, blocking the subpoenas), Powell has stated he has "no intention of leaving the board until the investigation is well and truly over, with transparency and finality." If Warsh is not confirmed before Powell's term expires on May 15, Powell will remain as chair pro tempore — creating a limbo that markets have not yet fully priced.

In practice, we believe the transition happens — but not smoothly. The political incentive is clear: the Lauder–Trump relationship (Warsh's father-in-law Ronald Lauder has been close to Trump since their Wharton days) ensures continued White House commitment to the nomination. And we suspect there is an implicit alignment between Warsh and the administration on near-term priorities: deliver one or two rate cuts before November to ease financial conditions heading into the midterms, in exchange for the seat. The hawkish balance-sheet framework is a long-term project; the immediate priority is political survival.

Rates — Add Duration, Steepener Still Works

The rates market is now offering the best entry point since the start of this cycle. The 10Y UST at 4.3% was the level we identified in December as “increasingly attractive,” and the 30Y at 5% offers what we consider to be one of the most compelling risk-reward setups in fixed income. We are adding duration here.

Our framework has not changed: 4% remains our fair-value anchor for the 10Y, reflecting the structural forces we have discussed at length—the end of the pre-COVID rate regime, persistent fiscal expansion, and a higher terminal rate floor. What has changed is that the Iran shock has pushed yields meaningfully above fair value, creating a window to add.

On the steepener, we acknowledge the temporary pain. The 2s10s has compressed from 70bps to 43bps, and the 2s30s from roughly 65bps to 56bps. The flattening reflects the long end’s sensitivity to inflation fears—the 30Y repriced aggressively as the market extrapolated oil pass-through into duration. But the front end has not rallied as we expected, because the market is pricing the Fed as stuck.

We believe this is temporary. Once the Iran situation de-escalates and oil normalizes, the front end has room to rally—the 2Y at 3.88% is roughly 30bps above where it should trade if the neutral rate is 3.5% and one to two cuts are forthcoming. Meanwhile, the structural forces keeping the long end elevated (fiscal supply, term premia, Warsh’s balance-sheet views) remain in place. The steepener is temporarily offside, but the fundamental drivers are intact. We are maintaining the position.

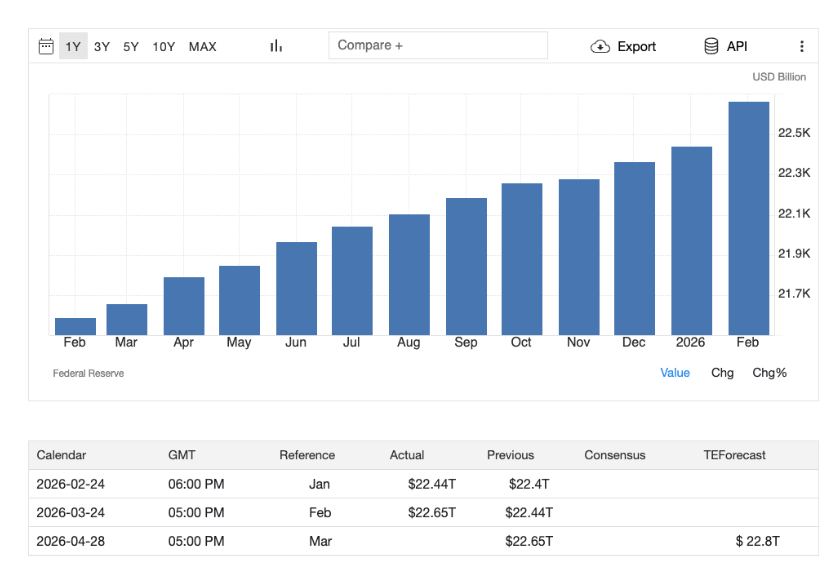

The liquidity framework we outlined in December — RMP (Reserve Management Purchases) and the eSLR recalibration — is no longer a forecast; it is now visible in the data. US M2 money supply reached a record $22.67 trillion in February, growing at 4.9% year-over-year — the 22nd consecutive month of expansion, and now exceeding the previous all-time high set in March 2022. The Fed's RMP program, launched in December, is running at approximately $40 billion per month in Treasury bill purchases, with the pace expected to remain elevated through April to accommodate seasonal reserve drains. The eSLR recalibration officially took effect April 1, freeing up an estimated $219 billion in Tier 1 capital requirements for major bank subsidiaries — capital that can now be deployed to intermediate Treasuries and repo. While the market's attention has been consumed by Iran and the FOMC, the plumbing is quietly and materially improving. This is bullish for risk appetite once the geopolitical fog lifts.

Credit — CDS Dislocation Creates Opportunity

Credit markets have given us exactly the setup we wanted. In December, we argued that CDS indices were the cleanest expression of carry in a late-cycle environment — that you "don't get paid for optimism" when spreads are sitting at multi-year tights. Three months later, the discipline to stay cautious has been validated, and the risk-off move has widened CDS spreads to levels that are genuinely interesting — and, crucially, created a technical dislocation between CDS and cash credit that we intend to exploit.

CDX IG has widened from sub-50bps to 66bps; iTraxx Main opened the week around 75bps. Both are above the 70th percentile of their 10-year range — the widest since Liberation Day, and outside of that tariff spike, the widest since 2023. Friday March 20 marked the semi-annual roll (iTraxx S45, CDX IG S46), with modest credit quality deterioration: Paramount exited CDX IG, Suedzucker and Stellantis fell out of iTraxx Main. New series traded 4.5–4.8bps wider on the maturity extension.

The dislocation that matters most is CDS versus cash. Global IG cash spreads sit at just the 14th percentile; HY at the 22nd. CDS has widened on hedging demand — it is the natural short instrument since cash bonds are hard to borrow — while cash has been insulated by all-in-yield buyers. Private credit headlines have added a further layer of protection buying, particularly in software and capex-sensitive names. In prior sell-offs, CDS widens first on hedging, then cash catches up once mutual fund outflows hit. We may now be entering that second phase.

We are adding short CDS exposure, with a clear preference for CDX over iTraxx. The US is a net energy exporter and less exposed to oil pass-through than Europe. CDX IG has only one software name out of 125, so index-level widening driven by private credit and SaaS fears looks overstated.

The market is pricing the worst-case path: oil spike, reflation, recession, DM hikes. We disagree. Unlike 2022, this is one commodity complex — no broad fiscal stimulus, no supply-chain collapse, no post-COVID labor dislocation. The Fed is more likely to delay cuts than to hike. If that proves right, the repricing from "hike fear" to "cut cycle" compresses spreads. That is the asymmetry.Iran's leverage via Hormuz should diminish over time as workarounds emerge — UAE/Saudi pipeline capacity, Red Sea rerouting, SPR releases. The marginal cost of maintaining the blockade rises for Tehran while the impact on the West gradually fades.

Over our 53-month live track, entering at 70–80bps has produced 17–18% net one-year returns in USD. If we are wrong on the macro, rate impact on the portfolio is contained as CDS duration is almost neutral. At these levels, carry plus roll should absorb Iran-related volatility — provided we maintain strict downside controls and conservative leverage. The risk-reward is compelling.

FX — Crisis Premium, Not Regime Change

The dollar has rallied in Q1 — and we got that wrong in the near term. But the nature of this move is important to understand, because it tells us something about what comes next.

The key difference between Liberation Day and the Iran shock is positioning. Last April, when Trump pushed tariffs, the market was already short USD — the pain trade was dollar strength, and it squeezed. Today, the dynamic has flipped: in a genuine geopolitical crisis, capital is flowing into the dollar, not out of it. With DXY around 100, the US has a clear relative advantage against the other major reserve currencies. Against EUR and JPY in particular, the US is more resilient because it is a net energy exporter, while Europe and Japan remain heavily dependent on imported energy. That relative advantage is also visible in equity market performance — US indices have held up better on a relative basis precisely because the energy shock hits DM importers harder.

However — and this is the nuance the market is missing — because the US is better positioned to contain inflation from this shock, the Fed is still the only major central bank that could plausibly remain on a cutting path over the next year. The BOE, ECB, BOJ, and RBA all face greater risks of having to lean hawkish again as imported energy costs feed into their inflation prints. Once Iran is resolved and the oil premium fades, rate differentials should compress against the dollar, not in its favor. That is why we maintain the structural debasement thesis: the USD rally is a crisis premium, not a regime change. When the fog clears, the medium-term path for the dollar remains lower.

Gold — Forced Liquidation, Not Fundamental Breakdown

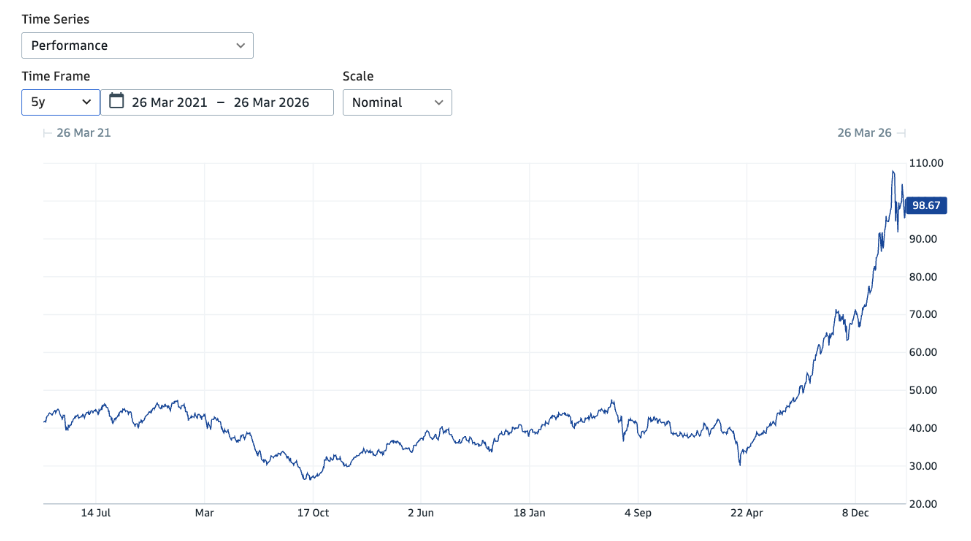

Gold has been the most painful surprise in the last week. After hitting an all-time high of $5,603 on January 29, the metal has corrected roughly 22% to trade near $4,320 — the worst drawdown since 1983 and the steepest weekly decline since the Volcker era. For an asset that had become a consensus crowded long, the violence of the move has shaken conviction across the allocator base.

We believe the selling is mechanical, not fundamental. The drawdown reflects a confluence of forces that are all temporary in nature: a stronger dollar, rising real yields, crowded positioning, and profit-taking after a historic rally. When the Iran shock broadened into a correlated sell-off across equities, credit, and rates, margin calls forced portfolio-wide deleveraging — and gold, as the most liquid non-dollar store of value, was sold to meet margin elsewhere. This is the classic pattern: gold sells in the acute phase of a crisis not because the thesis is broken, but because it is the easiest asset to monetize.

One theory we find plausible is that some Gulf sovereign holders may be selling gold for USD liquidity as the oil disruption reduces revenue and regional uncertainty rises. That would be consistent with both the magnitude and the character of the flows.

Despite the severity of the correction, we still like gold here — and three factors reinforce our conviction. First, the 200-day moving average has held. This is the level that has historically marked the floor of corrections within secular bull markets; a sustained break below would change the picture, but so far the defense has been strong. Second, EM central bank buying remains structural. China, India, and others continue to accumulate gold as part of long-term reserve diversification and partial de-dollarization — this bid is generational, not cyclical. Third, if the market eventually reverses the hiking assumption and moves back toward a cutting cycle, gold regains a powerful tailwind from falling real yields.

Gold also remains one of the best hedging instruments in a multi-asset portfolio — superior to most other commodities in terms of liquidity, portability, and crisis correlation. Tactical flows have hurt it this quarter, but strategically it remains one of our favorite longs.

Equities — Three Themes for Q2

We still hold a constructive stance on US equities, especially relative to the rest of the world. The US retains the strongest listed technology franchises globally and remains more resilient to the Iran shock than peers. We enter Q2 with equities significantly cheaper than where we started the year, and we believe this is an opportunity to position for the next leg. The Magnificent Seven — which carried the market to all-time highs in January — have collectively lost over 11% year-to-date, with not a single name in positive territory. SaaS names have been decimated. Yet the AI super-cycle has not ended — it has merely entered its proof phase, where the market demands execution, monetization, and free cash flow rather than narrative.

We organize our equity framework around three themes:

Theme 1: Mag7 as beta, not alpha. The mega-cap technology names remain the most liquid, efficient vehicles for expressing a directional view on the AI cycle. When the market turns — and we believe it will as Iran de-escalates — the Mag7 will lead the recovery simply because of their liquidity and index weight. We are buyers on further weakness.

That said, this is no longer a group where beta alone generates outsized returns. Even though earnings continue to beat expectations, capex concerns remain a persistent overhang. This is a regime shift from the last few years: the market has become much more cautious on multiples and is placing greater weight on free cash flow. Given the AI arms race, none of the hyperscalers wants to be left behind — which means capex stays elevated and near-term multiple expansion is limited. The Mag7 can still serve as portfolio beta, but alpha generation from the group is likely to be more constrained than in prior cycles.

Theme 2: SaaS — avoid on a long-only basis. This is a departure from our previous stance, and it deserves explanation. Since last October, Anthropic and peers have been releasing new tools, plugins, and agent-workflow capabilities at an accelerating pace, creating meaningful doubt around parts of the software business model. Those fears intensified after the publication of The 2028 Global Intelligence Crisis by Citrini Research, which laid out a detailed case for how agentic AI compresses the value of traditional subscription software. When an AI agent can perform the task that a SaaS tool automates, pricing power erodes — and this is no longer hypothetical. It is happening now in customer service, data entry, and basic analytics.

Interestingly, software has recently outperformed semiconductors during the Iran escalation — a short-term relative trade that might tempt some to re-enter. We think the business model remains fragile and vulnerable to recurring negative headlines — every new step-function release from Anthropic or a similar player resets the narrative downward. We would therefore avoid this theme on a long-only basis. For those with the capacity to run active long/short exposure, there are opportunities — but the survivors will be those that embed AI natively and become the platform layer, and picking winners here requires a level of professionalism we do not yet have.

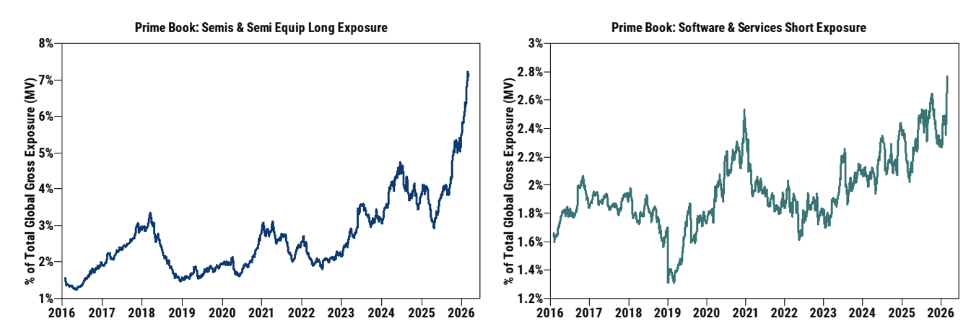

Theme 3: Bottleneck trades — where alpha lives. This is our highest-conviction equity theme. As the AI buildout accelerates, the binding constraints are not compute (which is scaling) but the physical infrastructure that enables compute.

Our own experience using agent tools heavily has made us more convinced that they can materially improve productivity, especially in local deployment settings. We have begun framing this as TASS — Token As Survivability Token: the idea that in an agentic economy, token consumption is not a cost center but a productivity multiplier, and companies that fail to adopt token-native workflows will be structurally disadvantaged. Token consumption should continue rising in both frequency and scale, while agent workflows require longer context windows and more compute-intensive memory usage. That supports a constructive medium-term view on memory, especially after the recent sell-off.

We are particularly focused on three sub-themes:

Energy and power: Data centers are reshaping electricity demand. BE, CEG, VST, and related names benefit from structural demand growth that is visible, contracted, and not easily substitutable.

Device and memory: Memory remains in a structural upcycle driven by HBM, DDR5, and GDDR7 demand. The pricing environment is firm, and the cycle has further to run — supported by the agent-driven compute thesis above.

Niche supply chain: This is where we see the most underappreciated opportunities. MLCC, T-glass substrates, ABF, high-end passive components, and advanced packaging materials are all experiencing demand that exceeds supply by meaningful margins. These are the physical choke points of the AI buildout — and unlike semiconductors, they have limited capacity to scale quickly. Japanese, Taiwanese, and Korean suppliers dominate these segments, and many trade at reasonable valuations relative to their structural growth profiles. Even after decent YTD performance, valuations still look broadly fair rather than excessive.

Overall, we remain constructive, but this is clearly not a market for broad beta complacency. Selectivity matters much more now than in the last cycle.

In summary, Q2 is shaping up to be a market that rewards conviction and punishes indecision. The assets we liked in December are now cheaper, the macro thesis we articulated has not changed, and the geopolitical catalyst for normalization—Trump’s midterm imperative—is as powerful as any fundamental driver. We are adding risk selectively: duration in rates, short CDS for carry, gold on the dip, and bottleneck equities for alpha. The fog of war will clear. Our job is to be positioned when it does.

Next week, we will publish Part II covering China and Japan, where the Iran shock creates a very different set of opportunities and risks. Stay tuned.