The New Arms Wrestling - AI and the Intensifying Global Competition for Energy

Forget the notion that widespread electricity shortages are a problem confined to less developed regions. Could you ever imagine the United States, the world's most advanced economy, facing the threat of widespread blackouts? The answer, alarmingly, is yes.

In July 2025, the U.S. Department of Energy (DOE) released its "Report on Evaluating U.S. Grid Reliability and Security," which delivered a stark warning. The report suggests that the premature retirement of existing power generation assets, coupled with significant delays in bringing new, reliable capacity online—a situation exacerbated by the aggressive green policies of past administrations—is creating a perfect storm. This is leading to a surge in power outages and a dangerous mismatch between soaring electricity demand and stagnant supply. The unprecedented growth of artificial intelligence (AI)-driven data centers is pinpointed as a primary catalyst, directly threatening America's energy security.

Therefore, we must look beyond traditional energy metrics like barrels of oil or cubic feet of gas. It is increasingly probable that the most critical resource of the 21st century is becoming the raw power required to think at scale. The race for AI supremacy is, in its most fundamental form, a race for energy. And the battle to feed AI's insatiable appetite has already begun.

Executive Summary

The rapid advancement and deployment of Artificial Intelligence (AI) are triggering a paradigm shift in global energy markets, igniting a new form of strategic competition. This report analyzes the convergence of factors creating an unprecedented surge in power demand, primarily from data centers. We project that the competition for reliable, scalable, and affordable energy will be a primary determinant of AI leadership and economic competitiveness through the end of the decade and beyond. Key findings indicate a generational demand surge, with U.S. electricity demand growth accelerating to 2.4-2.6% annually through 2030 after a decade of flat growth, driven overwhelmingly by data centers which are projected to grow from 3% to as much as 11% of total U.S. power demand. This competition is governed by a complex framework of factors: the Pervasiveness of AI applications, the Productivity paradox of more efficient chips driving higher total consumption, the ability to pay higher Prices, supportive and limiting Policy, and critical bottlenecks in Parts supply and skilled People. Significant constraints in power generation, transmission, and labor are creating regional energy hotspots. Furthermore, a corporate and geopolitical dimension has emerged, with well-capitalized technology hyperscale’s securing energy resources years in advance, and nations formulating policies to ensure their energy infrastructure can support AI-driven economic growth. The transition from a period of energy abundance to one of strategic competition for electrons is underway, and success will belong to those who can navigate this complex landscape of technological innovation, infrastructure investment, and policy enablement.

Introduction: From Digital to Physical

The AI revolution, often perceived as a purely digital phenomenon, reveals a profound physical reality: intelligence requires immense amounts of energy. The training and operation of large-scale AI models are computationally intensive processes that consume power on an industrial scale. This report synthesizes data from financial analysis, industry case studies, and market forecasts to investigate the following core question: why has competition for energy, particularly for AI development, become so intense? We argue that this competition is not a temporary market imbalance but a structural shift, fueled by the convergence of exponential growth in AI compute demand and the linear, capital-intensive nature of energy infrastructure expansion.

The Scale of the Demand Shock

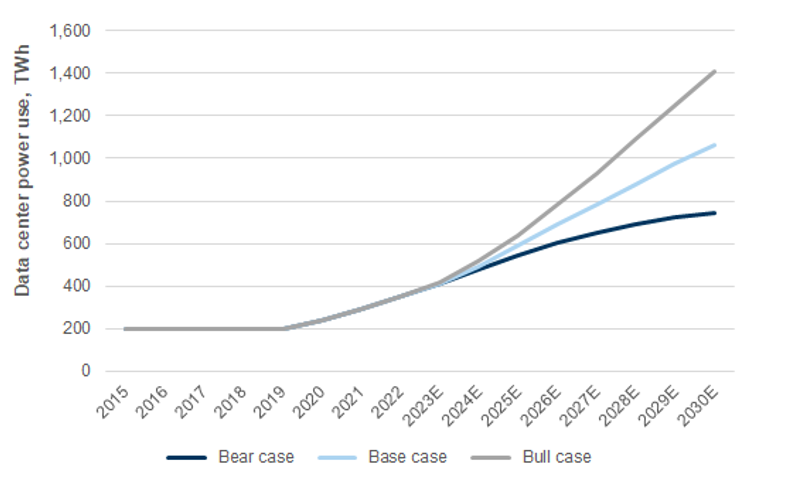

The primary engine of new electricity demand is the data center. After a period of efficiency gains that flattened power use despite growing data workloads between 2015 and 2020, the advent of large-scale AI has dramatically reversed this trend. Global data center power demand, excluding cryptocurrency, is projected to grow by approximately 175% from 2023 levels, reaching about 1,131 TWh by 2030. This growth is equivalent to adding electricity consumption of a top-10 global economy. This surge is most acute in the United States, the epicenter of AI development. U.S. electricity demand is forecast to accelerate to a 2.4-2.6% compound annual growth rate through 2030, a stark contrast to the nearly 0% growth over the previous decade. Data centers alone are expected to contribute 90 to 120 basis points to this growth rate, with their share of U.S. power demand projected to rise from about 3% in 2023 to between 8% and 11% by 2030. This represents a generational shift not seen since the early 2000s, forcing utilities and grid operators to radically revise long-term planning models.

The Analytical Framework: Drivers of the Energy Competition

The intensity of the competition can be understood through six critical, interconnected drivers. The first is Pervasiveness. AI is no longer a niche technology but is being integrated into nearly every sector, from healthcare and finance to manufacturing and transportation. This creates a ubiquitous, always-on demand for AI inference, exemplified by edge computing solutions that bring real-time analytics to smart cities and factories, creating distributed energy demand points beyond massive, centralized data centers.

The second driver is Productivity, which exhibits a classic Jevons Paradox. While hardware efficiency is improving dramatically, it is fueling, not curbing, total energy demand. For instance, NVIDIA's latest DGX B200 server is 15 times more computationally efficient than its predecessor from just a few years ago, yet its absolute power consumption per server has more than doubled. The impact on aggregate energy use hinges on a key constraint question. If customer purchases are constrained by budgets, they may buy fewer, more powerful servers, leading to a 20% increase in power use for a doubling of compute speed. However, in a scenario with no budget constraints, where customers buy the same number of new, more powerful servers, power consumption per unit of compute can soar by 500%.

The third driver is Price and the emergence of a "Green Reliability Premium." Financially robust hyperscalers like Google, Microsoft, Amazon, and Meta are willing and able to absorb higher energy costs. They are actively seeking 24/7 low-carbon power, which commands a premium estimated at $40 to $48 per MWh over a standard natural gas power plant. If applied to all global data center growth, this would cost the hyperscaler industry an estimated $29 to $34 billion annually by 2030, a manageable 2-3% of their projected EBITDA. This financial capacity allows them to outcompete other energy consumers for the most desirable and reliable power contracts.

The fourth driver is Policy. Government incentives, such as the U.S. Inflation Reduction Act, have accelerated renewable deployment. However, the potential sunsetting of these incentives and, more critically, lengthy permitting and interconnection queues for both generation and transmission projects act as a significant brake on new supply, intensifying the scramble for existing grid capacity.

The fifth driver is the availability of Parts, or supply chain bottlenecks. The pace of new power capacity is governed by the lead times of critical components. In the near-term, growth is limited by the supply of utility-scale solar panels, battery storage, and natural gas peaker plants. In the medium-term, new natural gas combined cycle plants are constrained by turbine availability. For the long-term, nuclear power faces the longest lead times but offers the most reliable baseload power. This sequencing creates a "ladder" of energy sourcing, where AI developers must compete for whatever capacity is available at each stage.

The sixth and final driver is People, specifically a severe skilled labor shortage. The energy transition and AI demand surge require a massive new workforce. Estimates indicate a need for approximately 510,000 new jobs in the U.S. power and grid sectors by 2030. The most critical constraint lies in the roughly 207,000 of these jobs needed for skilled transmission and distribution roles, such as linemen and engineers, which require three to four years of training. With an aging workforce and only about 45,000 active apprentices in the U.S. energy sector, this represents one of the most severe and tangible bottlenecks to overcoming the energy crunch.\

The Corporate and Geopolitical Arena

Competition extends beyond market fundamentals into the corporate and geopolitical spheres. The major technology companies are engaged in a hyperscale arms race, transforming from mere energy consumers into active energy asset managers. Corporate power purchase agreements for renewables skyrocketed to 33 GW in 2024, up from approximately 18 GW in 2023, as companies lock in supply for the better part of a decade. Some are exploring on-site generation, including nuclear microreactors, to ensure independence from the grid.

This competition is geographically concentrated, creating regional hotspots and infrastructure strain. Northern Virginia's "Data Center Alley" is a prime example, where utility Dominion Energy faced such severe transmission constraints that it temporarily paused new data center connections. The response was a $5 billion transmission upgrade approved by the regional grid operator, a scenario likely to be repeated in other key markets like Texas, Georgia, and the Midwest. On a broader scale, nations are recognizing that AI sovereignty is intrinsically linked to energy sovereignty. Policies are being crafted to ensure that domestic energy infrastructure can support a thriving AI industry, framing the issue as one of paramount economic and national security.

The hunger for power: who wins?

We generally categorize the beneficiaries of rising power demand—driven by the growth of data centers and AI—into two main groups. The first group consists of demand growth beneficiaries. These are companies exposed to increasing power needs and prices, such as unregulated power producers, natural gas firms, energy storage providers, and suppliers of power solutions tailored to data centers. It also encompasses businesses engaged in expanding power generation capacity to meet growing demand—including regulated utilities, merchant power producers, renewable energy companies, and manufacturers of power generation equipment. The second group includes supply chains and infrastructure beneficiaries. These are companies well-positioned to invest in the infrastructure and equipment required to support the expansion of power systems and enhance grid reliability. Below, we highlight Buy-rated stocks that align with these themes.

Demand Side:

- FSLR: As a major domestic solar panel manufacturer, FSLR is well-positioned to benefit from the anticipated surge in utility-scale projects required to meet rising power demand. We expect companies to increasingly source panels domestically to capitalize on domestic content incentives. In certain instances, FSLR engages in direct partnerships with data center owners, such as MSFT, further strengthening its market position.

- FLNC: This company stands to gain from the on-site deployment of its energy storage systems at data centers. The company provides clean backup power solutions that ensure grid reliability during outages. This capability is demonstrated by FLNC's collaboration with GOOGL, where it is supplying and optimizing zero-emission backup systems for a hyperscale data center.

Supply side:

- MYRG: We believe this firm could offer a unique play on data center growth through its transmission and distribution (T&D) work and its leadership in electrical contracting. The company is poised for compelling growth, and we are constructive on its direct exposure to key macro themes driving infrastructure investment.

- SRE: Its regulated utilities in California and Texas will require increased grid investment to support data center load. However, we expect the most significant impact to be on its Texas utility, Oncor. SRE has already substantially raised Oncor's capital plan in recent years, and we see potential for further incremental capital expenditure, particularly in transmission infrastructure, as data center expansion continues within its service territory.

Conclusion and Outlook

In conclusion, the competition for energy for AI development is fierce because it represents a fundamental clash between exponential digital growth and linear physical infrastructure expansion. The drivers of Pervasiveness, Productivity, Price, Policy, Parts, and People create a perfect storm that is reshaping energy markets, corporate strategy, and national policy. Looking forward, the winners of the AI era will be those entities—both corporate and national—that can successfully secure long-term, reliable, and cost-effective power. This environment will favor well-capitalized hyperscale’s and regions with proactive energy policies and robust grids, while potentially pricing out smaller players. Furthermore, the energy crunch will inevitably accelerate innovation in next-generation nuclear technology, advanced geothermal, and grid-enhancing solutions. The narrative around sustainability will remain complex, as the AI boom simultaneously increases near-term fossil fuel demand for reliability while acting as the single largest driver of corporate investment in renewables. Ultimately, energy has become a foundational resource for the AI era, as critical as the algorithms themselves. The race to build and power intelligence is, fundamentally, a race to secure electrons, making the energy sector a central battlefield for technological and economic supremacy in the 21st century.