2025 H2 Global Economics Outlook (Japan & Europe)

2025 H2 Global Economic Outlook (II) – Japan and Europe

Japan

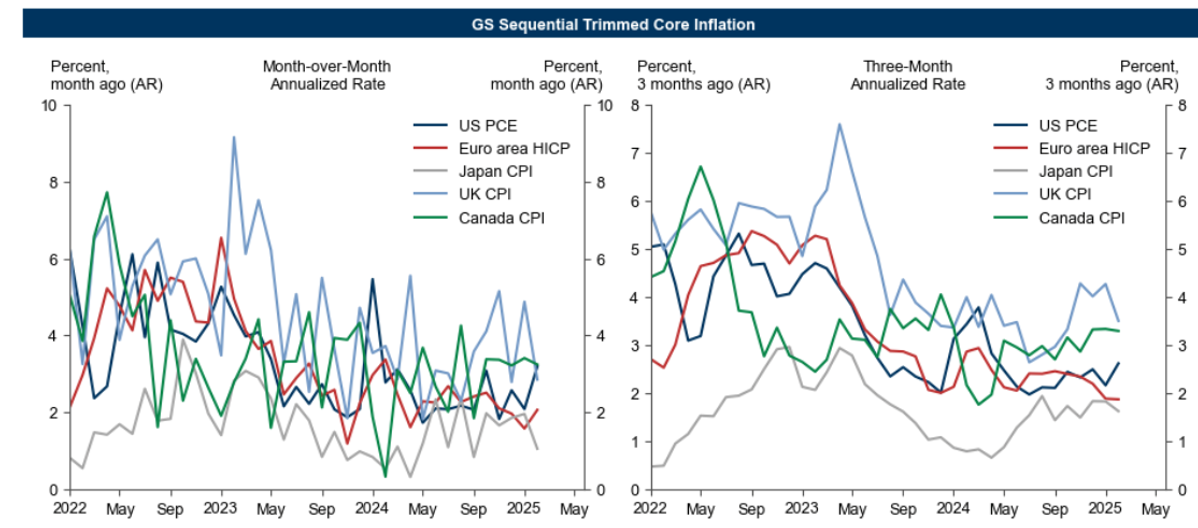

Inflation Pressures Persist

Japan has been grappling with the elevated inflation levels in the first half of 2025. As of May, Japan nationwide CPI rose 3.5% yoy, remaining above the BOJ’s long-term 2% target for 38 consecutive months. Core inflation (excluding fresh food) reached a two-year high at 3.7%, while the so-called “core-core” index—excluding both fresh food and energy and viewed by the BOJ as a better gauge of demand-driven pressures—accelerated to 3.3%, its fastest pace since January 2024.

The key driver of the inflation uptick has been food prices. Core food inflation surged 7.7% yoy in May, deepening the strain on household purchasing power. Notably, rice prices more than doubled, soaring 101.7% from a year earlier—marking the largest annual increase in over a half century.

While the 2025 Shunto wage negotiations delivered an average wage hike of 5.46%—the strongest since 1991—it has not been sufficient to offset the impact of rapidly rising living costs. Real wages remain under pressure, and consumer sentiment has deteriorated as a result.

From our perspective, an additional rate hike should be stay in place throughout 2025 despite the global uncertainties on tariff and Trump. Indeed, a recent BOJ research paper also cautioned that hiking rates too slowly while raw material costs continue to rise could trigger a wage–price spiral, eroding the central bank’s credibility and pushing inflation ahead of productivity gains.

BOJ's Reluctance to Tighten Policy

While in theory, inflation conditions might justify additional hikes, in practice, monetary policy decisions are shaped as much by political and market considerations as by macroeconomic fundamentals.

Over the past few years the BOJ has been taking a wait-and-see & data dependent approach. Ueda became Poseidon’s biggest enemy, consistently thwarting our efforts to achieve 100% accuracy in forecasting central bank policy moves. In the June MPM, the BOJ again kept the rate steady at 0.5% emphasizing the cautious stance due to uncertainties surrounding US Tariff and middle-east tensions.

Since taking the helm in 2023, Ueda has consistently favored measured policy adjustments, typically signaling intent via media leaks before making formal moves. This playbook allows the BOJ to test market reactions in advance, minimizing unintended volatility. For traders, this means that any JPY appreciation linked to policy speculation tends to front-run official announcements by several weeks.

Our conviction is that BOJ will refrain from hiking again to the extent possible in H2 2025.

1) In spite of the continuous inflationary pressure, for Japan – a country that suffered decades of deflation and wage stagnation – some degree of price growth is widely regarded in Japan as a necessary step toward structural normalization. Compared globally, Japan’s CPI still ranks among the lowest across major DM economies. Many of today’s policymakers came of age during the sharp downturn following the late 1980s, and they appear deeply committed to ensuring the country decisively escapes the grip of deflation. This backdrop supports a broadly dovish policy stance, with authorities intent on keeping rates—particularly long-term yields—as low as possible, even if it means tolerating some public dissatisfaction.

2) Japan’s real estate sector has seen strong post-COVID performance, thanks to robust demand from foreign buyers. Low interest rates have played a pivotal role in sustaining this property market momentum. A supportive housing market not only drives construction and investment but also fosters positive wealth effects, which can stimulate broader household consumption. As such, the BOJ has strong incentives to preserve accommodative financial conditions to maintain this virtuous cycle.

3) Another key constraint on monetary tightening is the unresolved trade friction between the US and Japan. Despite multiple rounds of bilateral discussions since the Liberation Day, no comprehensive deal has yet been reached. With Q1 GDP showing zero growth, Japan’s economic outlook remains fragile. The country’s heavy reliance on exports—particularly in autos and electrical machinery—makes it especially vulnerable to external shocks. In this context, the BOJ is unlikely to risk premature tightening that could exacerbate downside risks or force a policy reversal if trade tensions deteriorate further.

4) The Japanese yen holds a unique position in global financial markets as a key funding currency, given Japan’s low interest rates during 2010s. When the BOJ delivered a surprise rate hike last summer—at a time when markets were not positioned for it—JPY appreciated sharply, triggering one of the largest equity drawdowns in the US in 2024. This episode highlighted the yen’s central role in global liquidity dynamics and underscored the unintended spillovers of BOJ policy. Policymakers are now acutely aware of the potential consequences of policy missteps on Japan’s major trading partners, particularly the US and are therefore likely to tread carefully ahead of any formal trade agreement.

Currently the OIS market has priced-in 15bps hike by the end of the year.

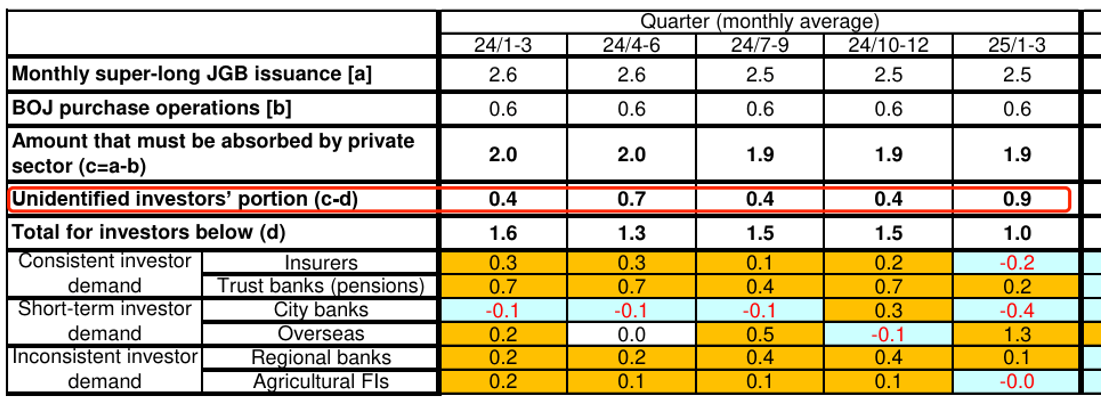

JGB Chaos

Japan's government bond (JGB) market has experienced volatility, particularly in the super-long segment. In response, the Ministry of Finance recently announced a significant reduction in the issuance of 20-, 30-, and 40-year JGBs to address market concerns of oversupply and calm recent volatility. However, the demand for the latest JGB 20y auction on this Tuesday was still weak.

Since 2022 amid covid, bond yields across the world have risen due to persistent inflation, higher-for-longer central bank guidance, and structural fiscal loosening (especially in the US and UK). However, Japan’s shift is most structurally significant, from a low of 0.525% to nearly 3.0% in five years。

We believe that JGB yields have substantial room to rise compared with its global peers. First of all, Japan has operated under ultra low or even negative interest rates for decades, reinforced by aggressive BOJ aggressive bond buying (i.e. YCC and QQE). Even though BOJ remains dovish, the perception of permanent repression of long end rates is fading. As a result, Long-term JGBs are no longer seen as risk-free “anchored” assets — JGB yields are rising to reflect market expectations.

Secondly, it is worth noting that Japan’s debt-to-GDP is the highest among major economies (~250%), and the government is used to issuing long dated bonds to fund stimulus. However, the latest announcement from BOJ to reduce JGB purchases means that the private sector must absorb more issuance, and considering sticky inflation and potential policy lag, together with the liquidity fears that BOJ now owns over 40% of the JGB market, investors demand higher yields for liquidity and fiscal risks (or “credit risk“).

Thus, with this structural shift we suggest investors avoid JGB investment at this point.

Japanese Yen Range Trading Strategy

The Japanese yen remains firmly positioned as a top-tier reserve currency, accounting for roughly 5–6% of global central bank holdings, according to IMF data. Its safe-haven status also gives it outsized influence in Asia, where it often serves as a regional policy anchor for emerging markets.

As a leading exporter of automobiles, semiconductors, and precision machinery, Japan relies heavily on a stable and competitive exchange rate. Even a single-yen move can significantly impact earnings across key sectors, making FX stability a cornerstone of economic policy.

This creates a complex balancing act for Japanese authorities. On one side, Tokyo must maintain a cooperative stance with the Trump administration, which is laser-focused on reducing trade deficits. On the other, it must safeguard the yen’s competitiveness to sustain export momentum. With the Federal Reserve deep into an easing cycle, the narrowing US-Japan yield differential has heightened FX sensitivity to BOJ signals, increasing volatility.

That volatility is unwelcome though. Japan’s recovery still depends on steady export receipts and inbound tourism, both of which benefit from a weaker currency. But an excessively soft yen risks importing inflation, driving up the elevated CPI, squeezing households. and complicating the BOJ’s policy calculus.

This policy dilemma likely limits the BOJ’s room to maneuver. From our perspective, a USDJPY range of 140–150 represents a pragmatic equilibrium. A good strategy from our perspective is to tactically express this view via forward positioning — entering near the edges of the band and unwinding as the pair reverts toward the mean.

Neutral Stance on TOPIX & NKY

Japan’s equity landscape is best understood through the lens of its two flagship indices — Nikkei 225 (NKY) and TOPIX — which reflect different structural exposures and macro sensitivities. The NKY has a disproportionately high weighting toward large-cap tech and consumer discretionary names such as Tokyo Electron, Advantest, and Fast Retailing. This gives it a higher beta to US tech sentiment and makes it more responsive to Nasdaq dynamics.

In contrast, TOPIX offers broader representation of the Japanese corporate sector. It is more sensitive to domestic macro conditions and BOJ policy, particularly given its heavier allocation to financials, industrials, and traditional exporters. The Japanese yen, given its influence on margins and competitiveness across Japan’s export-heavy sectors, remains a key driver for both indices — but more so for TOPIX.

While long-term structural reforms— such as corporate governance improvements and increased shareholder returns remain supportive over the medium term, and we maintain a constructive view on US equities, which indirectly supports Japanese names via the NKY’s tech exposure, our stance on Japan equities for H2 2025 is neutral.

- Political Uncertainty: The upcoming Upper House elections on July 20 pose potential risks. If the ruling bloc fails to secure a majority - having already lost the Lower House-policy continuity could be disrupted.

- Trade Negotiations: Japan-US trade talks face challenges, particularly concerning automobile sector disagreements. The likelihood of concluding these talks by the July 9 deadline appears low, but we do high probability of common ground to be established.

- Defence Spending Pressures: Planned 2+2 security talks may be cancelled due to U.S. pressure on Japan to increase defence expenditures.

Europe

ECB’s Easing Cycle Progresses Amid Inflation Moderation

As of June 2025, the European Central Bank (ECB) has delivered eight rate cuts since June 2024, bringing the deposit facility rate down to 2.00% from a peak of 4.00%. This aggressive policy pivot reflects the ECB’s response to consistent disinflation trends, with euro area headline inflation easing to 1.9% in May — slipping below the 2% target for the first time since Sep 2024.

The ECB is now entering a more measured phase. At the June 5 meeting, President Lagarde emphasized that monetary policy is “well positioned” at current levels, signalling a pause in July barring major data surprises – policy stance we agree with. Markets are now pricing in the next rate cut for September, consistent with the ECB’s incremental approach to easing amid global uncertainties.

Yet beneath this policy normalization lies a surprisingly resilient eurozone economy. The latest upward revision to Q1 GDP was largely driven by front-loaded activity ahead of anticipated US tariffs, but underlying momentum remains supported by stepped-up fiscal efforts in Germany and France. Both governments have committed to increased defence spending and infrastructure investment, in part to buffer against the geopolitical vacuum created by a potential US withdrawal from NATO.

Multi-tiered Economic Bloc

As Middle East tensions begin to subside, Europe’s strategic focus is pivoting back to its transatlantic relationship. With US trade policy turning increasingly protectionist, Brussels faces the challenge of responding to potential tariffs while also navigating its balancing act between Washington and Beijing. This evolving dynamic is not only reshaping Europe’s foreign policy posture but may also reinforce its role as a global swing player — with both the US and China vying for influence through trade, technology, and diplomacy.

From an economic perspective, the risk of US-imposed tariffs on European goods — particularly autos and luxury exports — looms large over the second half of 2025. While energy security concerns have diminished since the 2022 energy crisis, trade friction has re-emerged as the principal macro risk facing the continent.

One of the defining features of 2025 is the widening policy divergence within Europe (multi-tiered economic bloc):

- Germany and France have pivoted to expansionary fiscal policies, with increased defence and infrastructure spending—partly in response to Washington’s shifting security commitments and rising regional geopolitical threats.

- In contrast, Italy and the periphery remain constrained by higher debt loads, tighter funding conditions, and limited room for maneuvering.

- The Bank of England remains an outlier, keeping rates elevated at 4.75% amid lingering services inflation and sticky wage growth. UK inflation dynamics continue to differ from the eurozone due to a tighter labor market, continued housing price resilience, and the delayed pass-through of energy shocks. The BoE is likely to stay cautious well into Q4, especially given the proximity to the next general election.

EU Investment Opportunities

Against this complex backdrop, investment strategies in Europe should reflect both cyclical resilience and latent policy risk.

In equities, performance is likely to be uneven and highly sector-dependent. On the constructive side, companies tied to national security and infrastructure — particularly in Germany and France — stand to benefit from fiscal tailwinds and political support. At the same time, consumer staples and utilities may continue to outperform as inflation recedes and rate volatility diminishes, providing a defensive ballast to portfolios. Conversely, export-sensitive sectors such as industrials and autos could face renewed headwinds should trade tensions with the US escalate.

In fixed income, the ECB’s rapid rate cutting has revived duration appeal. With the policy rate nearing terminal levels and growth holding up, we see value in the 5–10Y part of the curve, where carry remains attractive without excessive exposure to long-end volatility. Sovereign debt from core eurozone countries — especially France and the Netherlands — may benefit from supportive demand amid modest issuance and a favorable inflation trajectory.

On the FX front, while the narrowing US–eurozone yield spread supports a stronger euro, we remain cautious. With the Fed still on hold and tariff negotiations unresolved, EURUSD may remain range-bound. From a tactical perspective, short-term rallies should be viewed as opportunities to trim exposure, with positioning skewed toward defensiveness until greater clarity emerges.

Switzerland: Transition to Zero Interest Rate Policy

The Swiss National Bank (SNB) delivered another rate cut to 0% this month, attributing disinflation to tourism trends and lower oil instead of currency gains. While the SNB retained its guidance that it remains willing to intervene in foreign exchange markets “as necessary,” there was no shift in tone or language regarding FX operations. This pre-emptive easing highlights Switzerland’s distinct disinflationary trajectory and further distinguishes the SNB’s stance from that of the BoE and ECB, which we believe will continue to be the case.

Over the past three years, while other major DM central banks pursued aggressive tightening cycles, Switzerland’s relatively low and stable rates made the CHF a preferred funding currency. It offered the dual advantages of low carry costs and stable FX volatility. However, since the beginning of 2025, the Swiss franc has outperformed nearly every G10 currency, making CHF short positions increasingly painful. This move has been driven by heightened tariff uncertainty, Middle East tensions, and the resurgence of CHF’s safe-haven appeal, which has arguably been more potent than that of the yen. One possible explanation: unlike Japan, Switzerland does not exhibit persistent underlying inflation, making the franc a purer defensive asset. In many ways, CHF price action in 2025 has mirrored gold — a classic safe-haven correlation.

Looking ahead, some investors expect CHF strength to persist, particularly in a scenario marked by geopolitical flare-ups, the looming “Big and Beautiful” tax plan, or the potential escalation of reciprocal tariffs under the Trump administration. With the SNB tolerating modest franc appreciation and Switzerland’s domestic data playing a secondary role, global macro dynamics—especially USD weakness—are now the primary driver of CHF performance.

However, CHF is now approaching multi-decade highs, with USDCHF near 0.81. Historically, the pair has traded below 0.80 for only 15 days in the past 20 years. While we recognize the franc’s safe-haven role in times of stress, we believe that current levels present an attractive entry point for short CHF positions. From a risk-reward perspective, the bar for further CHF appreciation is high, and normalization in global sentiment could quickly reverse recent gains.