Understanding Structured Products Series 7:Discovering a More Advanced Play - Accumulator

Discovering a More Advanced Play

Discovering a More Advanced Play

Prologue

“I actually liked that Accumulator we talked about last time,” Ada said, scrolling through her stock app. “But we only went over the concept and how to use it—we never really dug into how it actually works.”

“Exactly,” Jane laughed. “All I remember is that it lets you buy stocks in batches at a discount. But where does that discount come from? Why would the bank give it to you?”

Tom and Jerry exchanged a knowing look and smiled.

“Alright,” Tom said, “let’s break it down today. This time, let’s use NVDA as our example—currently trading at $100.”

Act I: Sell Put – Promising to Buy When Others Are Afraid

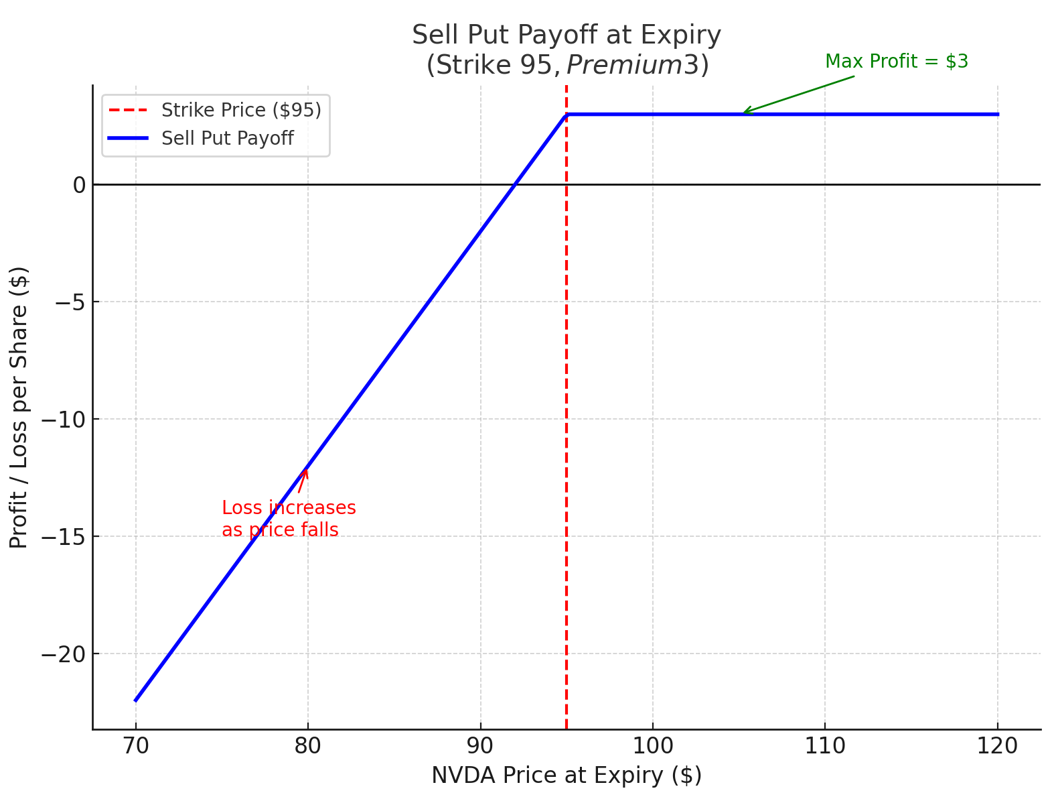

Tom wrote “Sell Put” on the whiteboard:

“Suppose the U.S. government announces stricter AI chip export controls. You expect NVDA’s stock price to come under short-term pressure. You agree to sell a put option with a strike price of $95.”

• Meaning: You promise your counterparty that if NVDA falls below $95 at expiry, you will buy it at $95—whether the market is at $94 or even $80.

• Return: In exchange for that promise, you receive an option premium (say, $3 per share).

• Risk: If NVDA falls below $95, you must buy at $95, even if the market is much lower.

Jerry added: “It’s like selling insurance—someone else fears a drop, you take the premium and promise to take delivery if it happens.”

Ada grinned: “So if I was already happy to buy NVDA at $95, I could also pocket the premium?”

Tom nodded: “Yes—but be careful. If it drops much further, say to $80, you still have to buy at $95.”

Act II: Buy Call – Locking in Future Upside with Small Capital

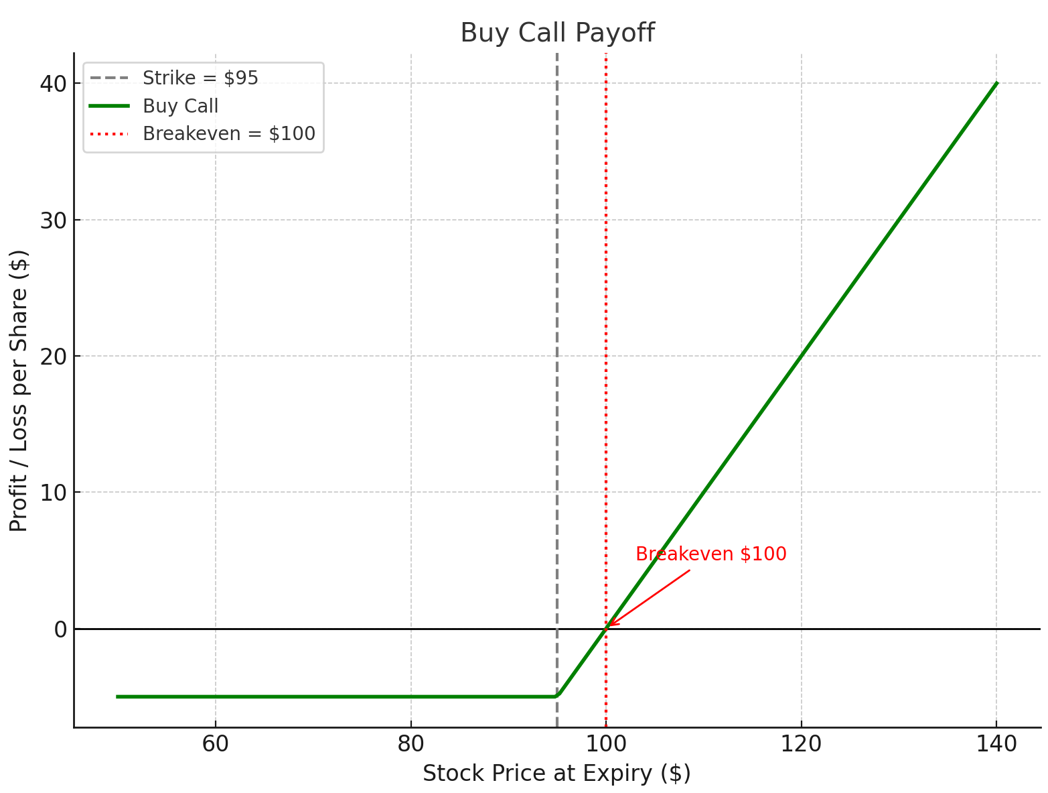

Jerry moved to the next board:

“Now suppose you’re also bullish on NVDA long-term and think it could push past $120 or even higher. You could buy a call option with a strike price of $95.”

• Meaning: This gives you the right, but not the obligation, to buy NVDA at $95 on or before a set date.

• Return: If NVDA rises to $130, you can buy at $95 and have an immediate $35 per share gain (minus the option premium).

• Risk: If NVDA falls below $95 upon maturity, the option expires worthless and you only lose the premium (say, $5).

Ada nodded: “So buying a call is like using a small stake to bet on a big rally—limited downside, but you capture upside if it comes.”

Act III: Sell 2 Puts + Buy 1 Call – Solving for the Strike Level

Tom drew the structure on the whiteboard:

“One of the core features of an Accumulator is that if the price drops below the strike level, you take delivery of double the daily quantity. This 2× feature means we can describe the structure with an equation:”

2 × Put(95) = Call(95)

Where:

• Put(95) = value of a put sold at the $95 strike

• Call(95) = value of a call bought at the $95 strike

• Left-hand side = income from selling two puts

• Right-hand side = cost of buying one call

Tom explained: “The bank uses market data—spot price, volatility, tenor, knock-out level, risk-free rate, dividend yield—and an option pricing model (Black-Scholes or local volatility) to calculate the strike level that makes this equation hold.”

Why do this?

• Strike too high → Put income exceeds call cost, but the investor’s downside risk is large

• Strike too low → Put income won’t cover the call cost, and the structure is no longer ‘zero-cost’

• Solving the equation finds the strike that perfectly balances put income and call cost

Jerry added: “This is why the strike level in an Accumulator always feels like the ‘perfect’ discount—it’s not random, it’s computed from the option pricing formula.”

Act IV: The Knock-Out Mechanism (“Up-and-Out”) and Contract Details

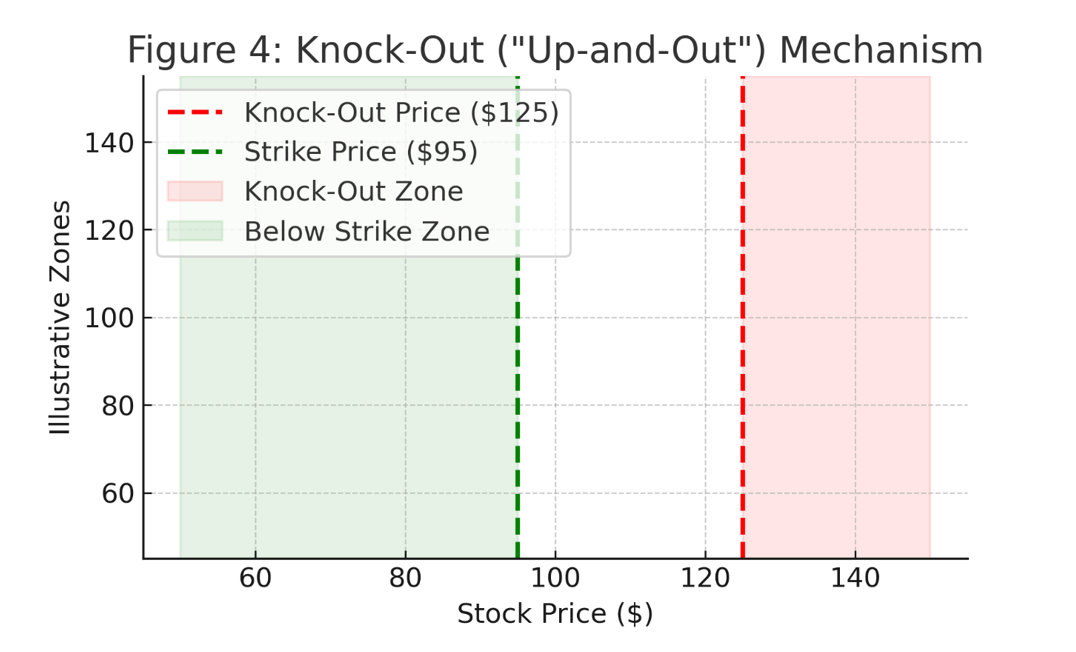

Jerry continued: “Most AQ products also include a knock-out clause—this is an up-and-out barrier feature: if the stock price hits a certain upper limit, the contract ends immediately.”

• What does ‘up-and-out’ mean? In barrier option terms, it means once the underlying price rises above the preset barrier, the option ceases to exist.

• In an AQ: If NVDA rises above the knock-out price (say, $125), the contract terminates early and no further daily purchases occur.

• Purpose: This limits investor upside but also protects the bank from prolonged exposure at unfavorable prices.

Why include it?

Without a knock-out, the call option embedded in the structure would be deep in the money for potentially a long time—making it expensive. Adding the barrier reduces the call’s cost, allowing it to be fully funded by the two puts you’ve sold. Without it, the 2 × OTM put = 1 ITM call balance would not hold in most cases.

Other core terms:

• Strike Price: $95

• Knock-Out Price: $125

• Daily Quantity: e.g., 1,000 shares; doubles to 2,000 shares if below strike (2× put trigger)

• Tenor: usually 3–12 months

• Leverage Factor: 2× clause rapidly increases position size in a falling market

Tom warned: “Because it’s observed daily, the leverage is cumulative—continuous declines can lead to massive holdings.”

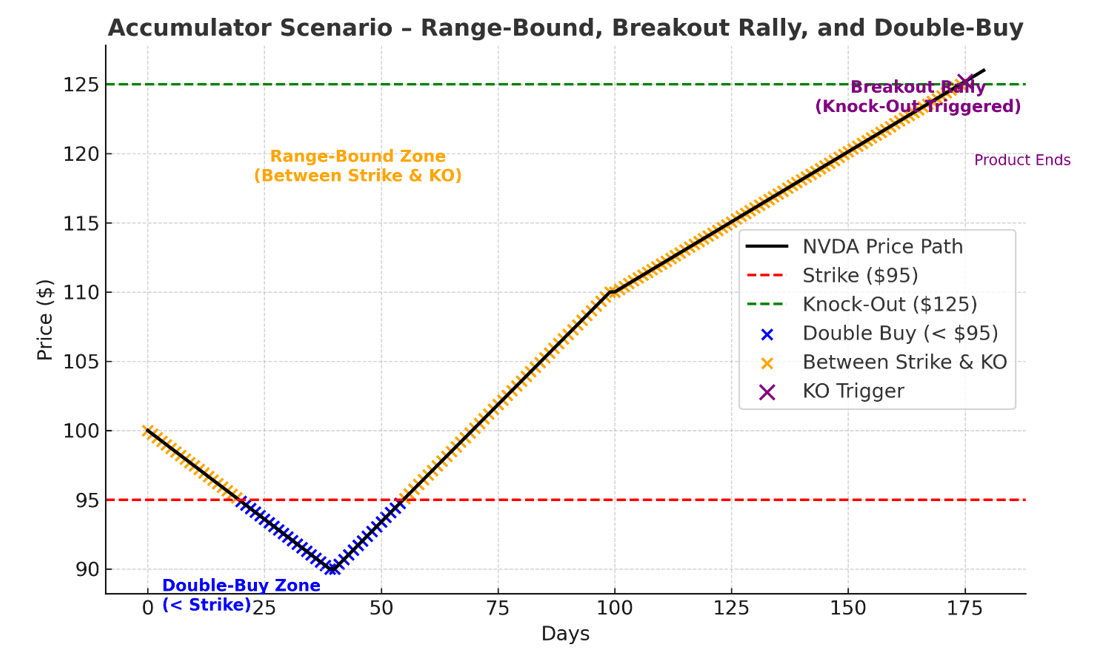

Act V: NVDA AQ – Three 6-Month Scenarios

Scenario A: Range-bound ($95–$115)

• Most days above $95 → Puts not triggered, call retains value

• Near knock-out → Call could lock in gains early

Scenario B: Breakout Rally (to $125)

• Knock-out triggers; call profits significantly

• Accumulated shares cost less than market, producing a large paper gain

Scenario C: Sharp Drop (to $80)

• Almost daily put triggers at double quantity

• Position balloons; average cost still above market, paper loss widens

Act VII: Pros and Cons

Pros

• Low-cost entry: Put income offsets call cost, sometimes zero net cost

• Gradual position building: Avoids full upfront capital commitment

• Upside participation: Retains call’s upside potential

Cons

• Falling market magnifies holdings: Sell 2 Put means buying more as price falls

• Locked purchase price: Must buy at strike even if market is far lower

• Knock-out limits upside: Profits capped if KO is hit early.

• Complex terms: Must understand knock-out, knock-in, leverage

Act VIII: Investment Takeaway – When It Works, When It Hurts

Why Some Investors Consider It

• Discounted Entry – The strike is usually set below spot, meaning you may buy shares cheaper than today’s price.

• Zero entry cost – The income from selling puts offsets the cost of the call, sometimes making the structure cost-neutral.

• Upside Participation – The call lets you ride a rally up to the knock-out price, capturing part of the gains without committing full capital upfront.

• Disciplined Accumulation – Instead of lump-sum buying, the daily/weekly observation enforces staggered entries, which can smooth out volatility.

When It Makes the Most Sense

• You have high conviction in the company’s long-term growth (e.g., NVDA’s AI leadership).

• You are willing and financially able to buy more shares if the price falls.

• You have liquidity to handle possible double delivery during downturns.

• You want exposure with defined terms rather than open-ended buying.

• You’re comfortable trading some upside (due to knock-out) in exchange for cheaper entry.

The Flip Side – When It Can Hurt Badly

• In a prolonged bear market, the 2× delivery accelerates stock accumulation at falling prices.

• Liquidity stress – If the market drops sharply, you may be forced to buy more shares than planned, tying up capital or forcing sales elsewhere.

• Early knock-out – If hit, you may end up with fewer shares than you wanted just before a big rally.

• Hidden leverage – Daily observation means losses (or exposure) can compound faster than many expect.

• Complex terms – Without fully understanding knock-out, knock-in, and delivery rules, it’s easy to underestimate the true risk.

Jerry leaned forward with a final word:

“An Accumulator works best when your patience, liquidity, and conviction are all strong.

If you get the direction right, it’s like buying your favorite stock at a discount while still riding part of the rally.

If you get it wrong, you’re not just stuck with the stock—you could end up owning a lot more of it than you ever planned.”