Stablecoins — Slowly Becoming “Stable”?

In our past Weekly write-ups, we traced Bitcoin’s journey from two pizzas to one million iPhones, and mapped its evolution from a speculative asset to a macro-relevant reserve alternative. Alongside, we explored how digital assets are no longer fringe, but are increasingly central to how capital formation, liquidity, and trust are being redefined in the 21st century. Today, another force is rising quietly—but just as powerfully—in the digital asset world: stablecoins.

As of July 2025, stablecoins are no longer just instruments of payment—they are levers of geopolitical influence, monetary strategy, and financial infrastructure. This report offers an investor-focused lens on the evolving U.S.-centered strategy to position dollar-backed stablecoins as a digital extension of the dollar system. Against the backdrop of a politically favorable administration, regulatory acceleration, and global fragmentation, we explore how stablecoins are being weaponized to reassert dollar dominance, attract capital to U.S. Treasuries, and reinvent cross-border financial rails. Investors should view stablecoins not as mere payment tools, but as programmable sovereign capital flows backed by the credibility of U.S. policy, global demand for liquidity, and scalable monetary interoperability.

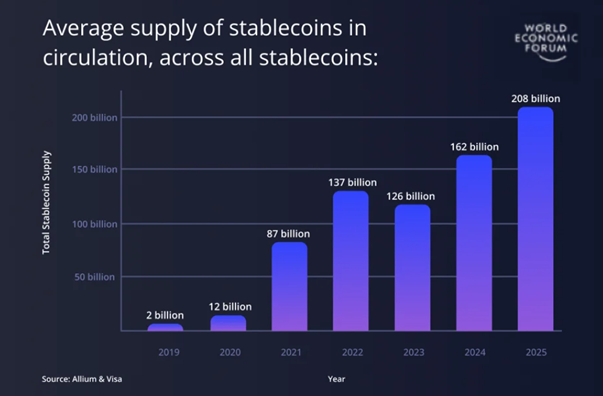

In 2019, stablecoins were a modest side note in the digital asset landscape, with a total supply of just $2 billion. Fast forward to today, and that figure is projected to exceed $260 billion, driven by a surge of interest from global banks, leading fintech platforms, and Web3 builders who are transforming the way money moves around the world. What’s fueling this rapid rise? Simply put, legacy payment systems are too sluggish, costly, and fragmented to keep pace with today’s global economy.

Traditional financial systems are often slow, expensive, and outdated—exactly why stablecoins are gaining rapid traction worldwide. Today, banks, enterprises, and fintech firms increasingly see stablecoins as a faster, more reliable way to move value and tap into new revenue streams.

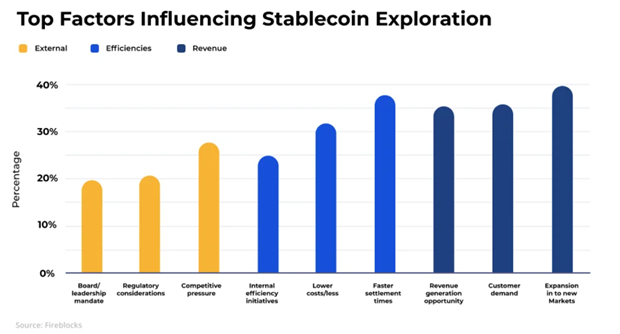

What’s fueling this momentum? Faster settlement times, significantly lower transaction costs, growing regulatory clarity in regions like the EU and Asia, and rising customer demand for modern, real-time payments. Stablecoins are quickly evolving from an experiment into a strategic necessity.

The Fundamental Logic of Stablecoins: The Beginning of Platformized Finance

Stablecoins are no longer just programmable money. They’re becoming the connective tissue of a fragmented global financial system—serving as interoperable value pipelines between banks, fintechs, DeFi protocols, and national economies. Think of them as the TCP/IP of finance: invisible to most users, yet fundamental to how transactions move across increasingly digital economies.

Their programmability enables a new paradigm in financial settlement: 24/7 availability, composability across platforms, and instant finality. Whether embedded into corporate treasury systems, powering Web3 apps, or facilitating retail payments, stablecoins offer a near-frictionless alternative to legacy rails like SWIFT or ACH. Importantly, this transformation is not happening in isolation—it's tightly coupled with evolving regulation and geopolitics.

Much like how broadband internet transformed retail and media through ubiquitous, programmable infrastructure, stablecoins are doing the same for payments, banking, and capital markets. The most profound changes often start at the protocol layer, and that’s where stablecoins live—invisible but indispensable.

Use Cases and Commercialization Pathways

The real driver behind stablecoins' explosive growth isn’t hype—it’s utility.

For corporations, stablecoins are rapidly becoming a tool for global treasury optimization. Companies can pay international contractors, manage FX exposure, and settle cross-border invoices—all without touching the correspondent banking system. In Latin America, Africa, and parts of Asia, freelancers now routinely request payment in USDC or USDT to shield themselves from local currency volatility.

On the consumer side, stablecoins are breaking into everyday finance. PayPal, VisaNet, and Stripe have all integrated stablecoin rails. What this means is users can now hold digital dollars in their wallets and spend them like fiat—bridging the UX of Web2 with the trustless backend of Web3. Stripe's acquisition of a stablecoin issuer Bridge in 2024 was a turning point, signaling that the biggest fintech platforms now view stablecoins not as competition, but as infrastructure.

Even banks are paying attention. In Asia and the Middle East, banks are experimenting with using stablecoins for cross-border interbank settlements and programmable FX flows. What was once a fringe crypto product is now reshaping mainstream financial plumbing.

Furthermore, we are seeing B2B and payroll adoption accelerate. As of Q2 2025, over 280 enterprise platforms support stablecoin settlements. Companies across supply chains, from agriculture to digital media, are using stablecoins for faster, cheaper, and programmable payments. When paired with tokenized invoices and smart contracts, stablecoins unlock real-time working capital management.

U.S. Policy Realignment: From CBDC Rejection to Stablecoin Acceleration

The U.S. government has made a strategic pivot. Instead of pursuing a central bank digital currency, it’s doubling down on regulated, privately-issued stablecoins as the digital backbone of dollar expansion.

In July 2025, “Crypto Week” on Capitol Hill saw the advancement of three critical bills that will define America’s approach to digital assets for the next decade. At the same time, the Trump administration has embraced the crypto sector—banning CBDCs while supporting innovation-friendly frameworks that empower private stablecoin issuers.

This pivot is not just economic—it’s ideological. The U.S. is positioning stablecoins as a free-market alternative to state-run digital currencies. The approach also reflects an understanding that global financial architecture is shifting from centralization to decentralization, and America intends to lead this evolution with private-sector-led innovation backed by regulatory clarity.

Why the U.S. Is Backing Stablecoins?

• Consolidating Tech and Finance Dominance: For four decades, the U.S. has led global value chains through technological and financial primacy. Stablecoins are the convergence layer of both.

• Rebuilding Treasury Demand: Foreign holdings of U.S. Treasuries have dropped precipitously. Stablecoin issuers like Tether and Circle are stepping in, holding over $120B in T-bills—making them stealth liquidity anchors for the U.S. debt market. Though such figure may sound like a drop in a bucket compared to $37T in debt for now, the demand will grow alongside the increasing numbers of the user cases.

ARK Invest estimates that if stablecoin market cap reaches $2T by 2028, reserve mandates could drive up to $1.6T in demand for U.S. debt. That’s a bigger buyer base than Japan.

• Digital Dollarization Strategy: In a world where China is rolling out its digital yuan and Europe is piloting the digital euro; the U.S. is using private stablecoins as its answer. These tokens enable dollar access abroad without relying on Fed accounts or correspondent banks.

Legislative Framework: The Three-Pillar U.S. Strategy

1. GENIUS Act – Stablecoin Legalization

• Allows stablecoin issuance by banks, licensed non-banks, and regulated state-chartered entities

• Requires 1:1 reserve backing with high-quality liquid assets (e.g. T-bills, FDIC-insured cash)

• Forbids interest-paying stablecoins and algorithmic models

• Monthly disclosures and annual third-party audits

By institutionalizing stablecoins, the GENIUS Act turns them into de facto digital cash, embedded within the U.S. regulatory perimeter.

2. CLARITY Act – Token Lifecycle Governance

• Classifies tokens based on lifecycle: pre-launch = securities, post-decentralization = commodities

• Assigns SEC oversight during fundraising, shifts to CFTC after project decentralization

• Includes safe harbor for DeFi interfaces and startup exemptions for small token offerings

This modular framework gives token projects a path to graduate into compliance.

3. Anti-CBDC Act – Digital Dollar by Private Sector

• Explicitly bans the Federal Reserve from issuing a retail digital dollar

• Reflects ideological and commercial preference for private rails over state-run solutions

Together, these laws build a coherent regulatory stack that favors stablecoins over CBDCs as the future of U.S. digital money.

Global Pushback: Fragmentation and Sovereignty Fights

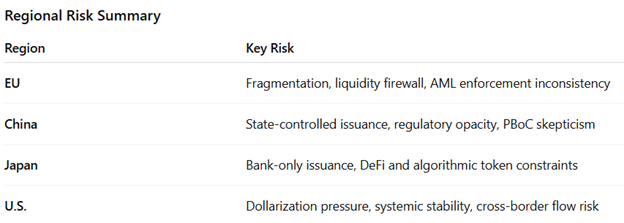

1. European Union – “European Walling”

Since June 2024, MiCA (Markets in Crypto Assets) has imposed tight rules: stablecoin issuers must localize reserves, hold at least 30% in liquid assets, and comply with a daily transaction cap of €200 million per issuer.

Risk: This effectively creates a legal barrier, preventing U.S. dollar stablecoins from dominating EU markets. While some issuers (e.g., Circle) have launched EU licensed affiliates, differences between U.S. and EU versions (e.g., in redemption rights) may lead to reduced fungibility and operational friction.

2. China & Hong Kong – Strategic Reinvention

While mainland China continues its ban on crypto, Shanghai is now exploring yuan pegged stablecoins, and giants like JD.com and Ant Group are lobbying for offshore renminbi tokens under Hong Kong’s upcoming licensing regime (effective August 1, 2025). Hong Kong has received over 40 applications (including from Ant, JD, Standard Chartered, and Circle), but will grant fewer than ten licenses under strict capital, reserve, and AML rules.

Risk: These renminbi stablecoins face strong central bank control—subject to PBoC policy shifts and capital control restrictions. Offshore issuers must also navigate uncertainties in license approvals under Hong Kong’s regime.

3. Japan – Cautious Innovation

Japan’s revised Payment Services Act (mid2023, updated early 2025) restricts stablecoin issuance to banks, trust firms, and licensed payment providers. Issuers must hold fully backed reserves (domestically trust held), with up to ~50% allowed in short-term government bonds.

Risk: Such rigid requirements limit yield potential in a low interest environment and raise bar on reserve management, ultimately squeezing profitability for issuers.

Risk Considerations

1. Banking and Reserve Risk

Stablecoins like USDC keep real money in banks to back their tokens. But in March 2023, when Silicon Valley Bank failed, $3.3 billion of USDC’s funds got stuck. This caused USDC to lose its $1 value temporarily, dropping to $0.87. If a bank fails, people may lose trust, and the stablecoin can drop in value.

2. Smart Contract Risk

Many stablecoins use smart contracts to operate. But these programs can have bugs or be hacked. In the past, projects like Euler and Curve lost millions of dollars due to code problems or trick attacks. Even well-known stablecoins can be exposed if the technology isn’t strong enough.

3. Reserve and Liquidity Risk

If a stablecoin doesn’t keep enough safe and liquid assets—like U.S. Treasury bills or cash—it may fail to pay back users when people try to redeem their coins. In Europe, new rules (like MiCA) require stablecoins to show their reserves in real time to help prevent this. Not following the rules can lead to big fines—up to €15 million or 3% of company revenue.

4. Losing the Peg and Market Panic

Sometimes even the biggest stablecoins briefly lose their $1 value (called “de-pegging”). This can happen during times of stress or bad news. When that happens, investors may rush to sell weaker stablecoins and move to safer ones. This can create sharp moves in the market and hurt confidence.

Conclusion: Stablecoins as the Dollar's Digital Avatar

The U.S. has chosen its path in the digital currency race — not a central bank token but privately issued, dollar-backed stablecoins operating under clear federal frameworks.

For investors, this marks a generational shift. Stablecoins are no longer a crypto product—they are now becoming the operating system of digital finance. The play is no longer just about tokens but also on retaining control over the settlement layer of the global economy.

In the coming quarters, institutional capital is expected to flow into stablecoin infrastructure, increased coordination between TradFi and Web3, and a blurring line between sovereign money and protocol-native liquidity. In the future, stablecoins will likely be less of a product—but more of a public utility.